There were no S&P 500 earnings reactions on Monday, but Canadian banks are red hot right now. We need to tell you about it.

Canadian banks have been absolute monsters for decades, backed by conservative underwriting, dominant domestic market share, and a regulatory environment that favors scale.

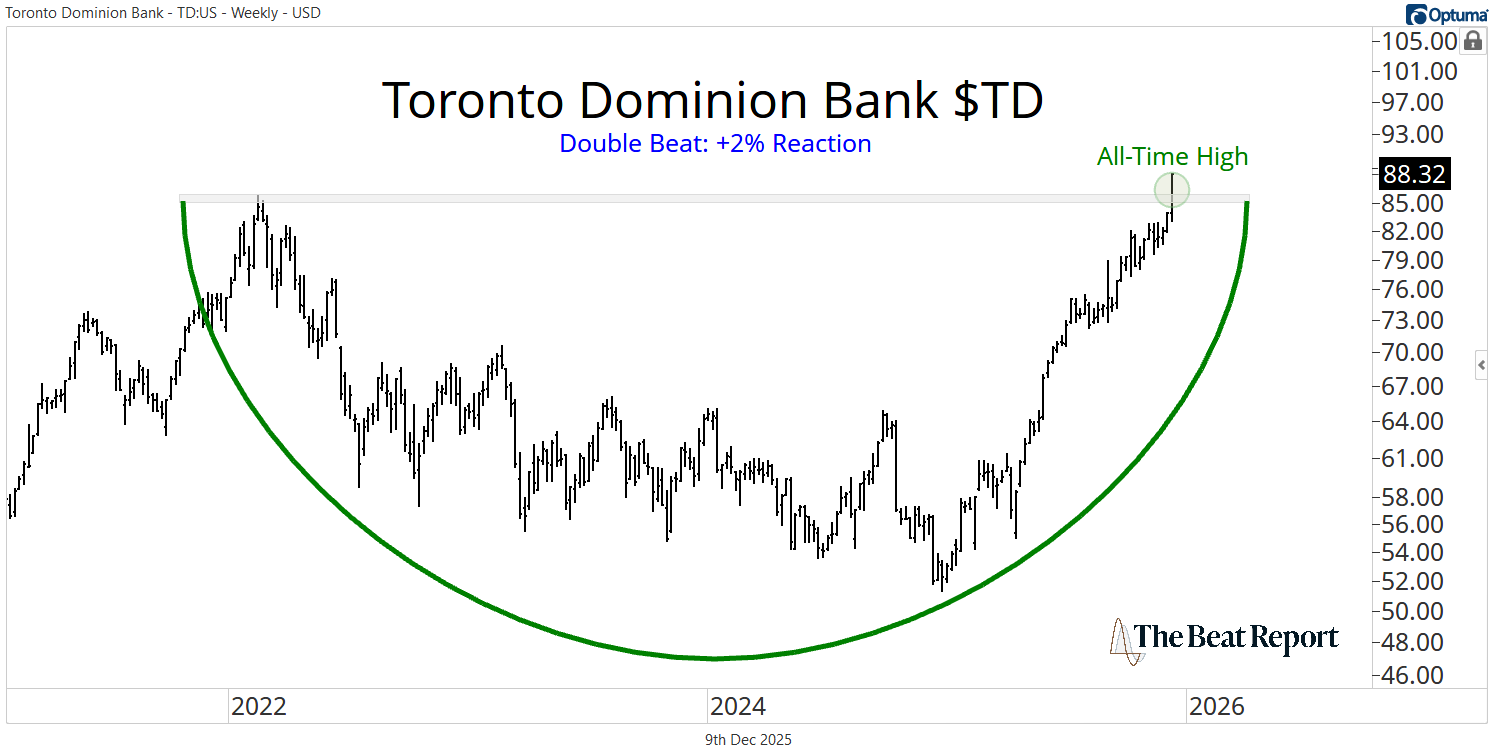

Toronto-Dominion Bank $TD is a perfect example of that.

This is a giant, diversified, cash-machine bank that keeps putting up clean earnings results and paying investors steadily rising dividends. The stock currently yields about 3.5%, and we expect it to continue growing.

The stock's combination of yield and technical strength is almost impossible to find anywhere else in global banking.

TD reported earnings last Thursday and beat both revenue and EPS expectations, then immediately gapped higher and never looked back. The stock rallied more than 2% on the day and followed through with another 2.5% on Friday.

That two-day surge pushed the stock decisively above the prior cycle’s peak from early 2022, completing a massive multi-year base. What’s even more impressive is how broad the strength was inside the quarter.

The company delivered record revenue, deposit, and loan volumes in Canadian personal and commercial banking, strong fee and trading income in wholesale banking, and record wealth earnings and assets across the entire wealth and insurance business.

Net income in U.S. retail was up 29% year-over-year on an adjusted basis, with continued progress in balance-sheet cleanup and in improving net interest margins.

In Canada, personal banking originations reached record levels, card balances continue to expand, and business lending remains comfortably ahead of trend.

The profitability metrics appeared solid as well.

Return on equity is 10.7%, efficiency ratios are performing well, and capital levels remain exceptionally strong, with a 14.7% CET1 ratio even after share buybacks.

TD also announced another dividend increase and continues to target a 40-50% payout ratio in the long term, meaning this dividend profile isn’t just attractive today; it’s built to rise with earnings over time.

Canadian banking is fundamentally an oligopoly, and TD is one of its crown jewels.

The technicals are just as good as the fundamentals.

TD has put the finishing touches on a massive accumulation pattern. From here, the path of least resistance is higher for the foreseeable future.

Except for Bank of Nova Scotia $BNS, every major Canadian financial stock is at a new all-time high. We expect the BNS to catch-up soon.

The macro backdrop favors large, well-capitalized banks with diversified revenue streams. That's why the market loves the Canadian banks.

The fundamentals are healthy, the dividends are excellent, and the technicals are supportive.

Happy Technical Tuesday!

-The Beat Team

P.S.Save your spot for today’s closed-door retail briefing with Macke. This session gives you access to his boots-on-the-ground consumer read, the kind normally reserved for members.