There were no S&P 500 earnings reactions on Tuesday, but we want to tell you about an emerging leader in financials.

Ally Financial $ALLY is a diversified financial services company best known for two things: it’s one of the largest auto lenders in the U.S., and it operates the nation’s largest all-digital bank.

They sit at the intersection of consumer credit, dealer finance, insurance, and deposits, which gives them a unique funding advantage and a highly scalable model.

In simple terms, they take in low-cost digital deposits and deploy them into higher-yielding auto loans and commercial finance, while layering on insurance and fee income along the way.

Over the past year, that model has begun to operate as intended.

Credit trends are improving, margins are stabilizing, and returns are moving decisively higher.

In the most recent quarter, Ally delivered EPS of $1.18, more than doubling year-over-year.

Net interest margin continued to expand, retail auto credit metrics improved meaningfully, and capital ratios strengthened as the company executed a $5B credit risk transfer at the tightest spreads in its program history.

Just as importantly, Ally’s deposit franchise remains a clear differentiator, with $142B in retail deposits, 92% FDIC insured, and customer growth now extending to 66 consecutive quarters.

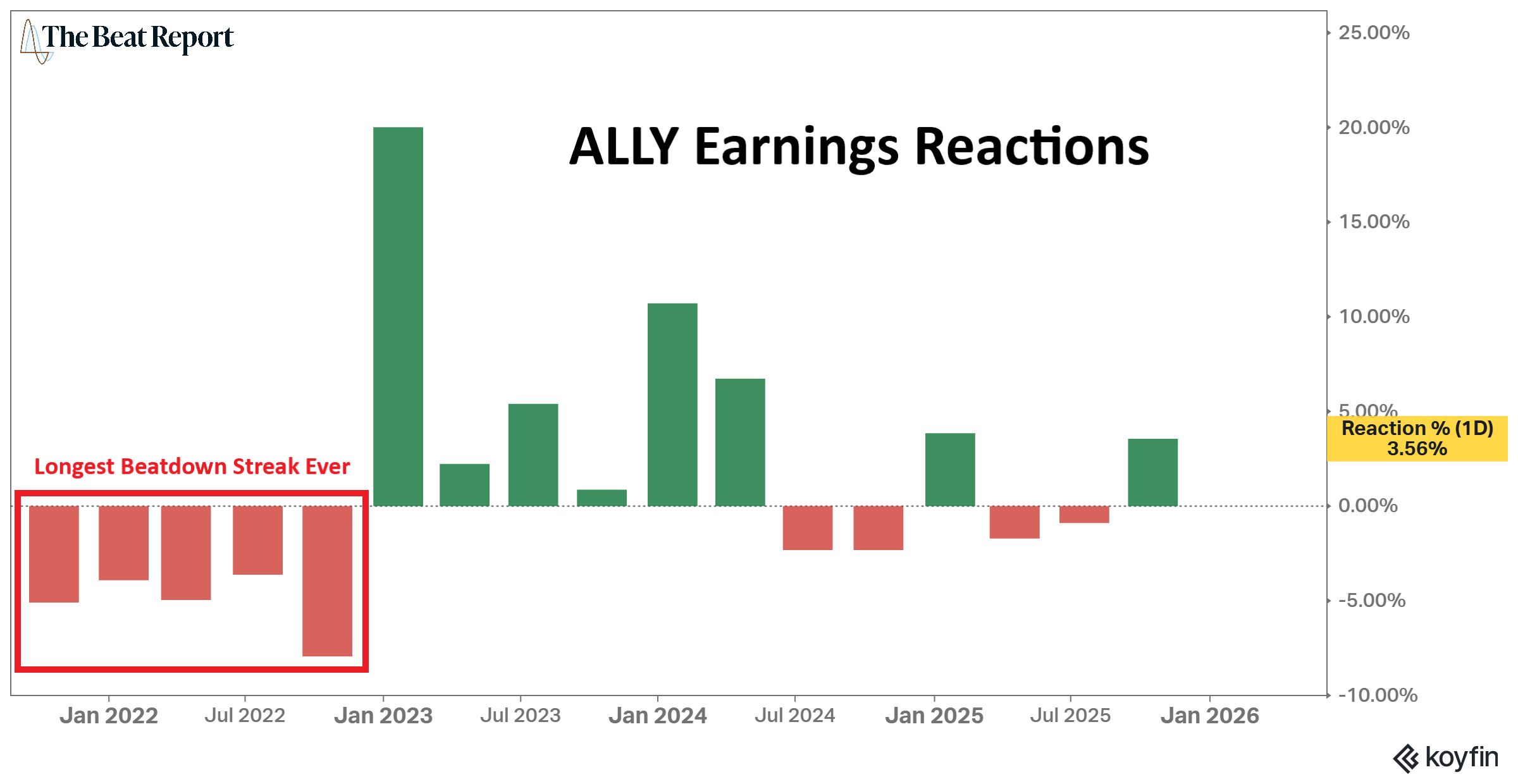

That fundamental progress is evident in how the market has been reacting to earnings.

After suffering its longest earnings beatdown streak ever in 2022, Ally snapped that negative cycle in Q1 2023 with a more than 20% post-earnings rally, the strongest reaction in the stock’s history.

That moment marked a clear inflection point in earnings sentiment.

Since then, shareholders have consistently been rewarded for the company's earnings events.

The most recent report in October reinforced that trend, as Ally beat both top- and bottom-line expectations, rallied roughly 3.5% on the day, and has seen steady upside follow-through since.

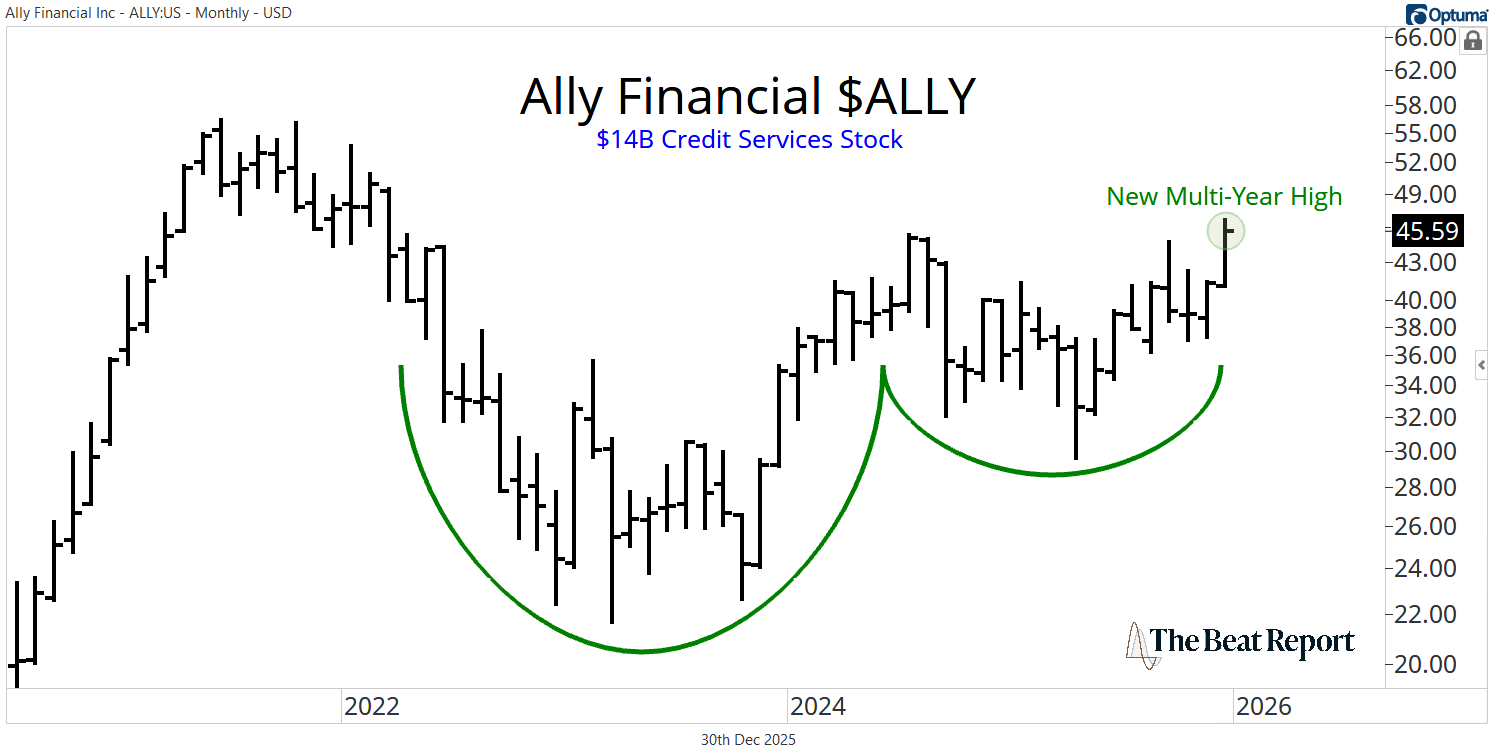

The stock chart tells the same story from a longer-term perspective.

After spending years carving out a textbook bearish-to-bullish reversal, ALLY is now breaking out to new multi-year highs.

This isn’t a stretched, late-cycle move.

It’s the early phase of a new primary uptrend, emerging as fundamentals, sentiment, and price finally align.

With the company set to report again on January 21, expectations are already elevated. Given the improving credit backdrop, expanding returns, and the market’s apparent willingness to reward execution, the setup suggests Mr. Market is leaning toward more upside than disappointment.

In short, ALLY has gone from a stock the market loved to hate to one that’s finally being re-rated.

The earnings reactions changed first.

The fundamentals followed.

Now, the price is confirming it.

Happy New Year's Eve! 🍾

-The Beat Team

P.S. More activity doesn’t mean better results, especially in options.

ASC Options emphasizes clarity and structure, and with end-of-year access now 50% off, it’s a measured way to add options exposure heading into January.