Earnings are the heartbeat of the market, and every week brings a fresh set of opportunities and risks.

With each report, we get new information on corporate health, investor sentiment, and where money is rotating.

In the Weekly Beat, we spotlight the most important earnings reactions from the prior week: the winners, the losers, and the surprises that moved markets.

Then we shift our focus to the week ahead, breaking down the technicals and fundamentals.

Whether it’s mega-cap leaders, niche growth stories, or the sectors most tied to the economy, we’ve got you covered on what traders need to know right now.

After missing expectations across the board, CSX $CSX rallied 2.4%. This wasn't a good quarter, but the management team's forward guidance was tremendous. They expect low single-digit revenue growth, 200-300 basis points of operating margin expansion, and at least 50% free cash flow growth.

Following a big double beat, Intel $INTC cratered 17% for its worst earnings reaction since 2002. While this quarter's results exceeded the market's expectations, the management team's forward guidance was weaker than expected.

The $55B energy services stock, Baker Hughes $BKR crushed the market's expectations and rallied 4.4% to the highest level since 2017. During the quarter, the company had major contract wins in LNG, power systems, and new energy, including data center and geothermal projects, as well as significant awards in the U.S., Kazakhstan, and the Middle East.

Steel Dynamics $STLD posted mixed headline results, and initially popped to a new all-time high. However, the sellers stepped in during the session and pushed the price 4.4% lower for the worst earnings reaction since Q1 2021.

After beating headline expectations, the $40B food distribution stock, Sysco $SYY rallied 10.1% and snapped a 5-quarter beatdown streak. Following this blockbuster earnings report, the management team raised its forward EPS guidance. They also expect to raise the dividend significantly.

In reaction to a mixed earnings report, UnitedHealth $UNH tanked nearly 20%. Shareholders have now been punished for 5 of the past 6 earnings reports.

Following another big double beat, Seagate Technology $STX had its second consecutive 19% earnings reaction. Gross margin reached 42.2%, growing a remarkable 670 basis points year-over-year.

The $178B electronic components stock, Amphenol $APH, beat the market's expectations, yet the market showed no interest. Sellers drove the price down by over 12% for the worst earnings reaction of the 21st century.

Despite posting mixed headline results, Southwest Airlines $LUV rallied 18.7%, market the best earnings reaction of the 21st century. The management team expects to earn $4 per share in earnings during 2026. This is more than a threefold increase from 2025.

The world's largest software stock, Microsoft $MSFT beat expectations across the board, but fell 10% for the worst earnings reaction since 2013. While the management team issued solid revenue guidance, the market was disappointed by the Microsoft Cloud guidance. They expect a significant decline in profitability due to AI investments.

What's happening next week 👇

Next week will be packed with big earnings reports, and our attention will be focused on the mega-cap tech and healthcare stocks, including Alphabet $GOOGL, Amazon.com $AMZN, Eli Lilly $LLY, and Novo Nordisk $NVO.

We'll also be watching:

Tech stocks such as Palantir $PLTR, Advanced Micro Devices $AMD, and NXP Semiconductor $NXPI.

The energy giants Shell $SHEL and Conoco Phillips $COP.

Healthcare bellwethers, including Pfizer $PFE, Merck $MRK, and Bristol-Myers Squibb $BMY.

The exchange operators CME Group $CME and Cboe Global Markets $CBOE.

And more!

There will be plenty of earnings reactions to unpack next week in the Daily Beat. Stay tuned...

Now, let's talk about the reports that are front and center for us next week.

Let’s start with the strongest chart on the board.

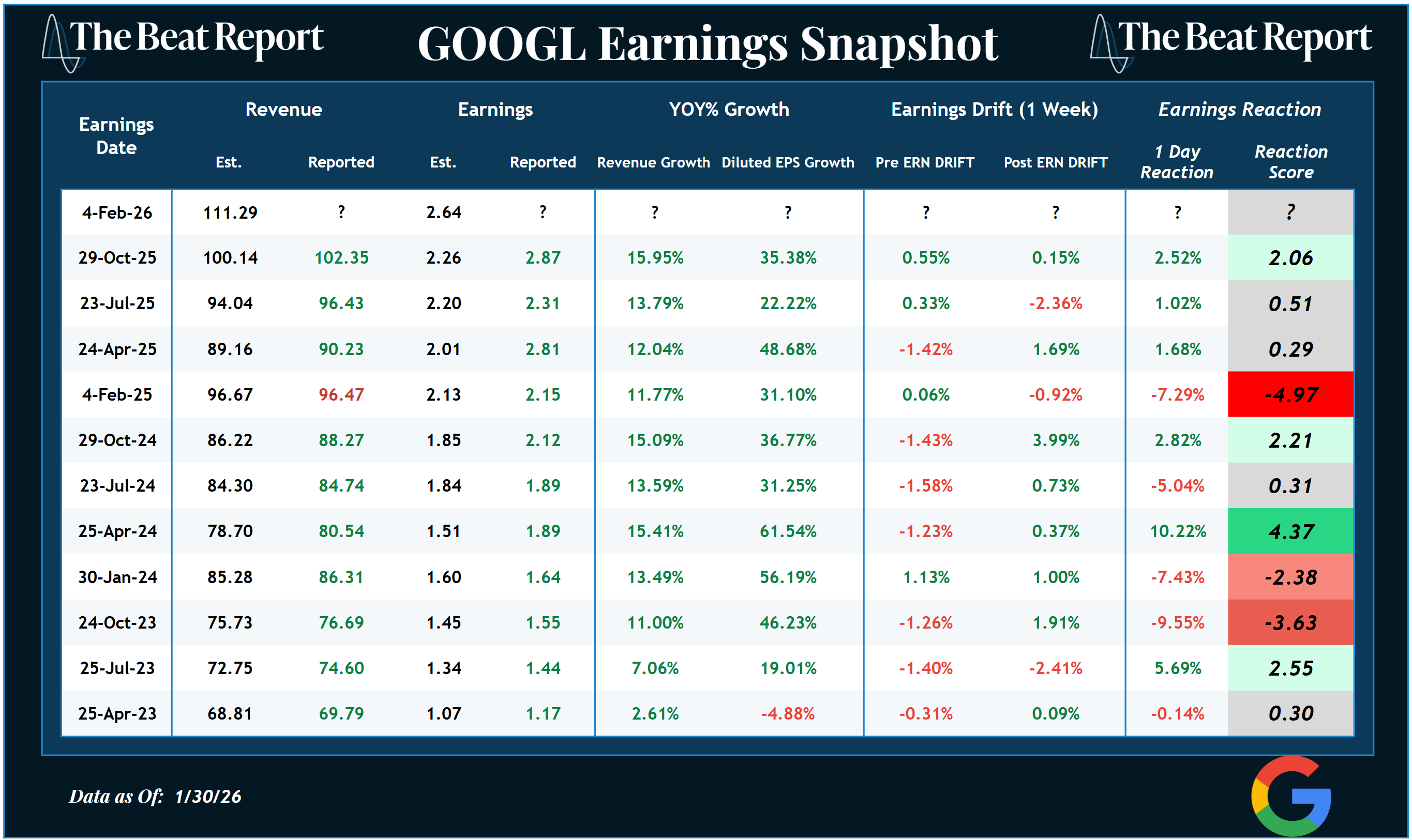

Alphabet $GOOGL reports earnings Wednesday after the market closes, with the Street looking for $111.29B in revenue and $2.64 in earnings per share.

Heading into the report, the technical picture is about as clean as it gets. Since bottoming in April of last year, the stock has been in a virtually straight-line higher, repeatedly carving out textbook bullish continuation patterns and resolving them to the upside.

Every pause has been constructive, and every pullback has been shallow.

This has been the most dominant player within mega-cap tech, and there’s nothing in the price action to suggest that trend is ending. If anything, GOOGL looks poised for another upside resolution if earnings deliver.

The fundamentals are doing exactly what you want to see in a leadership stock.

Over the past three years, Alphabet has consistently beaten top- and bottom-line expectations, while delivering spectacular revenue and earnings growth.

Even more important, the market has rewarded the stock for it. Alphabet has now seen three consecutive positive earnings reactions, confirming that earnings sentiment is firmly aligned with the bullish technical trend.

This is what leadership looks like, and heading into earnings, GOOGL remains one of our favorite setups in mega-cap tech.

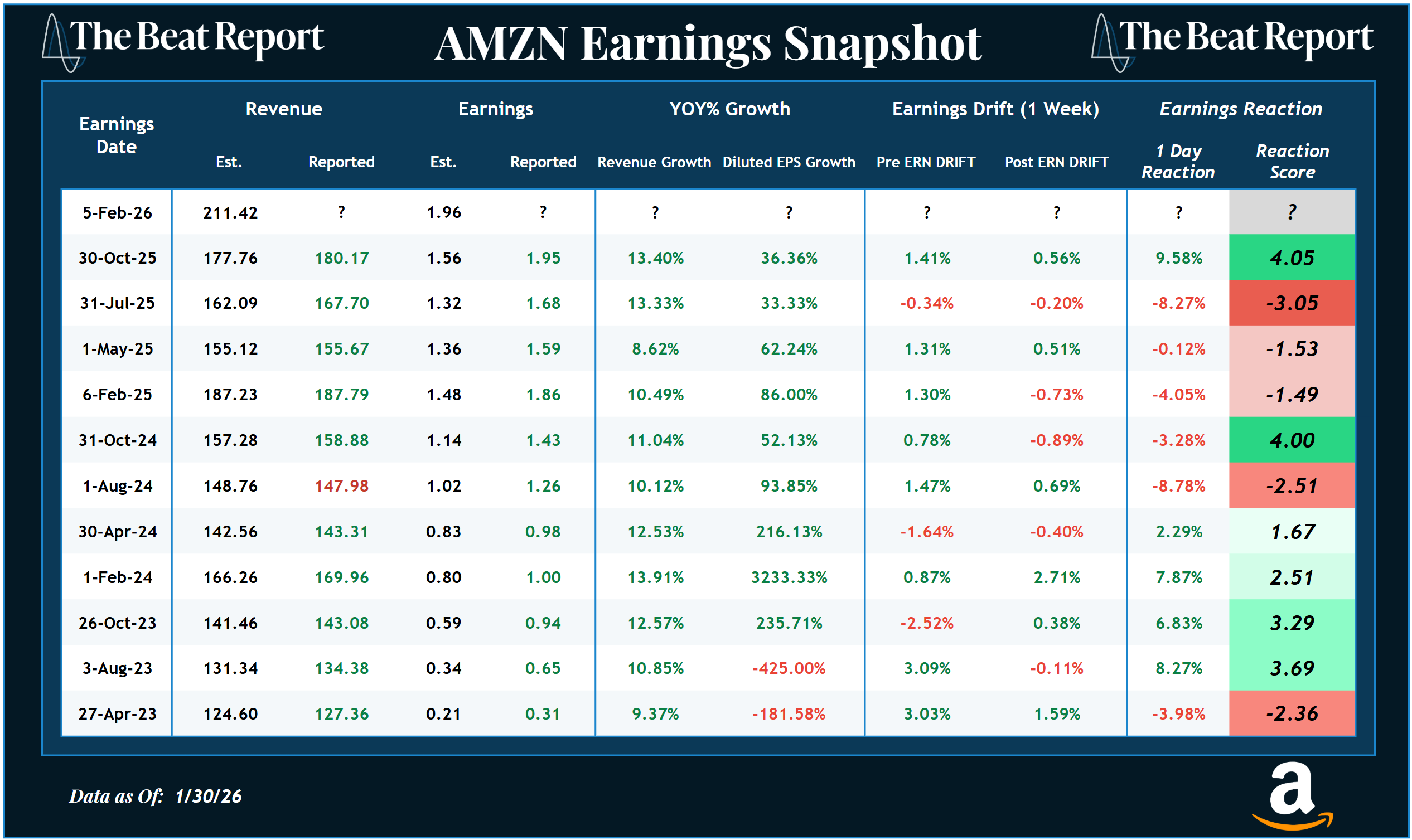

Next up is Amazon $AMZN, which reports Thursday after the market closes. The market is expecting $211.42B in revenue and $1.96 in earnings per share.

From a technical perspective, Amazon has been one of the messiest charts in the mega-cap growth space.

Despite multiple opportunities to break out and establish a new primary uptrend, the stock has repeatedly failed to follow through.

Instead, it continues to churn sideways, carving out what appears to be a massive accumulation pattern. The structure is in place, but the buyers haven’t yet proven they’re in full control.

That’s why this earnings report matters so much. A strong reaction could be the catalyst that finally puts the finishing touches on this base and launches a new uptrend.

Until then, the path of least resistance remains sideways, and patience is required.

Fundamentally, Amazon remains a machine.

Amazon almost always beats expectations, and while earnings growth has decelerated recently, it’s still impressive. Last quarter, earnings per share grew 36% year-over-year, alongside double-digit revenue growth.

More importantly, we saw a clear change in earnings sentiment. Amazon snapped a five-quarter streak of negative earnings reaction with its best post-earnings move in years.

That shift matters.

If the company delivers again this quarter, it could have major technical implications for a stock that has been coiling for a long time.

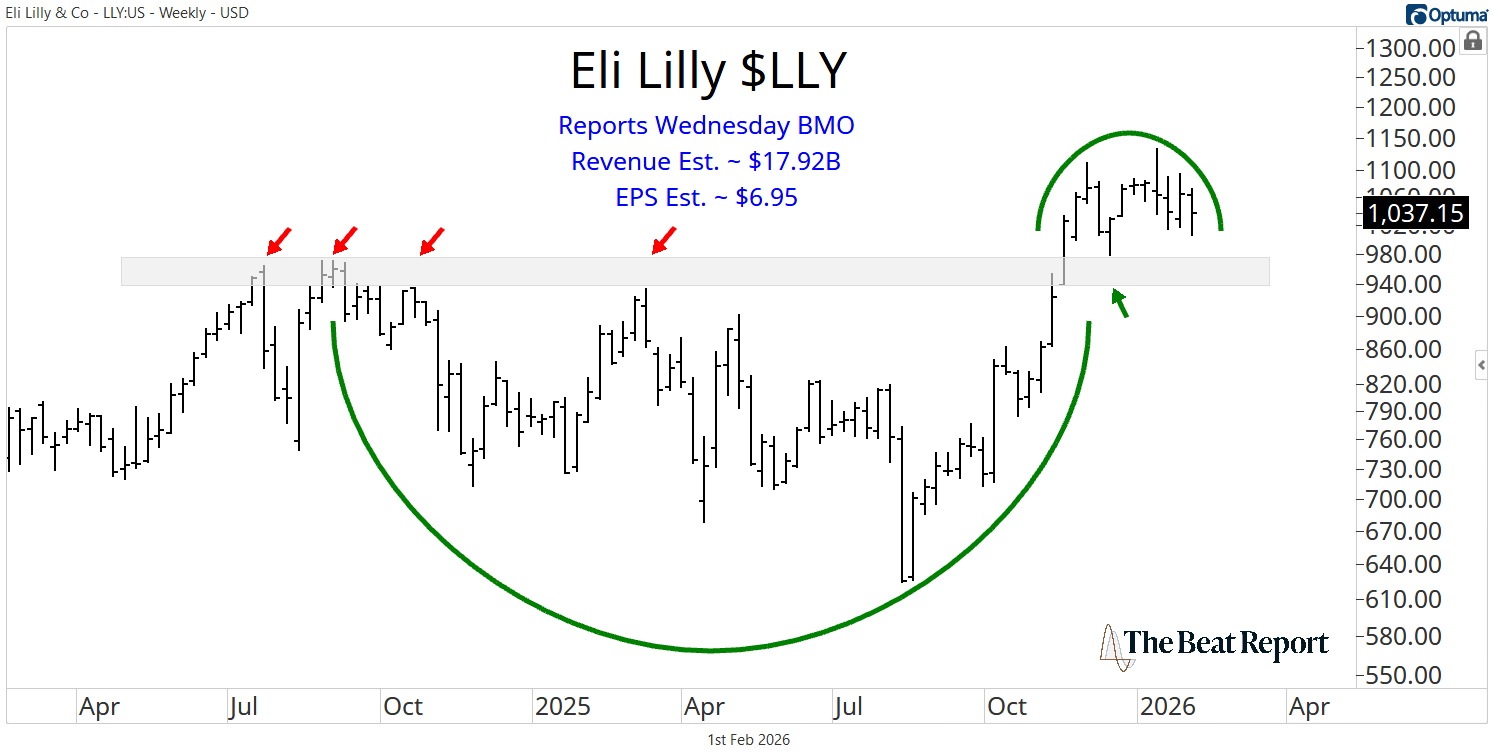

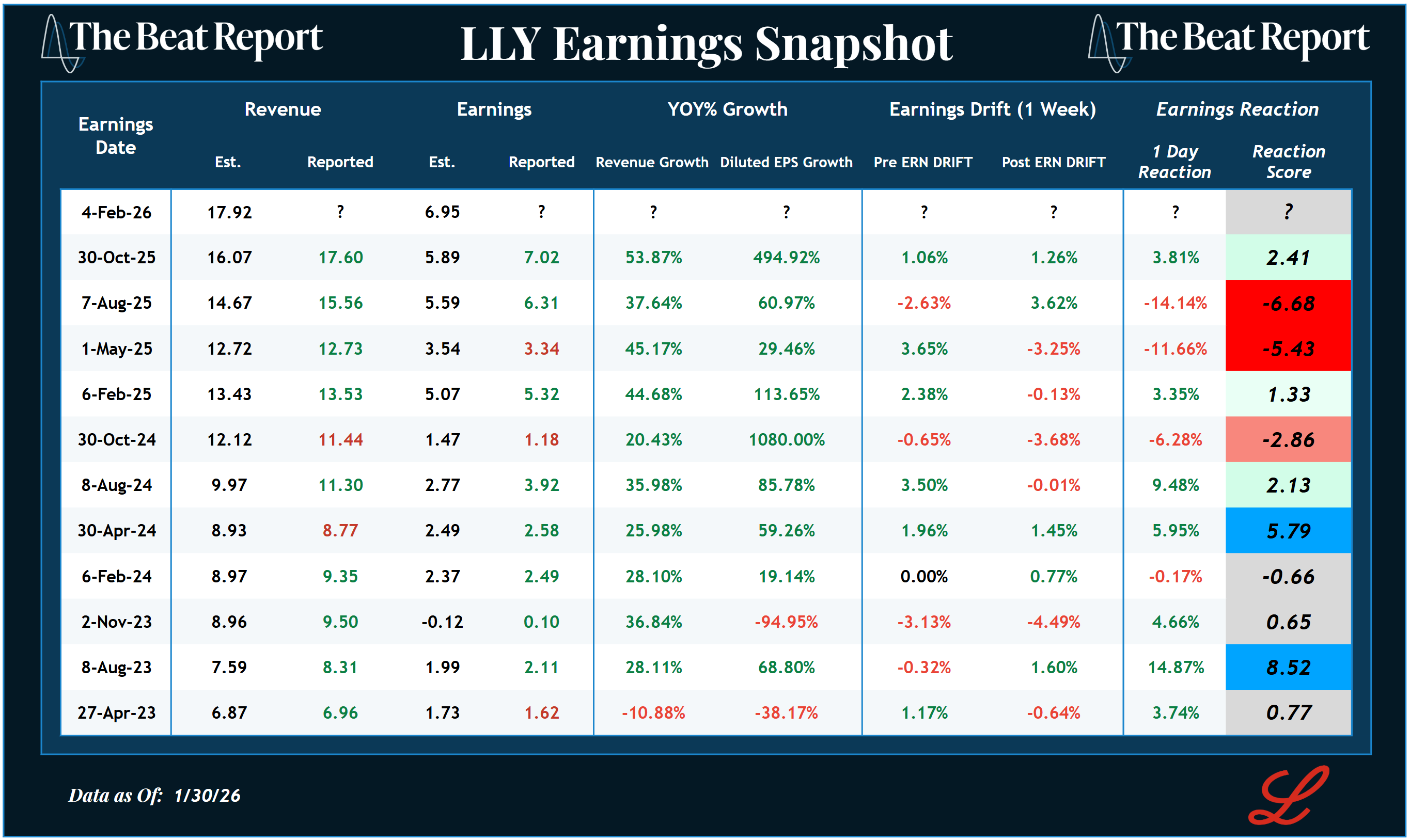

Shifting gears from mega-cap tech to healthcare, we turn to the GLP-1 leaders, starting with Eli Lilly $LLY. The company reports on Wednesday before the market opens, with expectations for $17.92B in revenue and $6.95 in earnings per share.

Technically, Eli Lilly already did the hard part late last year when it completed a prolonged accumulation pattern and broke out to new all-time highs.

Since then, the stock has been consolidating above former resistance, successfully flipping it into support.

As long as this level holds, the primary uptrend remains firmly intact, and a fresh leg higher appears to be a matter of time.

The earnings snapshot reinforces that view.

While Eli Lilly suffered back-to-back ugly earnings reactions earlier last year, that negative streak ended decisively with a +3.81% reaction late in 2025, which helped drive the breakout.

And the growth numbers remain absurd.

Revenue growth is strong, but earnings growth is on another planet. A 494% year-over-year increase in earnings per share is almost unheard of at this scale.

This is still one of the best fundamental stories in the entire market, and both the technicals and fundamentals remain aligned in strong primary uptrends.

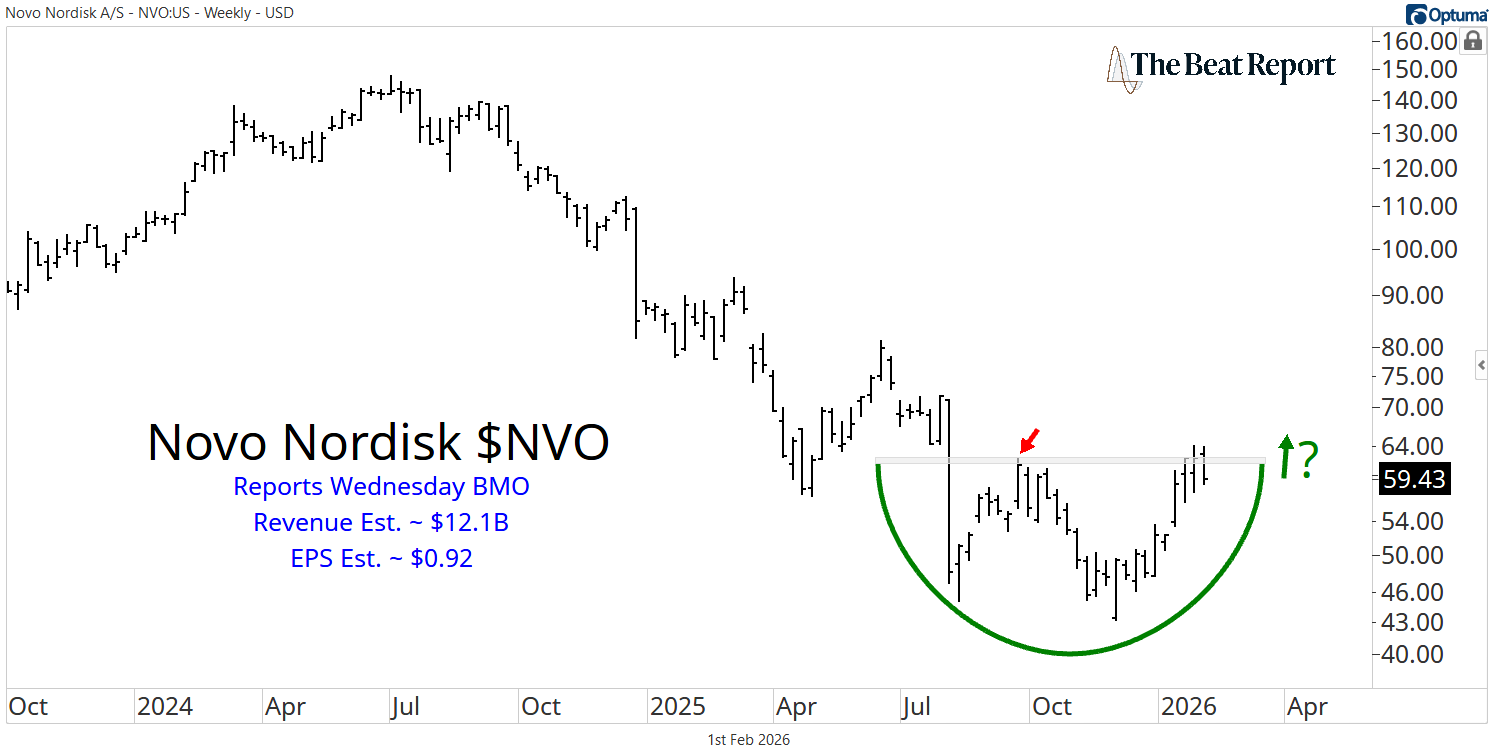

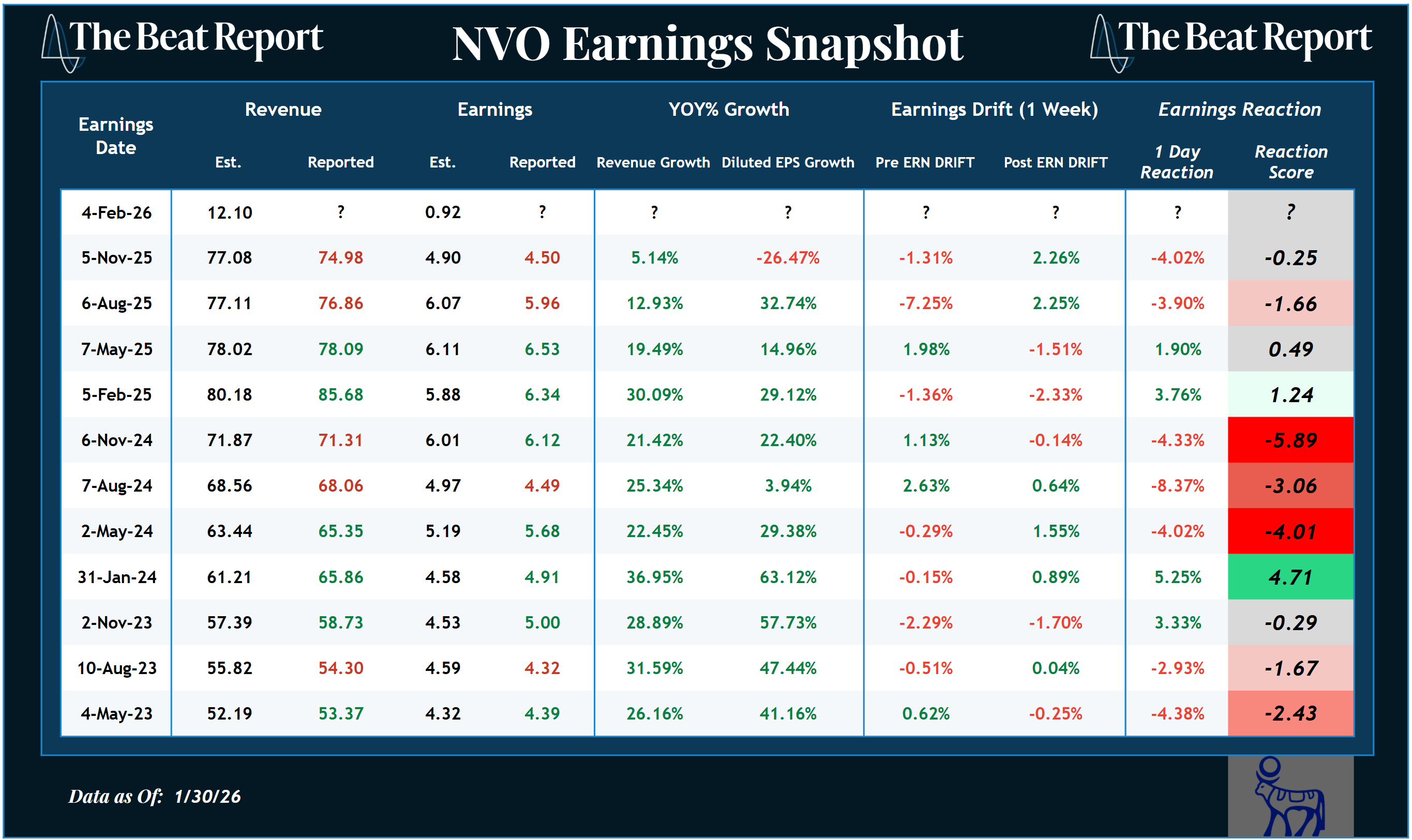

Finally, we get to Novo Nordisk $NVO, which also reports on Wednesday before the market opens. The market is looking for $12.1B in revenue and $0.92 in earnings per share.

Unlike Eli Lilly, Novo Nordisk’s chart tells a very different story. The stock suffered a brutal decline of more than 70% over roughly a year and a half, wiping out years of gains.

However, the important thing is that the selling pressure has stopped. Price has stabilized and carved out a textbook bearish-to-bullish reversal pattern, and it’s now pressing up against the upper boundary of that structure.

A decisive breakout here would mark a major regime shift and kick off a brand-new primary uptrend.

But we don't want to jump the gun.

The earnings snapshot explains why.

Novo Nordisk has now missed headline expectations in back-to-back quarters, resulting in two consecutive negative earnings reactions.

Even more concerning, last quarter, the company posted its first year-over-year decline in earnings per share in many years. This broke a long-standing growth streak.

That fundamental deterioration is why we're not sold on the improving technical picture.

Could that change with this earnings report? Absolutely.

But until it does, patience is critical.

This is a stock that needs to prove itself again, both fundamentally and technically, before we get aggressive.

The takeaway this week is simple: some leaders are already in full control, others are approaching make-or-break moments, and earnings reactions will tell us exactly where capital wants to flow next.

As always, we’ll let price and earnings sentiment do the talking.

Cheers to a new week!

-The Beat Team

P.S. Earnings season creates opportunity, but only if you know how to trade the events.

Instead of guessing direction, Steve Strazza focuses on how the market responds to earnings to identify high-probability trades.

Watch the replay to see how fundamentals, technicals, and sentiment come together to turn earnings volatility into actionable trades.