Here's the thing about options that continues to blow my mind even after 27 years of doing this: the Greeks don't always behave the way the textbooks tell you they should.

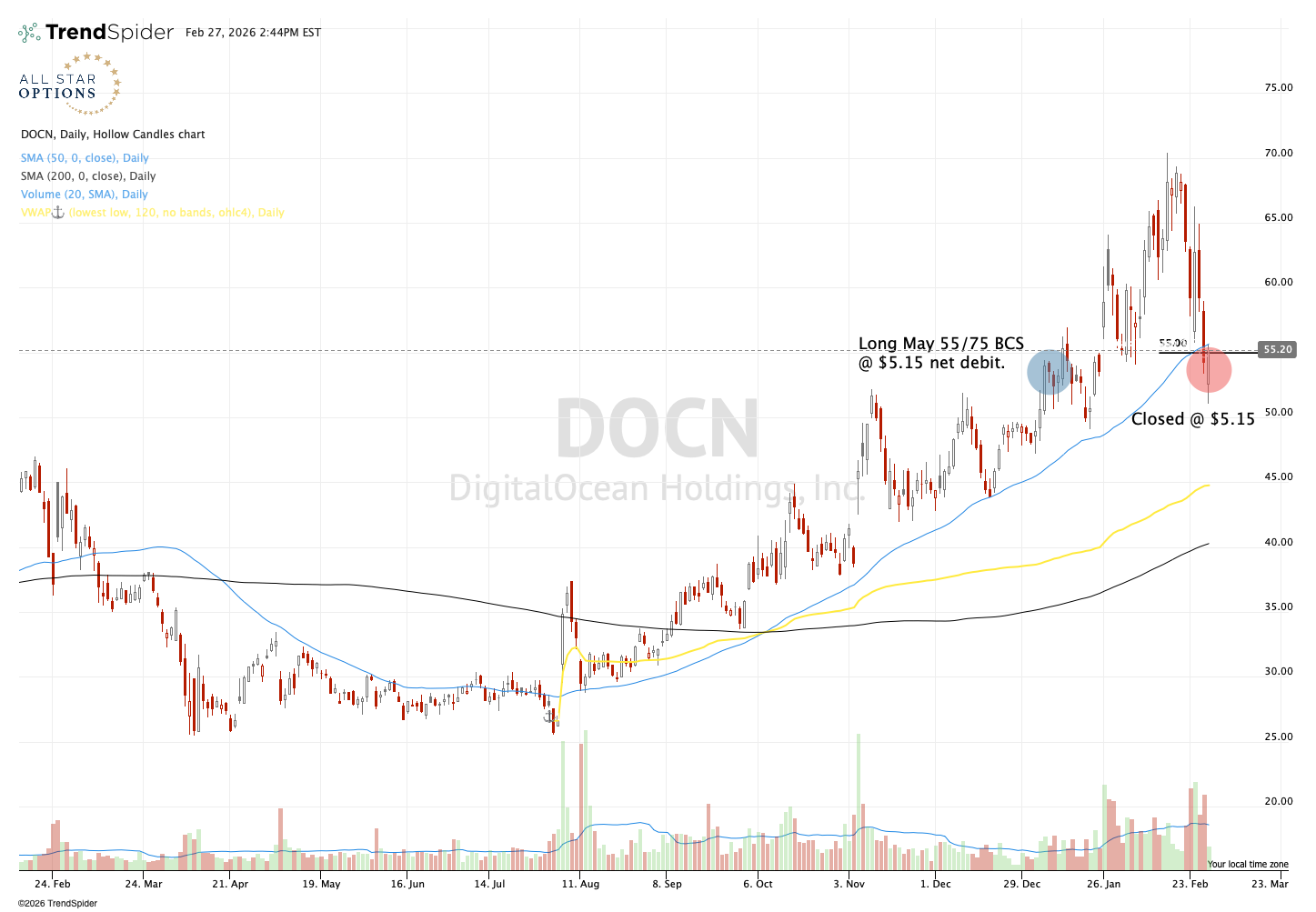

I've been in a May bull call spread on Digital Ocean $DOCN for 51 days. I entered on January 7th, paying $5.15 for the spread when the stock was trading around $54. Today — 51 days later — the stock was again trading right around $54 and I decided to exit because it had dropped below my updated stop level at $55. When I got my fill, I looked at the price and had to do a double take.

$5.15.

The exact same price I paid 51 days ago. A perfect scratch. Not a penny more, not a penny less:

Now, your first instinct might be the same as mine: how in the name of the Theta Gods is this possible? Shouldn't 51 days of time decay have eaten into this position? Shouldn't I have lost money here?

In theory, yes. And this is where it gets interesting.

What likely happened is that implied volatility expanded enough over those 51 days to completely offset the theta decay. Remember, when you're long a vertical spread, you're exposed to changes in implied volatility — particularly through vega. If IV rises while the stock stays flat, that rising IV can pump value back into your spread, counteracting the time decay that would otherwise be draining it.

Think about it this way: theta was quietly taking money out of my pocket every single day for 51 days. But vega was quietly putting money back in. And in this case, they happened to perfectly cancel each other out. It's like two tug-of-war teams pulling with the exact same force — nobody moves.

This is also a good reminder of why I trade spreads with plenty of time until expiration. When you give yourself enough runway, theta decay is slower and the other Greeks have room to work in your favor. If this had been a two-week trade, the theta would have been far more aggressive and IV expansion probably couldn't have saved me.

But here's what I really want you to take away from this: I followed my process.

The stock was below my stop, so I got out. I didn't hope, I didn't negotiate with the market, I didn't tell myself a story about why it might come back. I just executed the plan. And the market happened to give me a gift — a free look at a trade with zero cost.

Fifty-one days of exposure to Digital Ocean, and my only cost was the commission. I'll take that all day long.

Sometimes the Theta Gods giveth, and the Vega Gods giveth right back.

If you want to see every trade I'm putting on — the entries, the exits, the reasoning behind the strategy selection, and the risk management plans — come join us at All Star Options.

Sean McLaughlin | Chief Options Strategist, All Star Charts

--> If you'd like to receive these notes in your email, sign up here.