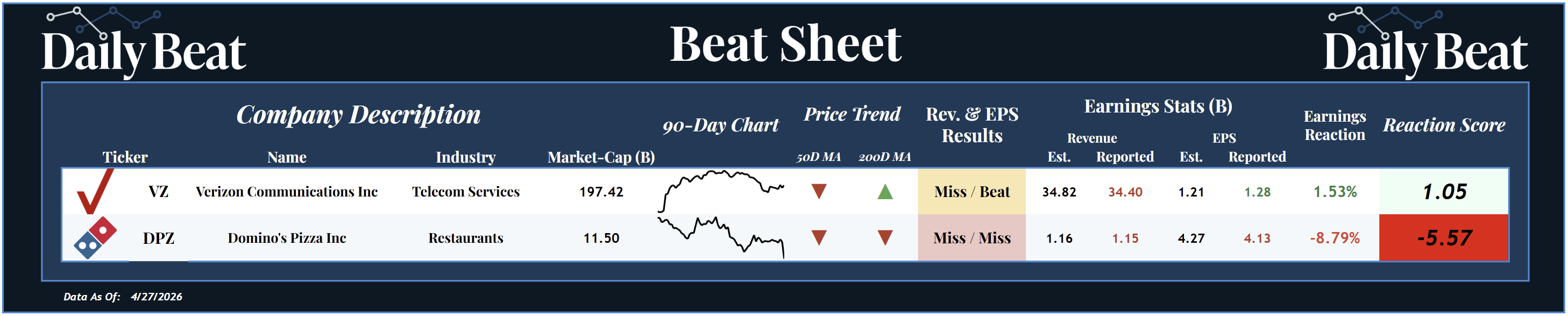

Here's why the market rewarded Verizon for reporting earnings & punished Domino's Pizza.

April 28, 2026

Yesterday’s action wasn’t about fireworks or extreme dispersion across dozens of names.

But underneath the surface, it told a very clean story about where capital wants to go… and just as importantly, where it doesn’t.

On one side, a nearly $200 billion telecom is quietly doing everything right and continuing to earn higher prices.

On the other hand, a consumer-facing brand is losing momentum, both fundamentally and technically, as the market responds accordingly.

*Click the image to enlarge it

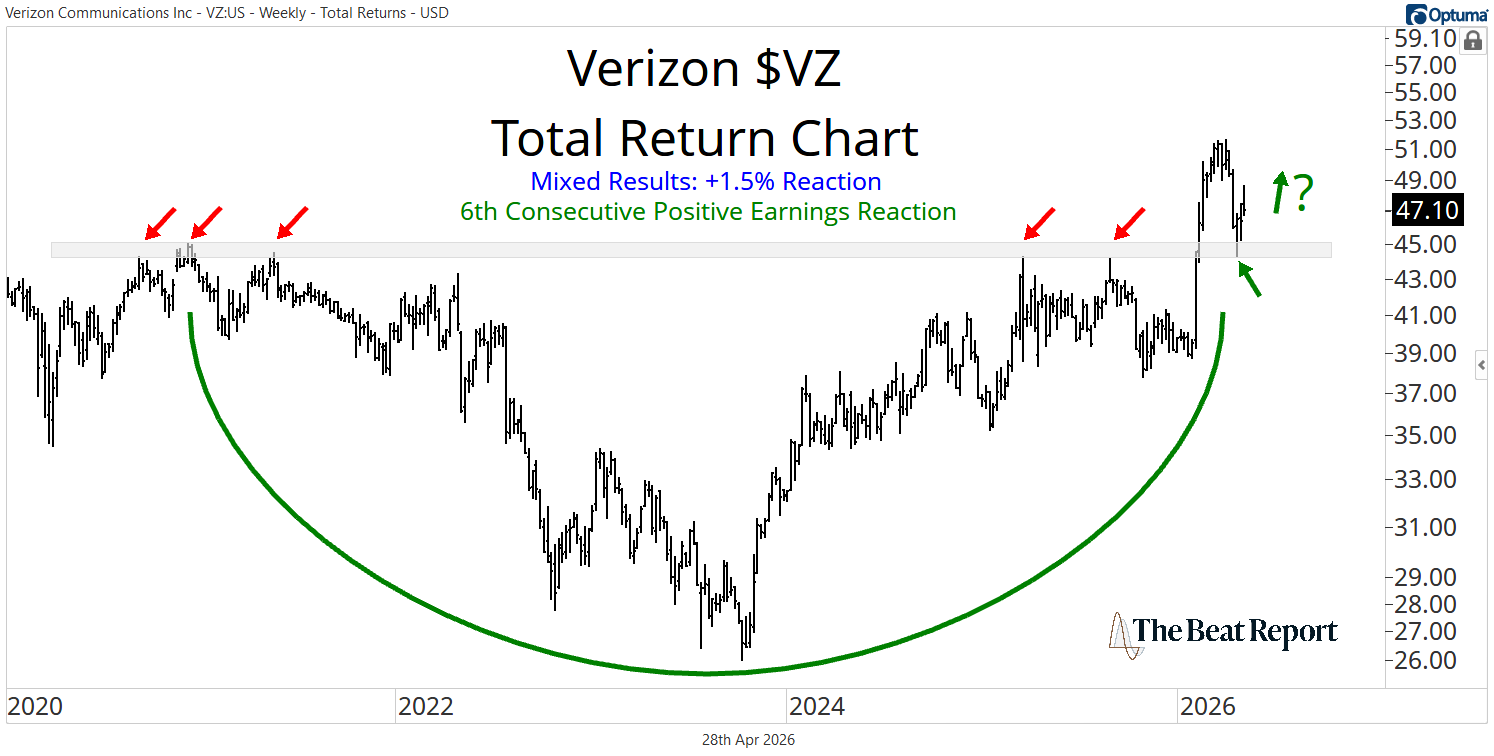

Starting with Verizon $VZ, this is one of the more interesting setups in the entire market right now, not because it’s flashy, but because it’s working.

The company came out and reported mixed results, missing revenue expectations while beating on earnings, and the stock responded accordingly with a modest gain.

Nothing dramatic, but this now marks 6 consecutive positive earnings reactions, and that consistency matters more than any single quarter.

When you dig into the fundamentals, it's clear that Verizon is no longer chasing growth at any cost.

Instead, management is deliberately shifting the business toward higher-quality, recurring revenue streams while improving customer economics across the board.

That shows up in 2.9% year-over-year revenue growth and 7.6% adjusted EPS growth.

This is happening even as acquisition and retention costs are coming down and churn continues to improve.

The most important piece, though, is what’s happening beneath the surface...

For the first time since 2013, Verizon posted positive first-quarter postpaid phone net adds, a clear signal that the turnaround is real and gaining traction.

This isn’t being driven by promotional gimmicks. It’s coming from a deliberate strategy focused on customer lifetime value, better service, and operational efficiency.

In other words, healthier growth.

Technically, the chart reflects exactly what the fundamentals are saying.

Verizon broke out of a massive multi-year base earlier this year and has since returned to retest that breakout level, flipping former resistance into support.

Now, on the heels of another positive earnings reaction, the stock is pressing higher once again, suggesting that this is the early stages of a new primary uptrend.

So long as VZ holds this breakout, the path of least resistance is higher for the foreseeable future.

And with a roughly 6% dividend yield, shareholders are being rewarded for sitting on their hands and riding the primary trend.

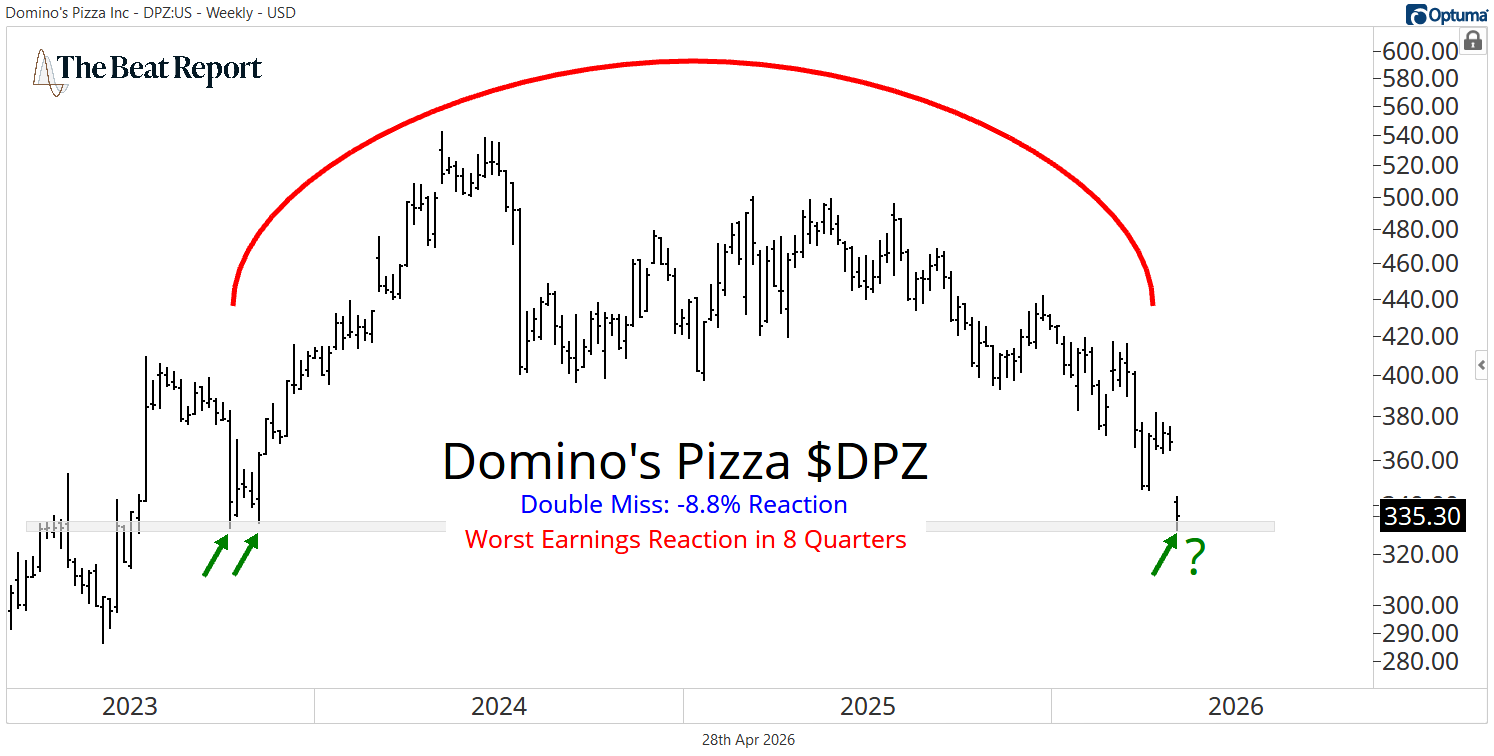

Contrast that with Domino’s Pizza $DPZ, and the difference couldn’t be more obvious.

Domino’s Pizza still has a strong long-term story on paper, but right now, the fundamentals are deteriorating, and the technicals are confirming it.

The company reported a double miss, coming up short on both revenue and earnings expectations, and the stock responded with its worst earnings reaction in 8 quarters.

The fundamental backdrop helps explain why...

Same-store sales in the U.S. came in at just 0.9%, well below expectations, as consumer pressure intensified throughout the quarter.

Management specifically highlighted declining consumer sentiment, ongoing inflation, and increased competitive intensity in the pizza space as key headwinds.

What’s more telling is that these pressures built as the quarter progressed, particularly into March.

This is a signal that the environment is getting tougher, and Domino’s is feeling it.

Even though the company continues to generate strong cash flow and has a long history of returning capital to shareholders, including billions in buybacks and dividends over the past decade, the near-term trajectory is clearly slowing.

And in this market, investors have no appetite for slowing growth.

The chart tells the same story as the fundamentals, just more bluntly.

Over the past few years, Domino’s has been carving out a large distribution pattern, and the recent price action suggests that this topping process is resolving lower.

The stock is now back at a key level that previously acted as support in late 2023, so it would not be surprising to see a short-term bounce from here.

But it’s important to keep the timeframe in mind...

The bigger picture is that the stock has broken down from a major top, and both fundamentals and technicals are pointing lower. That’s not a combination you want to fight.

We want to treat DPZ as guilty until proven innocent. This stock looks like nothing but trouble to us.

If you want more fusion analysis, you need to check out the work we're doing at the Premium Beat Report.

And we aren't just analyzing the technicals and fundamentals... We're actively putting capital to work in the strongest stocks.