SanDisk keeps ripping as AI storage demand explodes, while Stryker breaks down after its worst earnings reaction in more than a decade.

May 4, 2026

Friday kicked off the new month with another gap to fresh all-time highs for the S&P 500, and earnings season kept feeding the tape with new information.

We got fresh reactions from 29 components of the index, and the split was almost perfectly balanced between winners and losers.

Some stocks barely moved, others exploded higher, and a handful were hit hard enough to change their charts' structure completely.

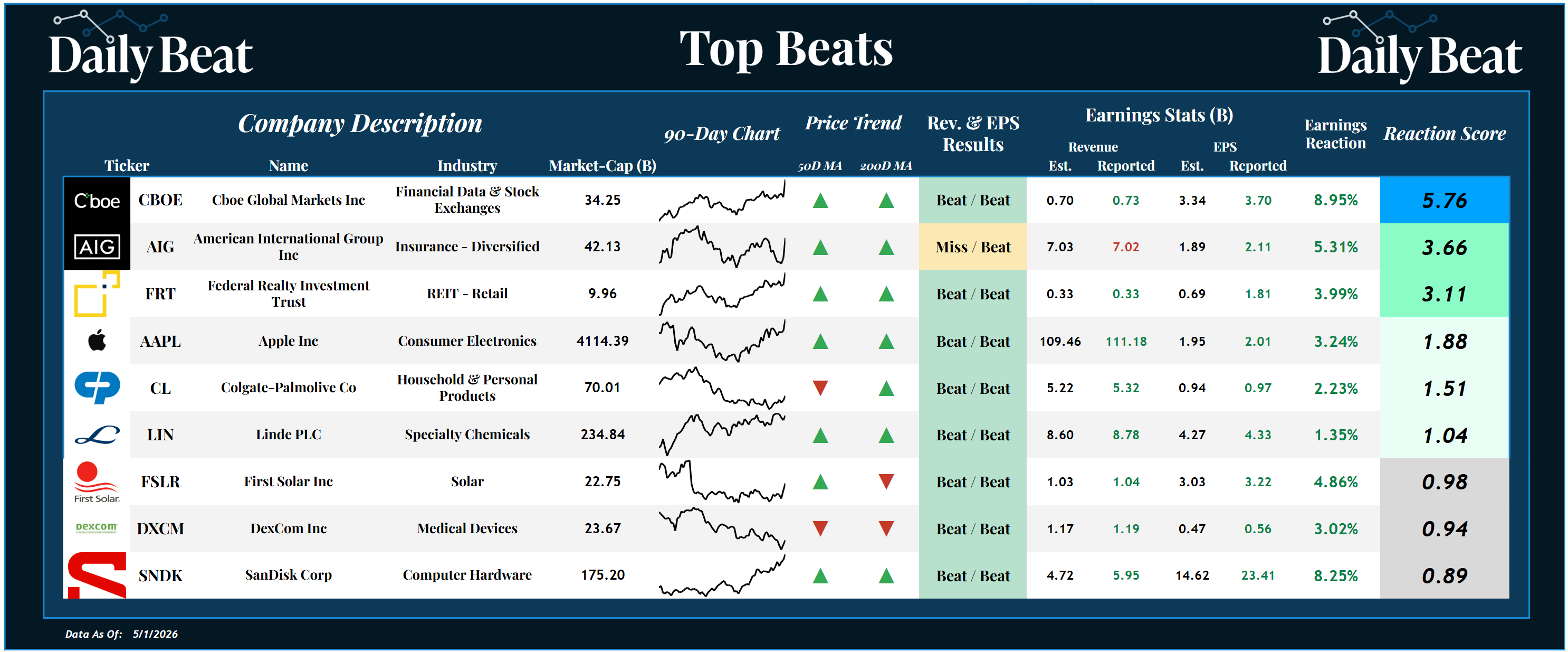

At the top of Friday's Beat Sheet, Cboe Global Markets $CBOE was the king of the session, ripping to a new all-time high on its best earnings reaction ever after a big double beat.

*Click the image to enlarge it

American International Group $AIG also stood out, rallying more than 5% in its strongest reaction since May 2023.

Meanwhile, Apple $AAPL posted its best earnings reaction since May 2024 and closed near its all-time high.

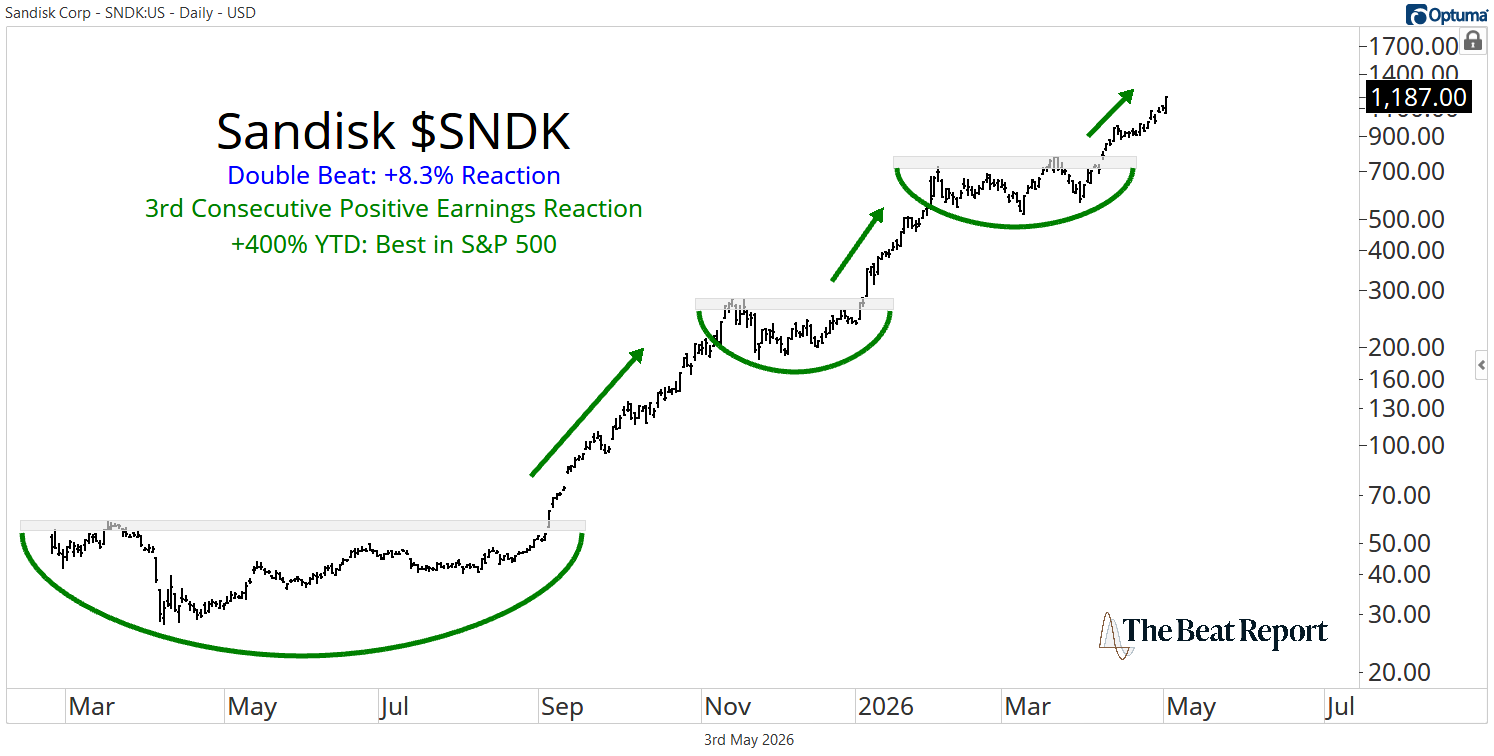

But the most important reaction on the board came from SanDisk $SNDK.

This is now a $175 billion computer hardware stock, and it is the runaway leader in the S&P 500 this year.

The stock is up more than 400% in 2026, and we are barely into May.

Intel $INTC is in 2nd place, up roughly 170%, which sounds incredible until you compare it to SanDisk.

Mr. Market is telling us loud and clear that SNDK is in a league of its own, and Friday’s reaction only reinforced that leadership.

SanDisk reported a massive double beat, clearing revenue expectations by about 26% and beating EPS expectations by roughly 60%.

The stock rallied more than 8%, closed at another all-time high, and investors have now been rewarded for 3 consecutive earnings reports.

And the fundamentals explain why this stock has turned into such a monster...

SanDisk's revenues surged 251% YoY, while non-GAAP EPS came in at $23.41, far ahead of guidance for $12 to $14.

In addition, gross margin exploded to 78.4%, and the company generated nearly $3 billion in adjusted free cash flow during the quarter.

This is one of the hottest growth stories in the entire market, and the biggest driver is the data center business.

During the quarter, data center revenues grew 233% sequentially to roughly $1.5 billion.

And the management team made it clear that NAND flash is becoming a critical piece of AI infrastructure as workloads shift toward inference, retrieval-augmented generation, deep reasoning, and agentic systems that require low-latency storage at scale.

In other words, the AI trade is not just about GPUs anymore. As models get bigger and usage becomes more persistent, the storage layer becomes more valuable too.

What's more, SanDisk is also doing something that could make this business far less cyclical than the old memory-stock playbook. The company has signed 5 multi-year supply partnerships backed by financial guarantees, with the longest contract extending 5 years.

These agreements include more than $11 billion in financial guarantees and are designed to create certainty in demand, supply assurance, and more durable margins over time.

With the fundamentals and technicals decisively pointing higher, we expect SNDK to continue leading the market and reach new all-time highs.

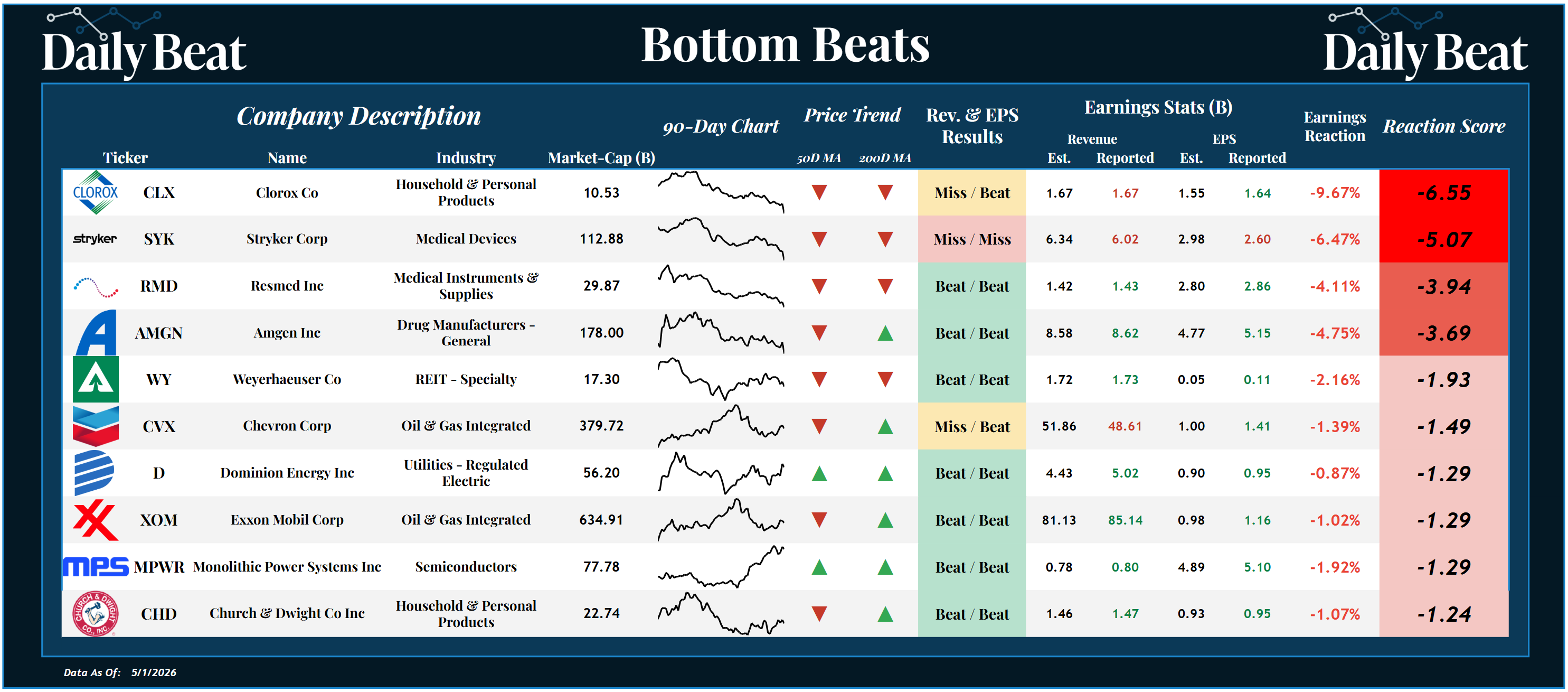

Now flip to the other side of the tape, and the Bottom Beats sheet told a much uglier story.

*Click the image to enlarge it

Clorox $CLX had the worst reaction of the day, falling nearly 10% for its worst earnings reaction since February 2022.

ResMed $RMD and Amgen $AMGN both sold off despite double beats.

And Chevron $CVX and Exxon Mobil $XOM were punished as well, even though the headline numbers looked fine.

CVX snapped a 2-quarter streak of positive earnings reactions, while XOM continued one of the worst earnings sentiment trends in the S&P 500, now getting punished for 10 of its last 12 reports.

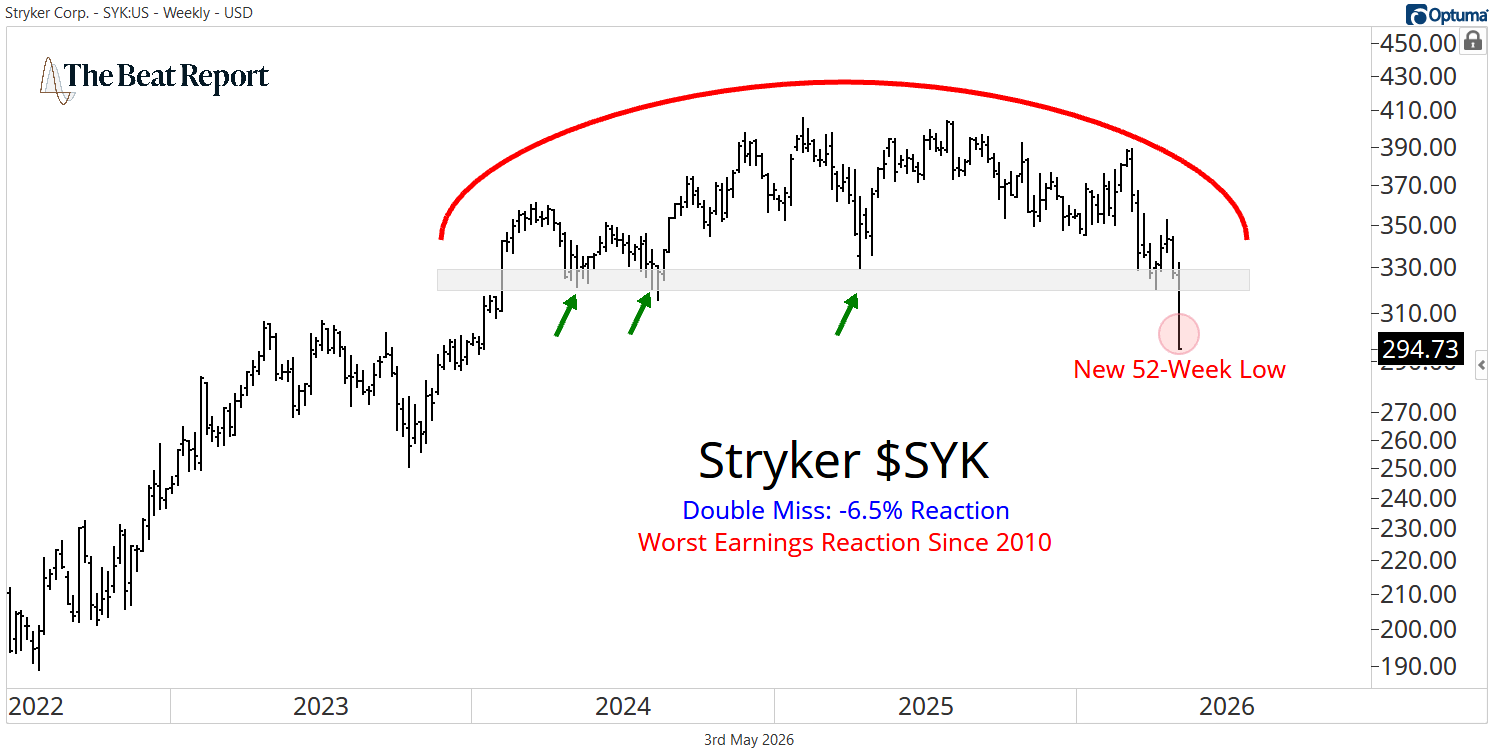

There were plenty of ugly reactions, but the one that stood out the most was Stryker $SYK.

Unlike many of the names on the Bottom Beats sheet, Stryker actually missed headline expectations across the board.

And as a result, the stock fell 6.5% and suffered its worst earnings reaction since 2010.

In addition, Stryker decisively resolved a multi-year distribution pattern and entered a brand-new primary downtrend.

Turning to the earnings report, it's clear why the market reacted so harshly.

Stryker’s net sales increased just 2.6%, and its adjusted EPS fell 8.5%.

But that's not all... The company's operating margin also contracted by 180 basis points.

The management team blamed much of the weakness on a cyber incident that disrupted business operations late in the quarter, delaying shipments and revenue recognition while also pressuring manufacturing absorption.

They said that the underlying demand environment remains healthy, with solid procedural volumes, steady hospital capital spending, and elevated capital order books.

As a result, they maintained full-year guidance for 8% to 9.5% organic sales growth and adjusted EPS of $14.90 to $15.10, arguing that much of the lost first-quarter sales should be recovered throughout the rest of the year.

But the market did not care...

And that is the point.

Management teams can lie, but price never does.

So we're giving the market the benefit of the doubt, and steering clear of SYK until it can reclaim the key 320 level.

At the Premium Beat Report, we’re tracking these reactions in real time using our proprietary reaction score to identify the stocks where technicals and fundamentals are aligned.

These are the trends we’re actively trading, and they’re the ones that can generate 3x, 5x, even 10x returns over time.

May the 4th be with you,

-The Beat Team

Editor's Note: Every day, Spencer sits across from some of the smartest analysts and traders in the business and listens to their best ideas.

So we built the SMTV Portfolio to put real money behind these ideas.

This includes long-term core positions, swing trades, and options.