Following a big double beat, Dell Technologies $DELL rallied more than 30% for its best earnings reaction ever. The company delivered record revenue of $43.84 billion, up 88% YoY, while non-GAAP EPS surged 214% over the same period.

In reaction to mixed headline results, Costco $COST fell 3.9%, confirming a failed breakout to new all-time highs. During the quarter, the company grew net sales by 11.6% YoY, while comparable sales rose 9.8% over the same period.

There were no new S&P 500 earnings reactions, so we wrote about one of our favorite software stocks. Its name is Okta $OKTA.

The company plays a critical role in enabling AI agents, and the stock is on fire. It's in the process of putting the finishing touches on a textbook bearish-to-bullish reversal pattern, and earnings sentiment is serving as a major tailwind.

After crushing the market's headline expectations, Hewlett Packard Enterprise $HPE rallied nearly 20% for its best earnings reaction ever. In their latest report, HPE reported record revenue of $10.68 billion, up 40% YoY, while non-GAAP earnings per share increased 108% over the same period.

On the flip side, Dollar General $DG reported mixed headline results and suffered its second consecutive negative earnings reaction. While it's not ready yet, we believe DG is shaping up for a new primary uptrend.

In reaction to a big double beat, Medtronic $MDT rallied nearly 6% for its best earnings reaction since 2018. Medtronic delivered 9.9% YoY revenue growth and posted its strongest annual top-line performance in 10 years.

Despite beating the market's headline expectations, Palo Alto Networks $PANW fell 5.6% for its third consecutive negative earnings reaction. While this was a good overall report, it wasn't enough to beat the market's expectations.

Despite crushing its top- and bottom-line expectations, Broadcom $AVGO cratered 12.6%, marking its worst earnings reaction ever. In its latest report, Broadcom reported 48% YoY revenue growth, while AI semiconductor revenue surged 143% over the same period. What's more, the management team guided Q3 AI semiconductor revenue to $16 billion, up more than 200% YoY.

Following a big double beat, CrowdStrike $CRWD fell 3.8%, snapping a streak of three consecutive positive earnings reactions. The company delivered record Q1 net new ARR of $256 million, record free cash flow of $468 million, and raised full-year net new ARR growth guidance by 520 basis points at the midpoint. However, this wasn't enough to spark a rally in the stock.

What's happening next week 👇

Next week will be lighter than what we have grown used to over the past month, but it will not be quiet.

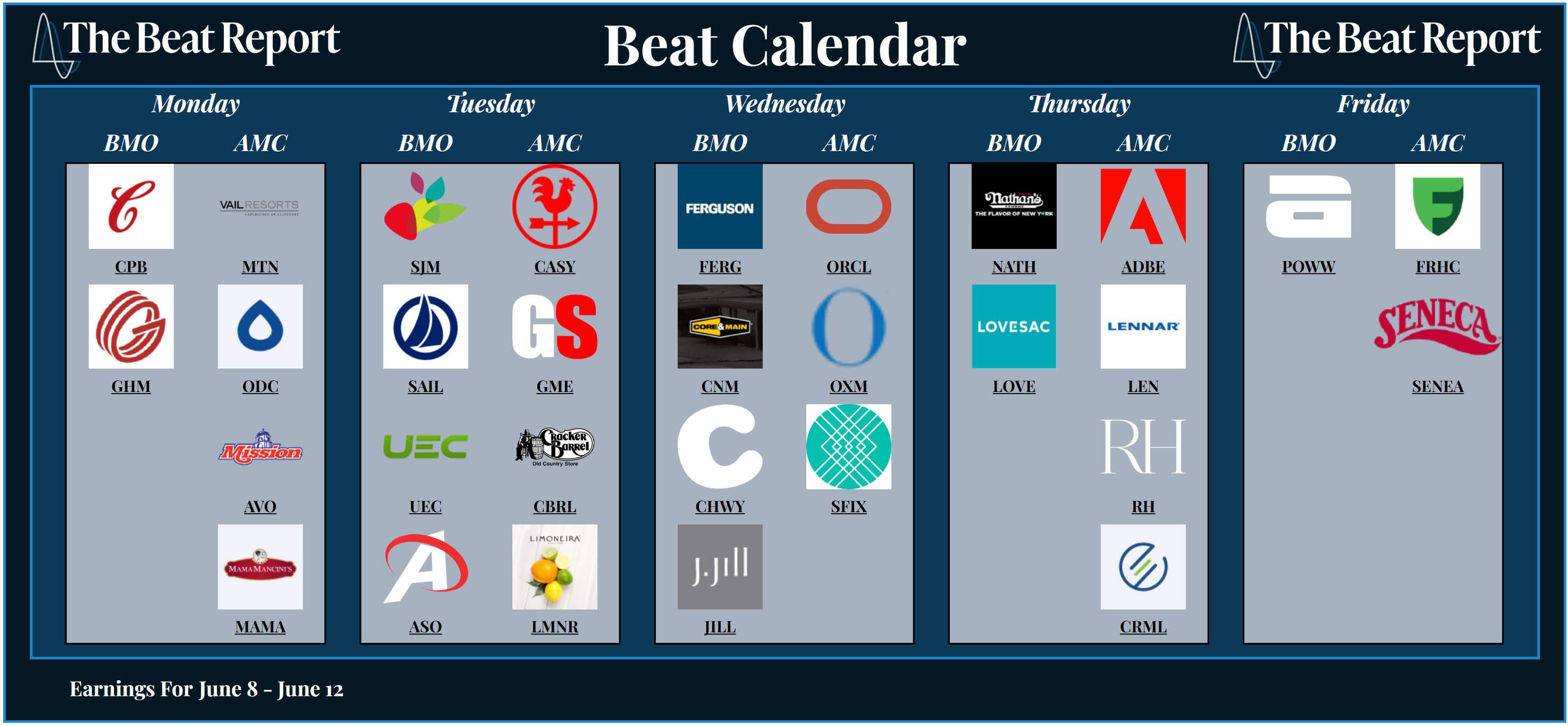

Here's a look at next week's Beat Calendar.

On Monday, we'll hear from Campbell's $CPB and Vail Resorts $MTN.

Then on Tuesday, J.M. Smucker $SJM, Casey's General Stores $CASY, Gamestop $GME, Uranium Energy $UEC, and more will step into the earnings spotlight.

Wednesday brings some of the biggest reports of the week with Oracle $ORCL, Ferguson Enterprise $FERG, and Chewy $CHWY.

Thursday will also be action-packed with fresh reports from Adobe $ADBE, Lennar $LEN, and RH $RH.

There will be plenty to monitor, but the two reports you must keep an eye on are ORCL and ADBE.

Both stocks are trying to tell a comeback story, but only one has earnings sentiment on its side.

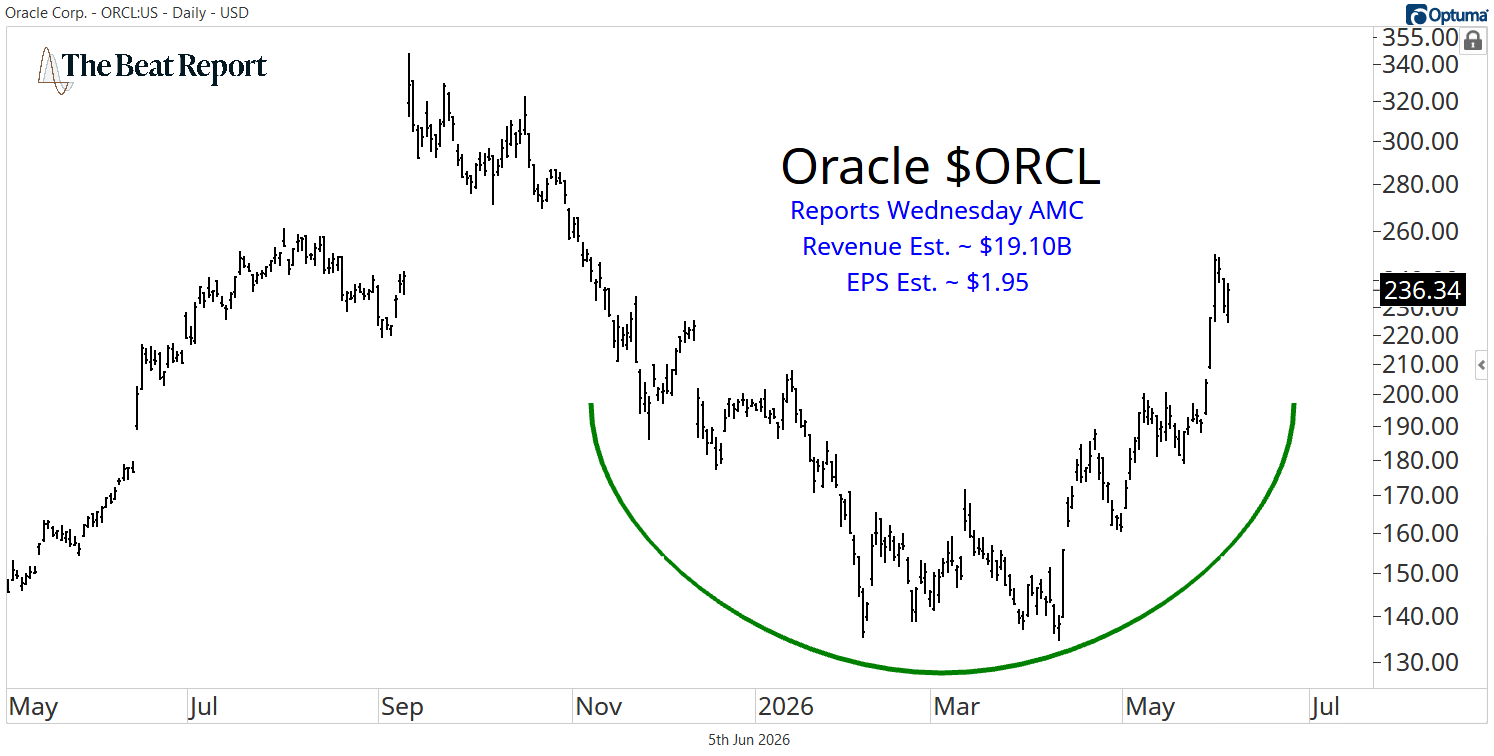

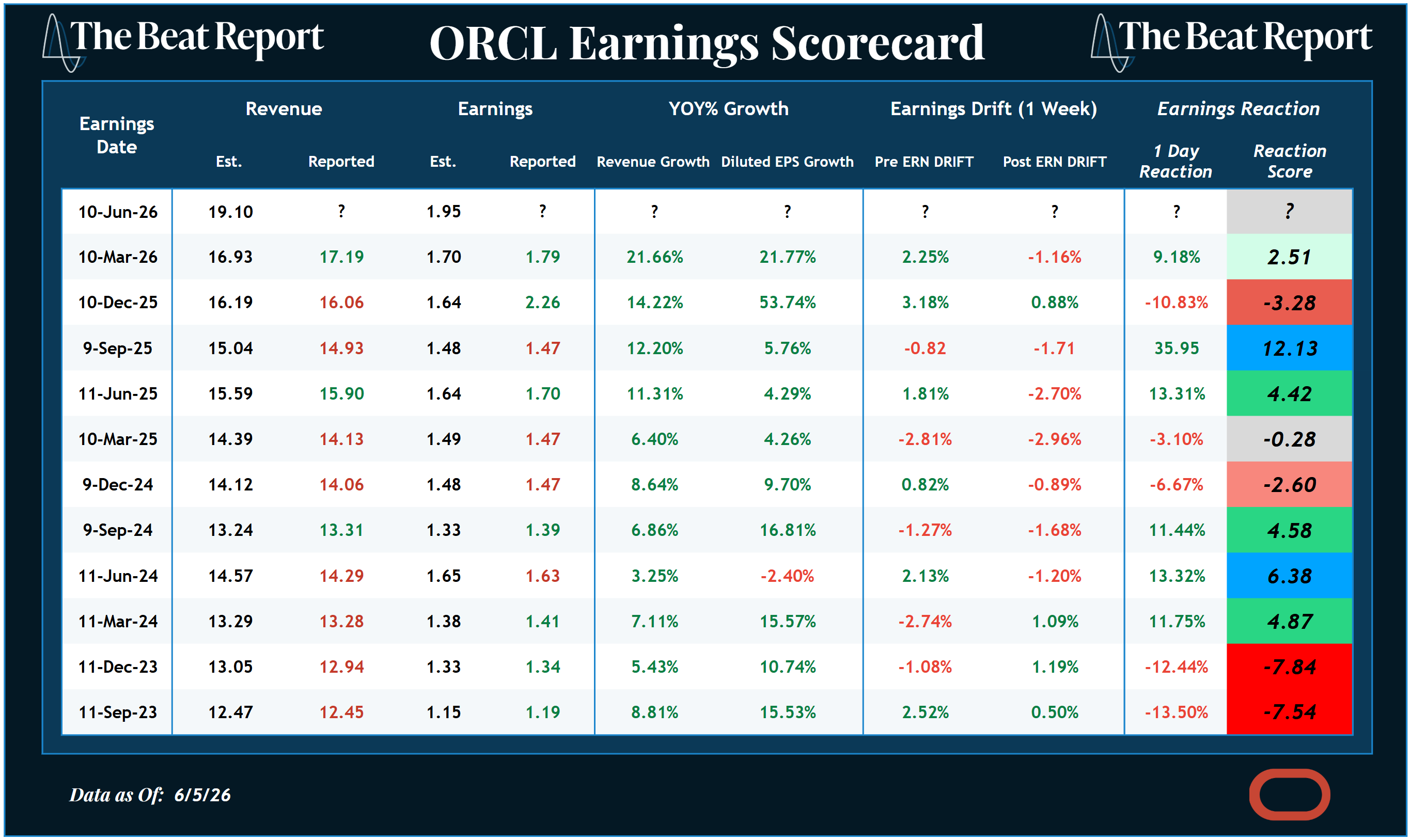

Oracle reports after Wednesday’s closing bell, and the market is looking for $19.10 billion in revenue and $1.95 in earnings per share.

Heading into the report, ORCL is trading near its highest level of 2026 as it attempts to complete a textbook bearish-to-bullish reversal pattern.

The chart is not quite there yet, but the fundamentals and earnings sentiment are already doing their part.

Oracle has been rewarded for three of its last four earnings reports, including the monster September 2025 reaction when the stock rallied nearly 36% in a single session and posted a reaction score north of 12.

Those are rare readings, and they tell us the market is willing to aggressively reward this company when the numbers land the right way.

The fundamental story explains why.

Last quarter, Oracle reported revenue growth above 20% YoY, led by cloud revenue growth of 44% YoY, and cloud infrastructure revenue growth of 84%YoY.

The company's remaining performance obligations also surged 325% YoY to $553 billion, driven largely by large-scale AI contracts.

This isn't your grandfather’s Oracle...

This is now one of the most important AI infrastructure stories in the market, with demand for cloud computing, AI training, inferencing, multicloud databases, and enterprise applications all pushing in the same direction.

Heading into Wednesday's earnings report, the setup is simple...

The fundamentals are accelerating, earnings sentiment is positioned bullishly, and now we need the chart to confirm.

If Oracle can gap higher and hold near new 2026 highs, the reversal pattern is likely complete, and the path of least resistance shifts higher.

If it fails to rally on another strong report, that would tell us expectations may finally be catching up with the story.

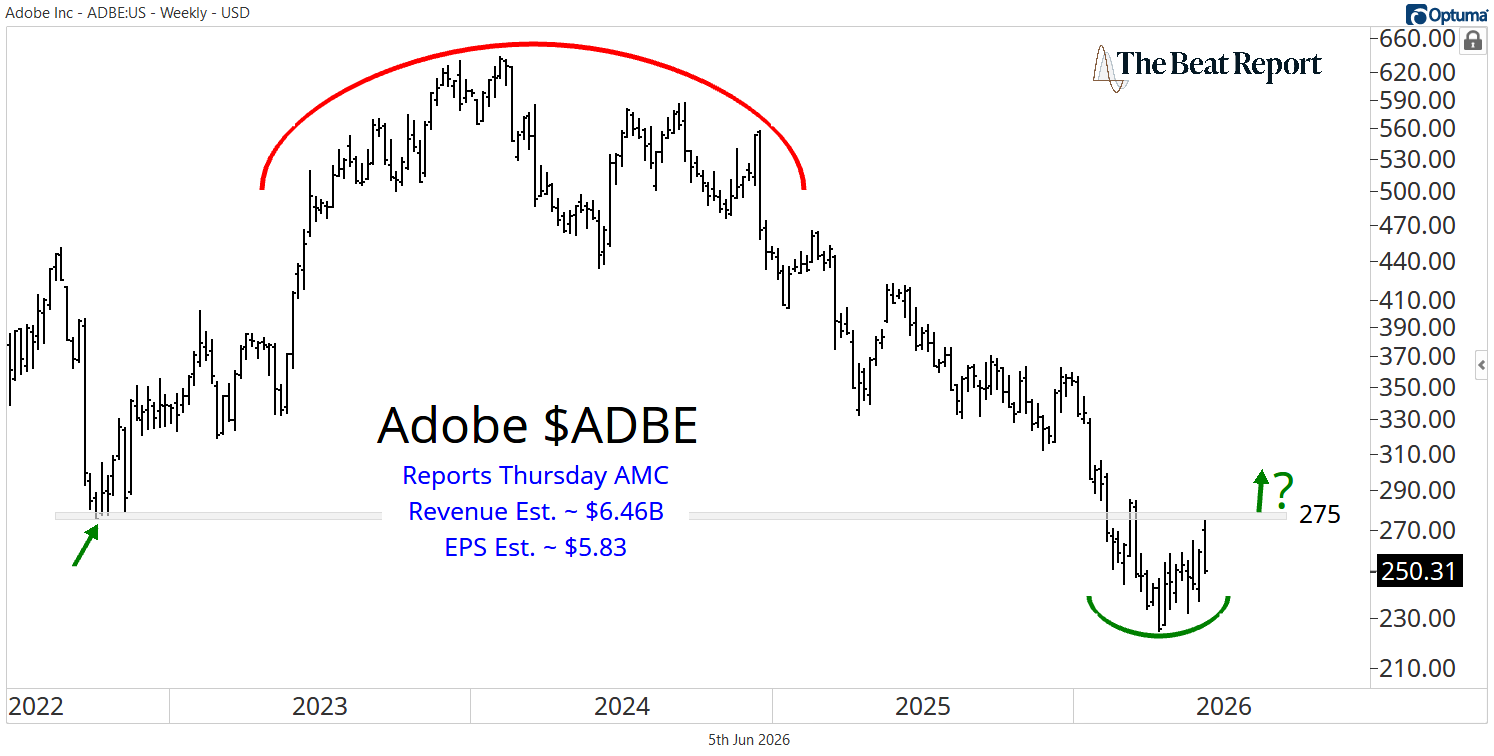

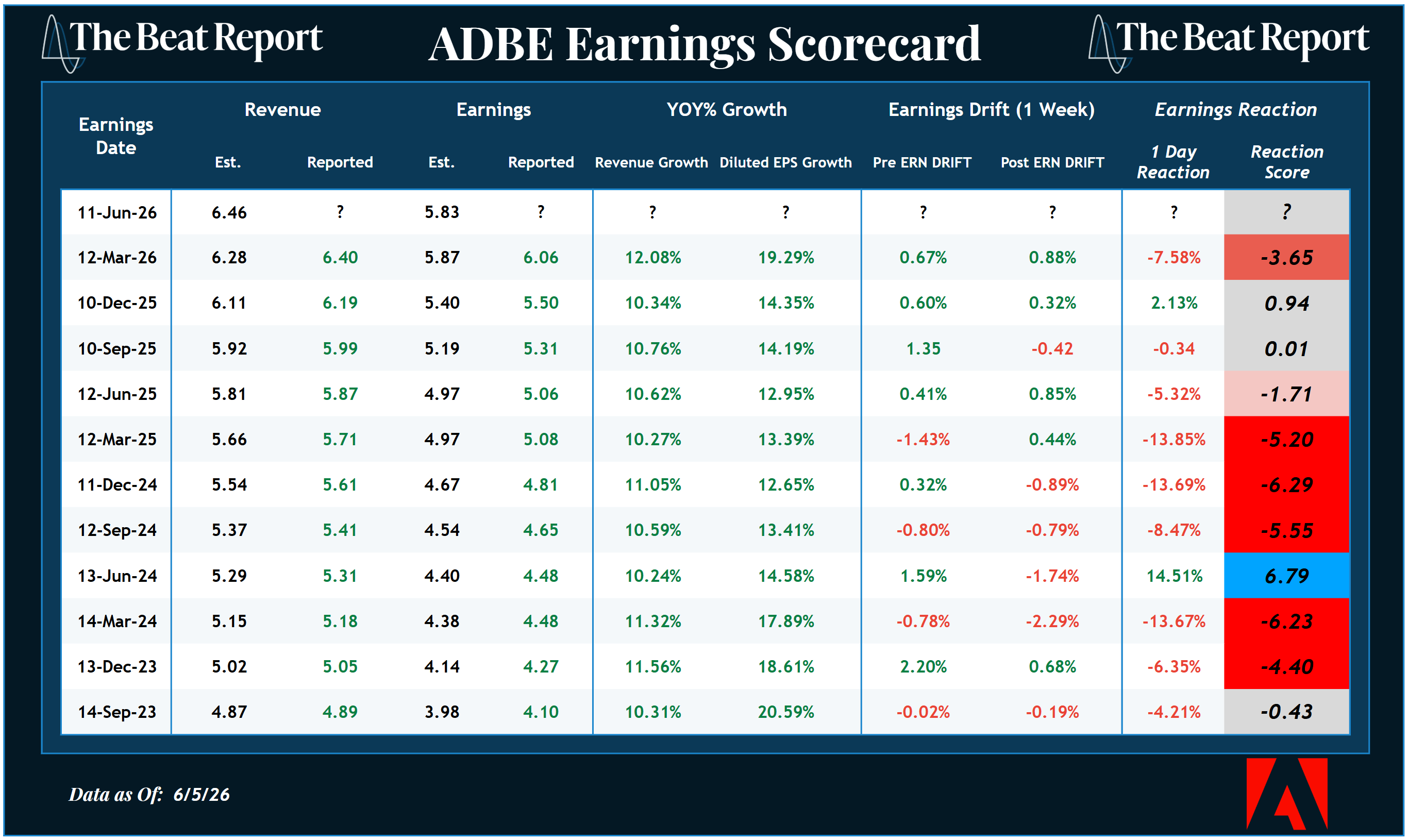

Adobe reports after Thursday’s closing bell, and the market is looking for $6.46 billion in revenue and $5.83 in earnings per share.

Heading into Thursday's earnings report, Adobe is coiling below the 2022 bear market low near $275. That level served as support during the prior cycle, and now it's the line in the sand for this reversal attempt.

Above $275, the squeeze is on.

And below it, ADBE remains vulnerable to another failed rally and a fresh leg lower.

That makes this report a big deal not just for Adobe but for the broader software industry, as Adobe is one of the largest software stocks in the market.

If buyers finally reward the stock and push it back above that former breakdown level, it would be a major vote of confidence for software bulls.

The problem is earnings sentiment...

Unlike Oracle, Adobe has not been rewarded consistently.

In fact, it has been punished for six of its last seven earnings reports, even though it almost always beats headline expectations. That is the key issue here.

The market is not asking whether Adobe can beat.

It probably will.

The real question is whether the market finally cares.

Fundamentally, Adobe's business is in better shape than the stock suggests.

Last quarter, the company delivered record revenue of $6.40 billion, up 12% YoY, while non-GAAP EPS was up 19% over the same period.

Subscription revenue grew 13%, operating cash flow hit a record Q1 level of $2.96 billion, and AI-first ARR more than tripled YoY.

Management is also pushing hard into AI across Creative Cloud, Acrobat, Express, Firefly, GenStudio, and customer experience orchestration.

Adobe said it surpassed 850 million monthly active users across Acrobat, Creative Cloud, Express, and Firefly, with 17% YoY growth, giving the company a massive user base to monetize as AI adoption expands.

So the fundamentals are definitely not the issue here.

The chart and earnings sentiment are.

Adobe has revenue growth, EPS growth, and an AI product story. What it doesn't have yet is a market willing to reward those numbers.

But that could change this week...

If Adobe reports another double beat and finally rallies through $275, it would mark a major change in character and potentially complete a bear trap below a key level of interest.

But if ADBE fails there again, the stock will remain one of the most frustrating software laggards in the market.

If you want access to our next trade, join our growing community at the Premium Beat Report.

We hope you enjoyed this post,

-The Beat Team

Editor's Note: Reading about ideas and acting on them are two different skills.

The SMTV Portfolio is where Spencer Israel takes the best of what crosses his desk from across the analyst network and trades it with real money. You can see every entry, every exit, in front of you.