The dollar is rebounding, but don’t expect it to last

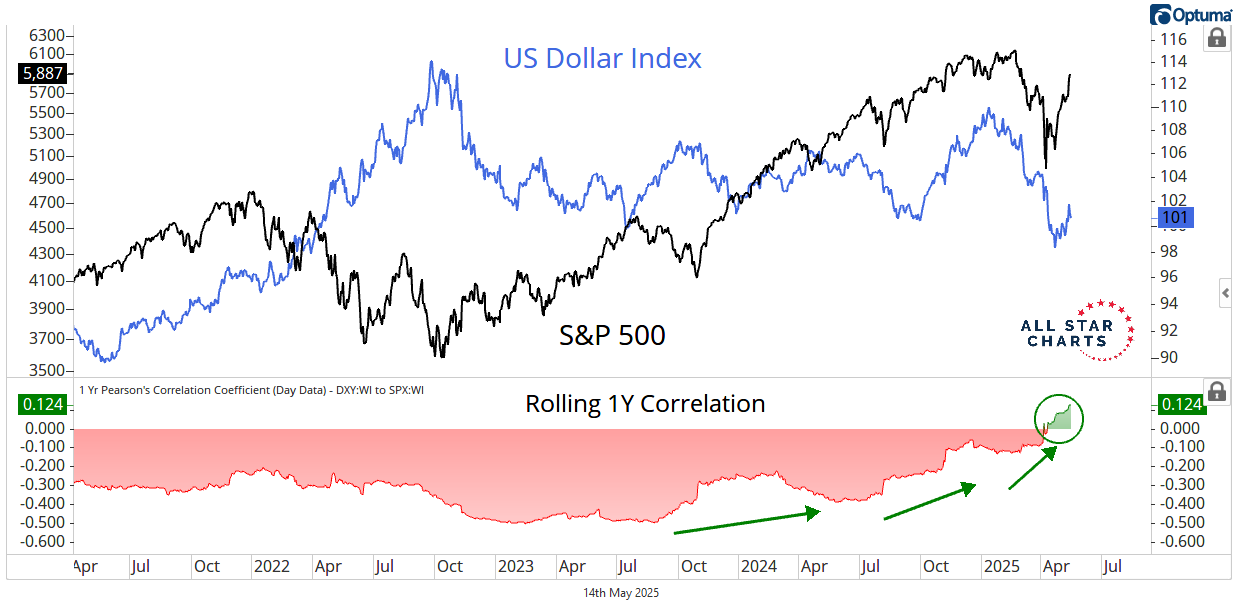

The US Dollar Index $DXY continues to sit near the top of our macro checklist.

It’s been one of the more important tells of the cycle, not just for currencies—but for equities, commodities, and global risk assets.

Traditionally, the dollar moves opposite to US stocks. But as technicians, we know better than to marry intermarket correlations. These relationships ebb and flow, strengthen, weaken, invert, and sometimes go completely quiet. That’s normal.

Late last year, a big shift took place as stocks began to move with the dollar. It's not typical, but it’s not without precedent either.

A few months later, when the dollar rolled over, it ignited leadership from ex-US equities. International stocks started to outperform the S&P and Nasdaq for the first time in decades.

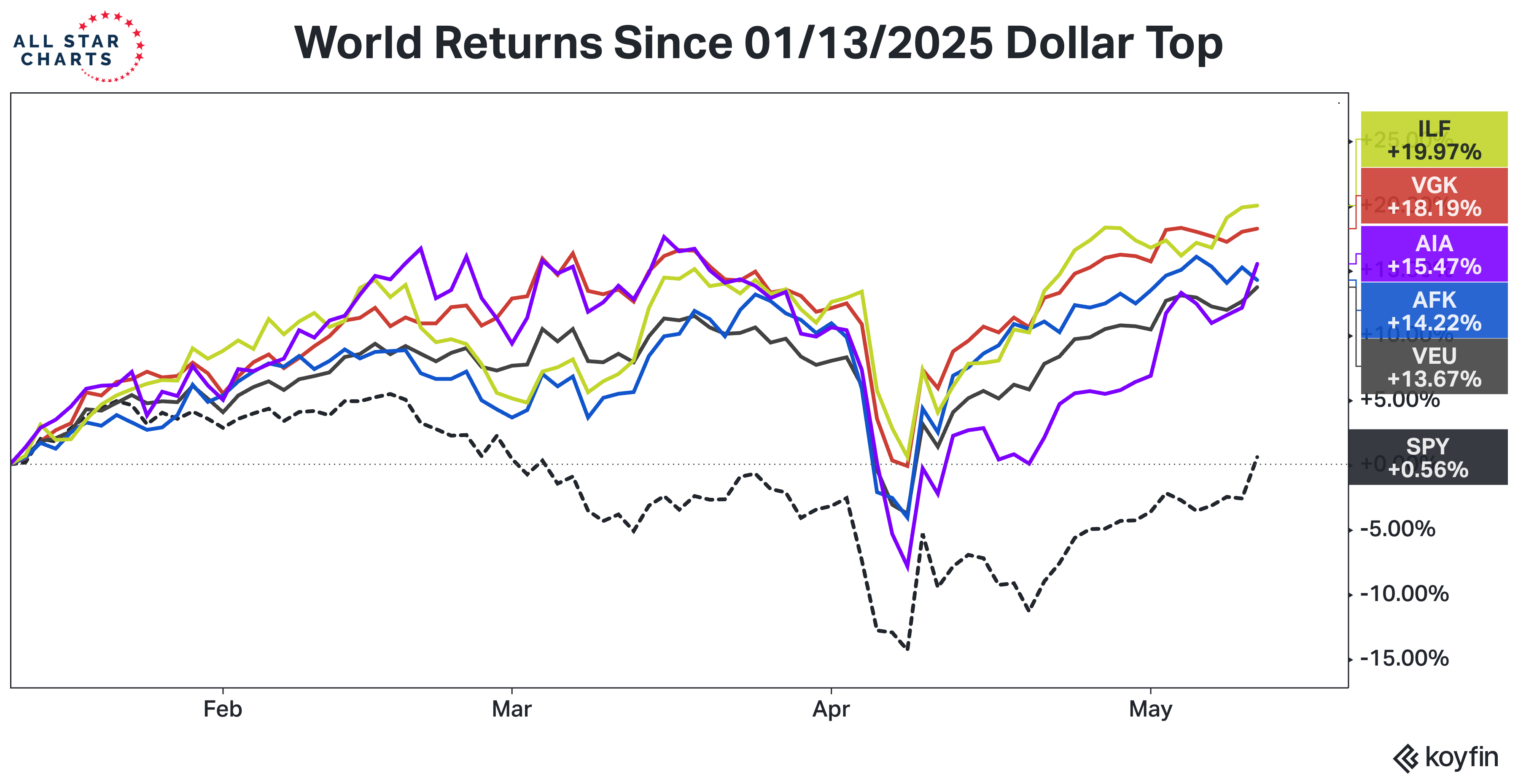

Here’s a look at that performance gap since the dollar peaked.

The S&P has been flat while Europe is up 18%.

With global rotation underway, we must now ask ourselves: was the breakdown in the DXY a head fake? Or is this current rally just a garden-variety retest before another leg lower? Remember: Retests are common after big moves.

Our thesis is simple: we’re in the early innings of a new “weak dollar" cycle.

No, that doesn’t mean the dollar is being replaced by gold, Bitcoin, BRICS, or XRP. It just means there are likely better opportunities elsewhere—particularly in non-dollar assets and international equities.

We just need price to confirm that view and the DXY to put the finishing touches on this distribution formation.

Let’s talk about the levels that matter.

The first key level is 102.50, which is where the 38.2% retracement of the YTD decline and the VWAP anchored to the YTD highs come into play. If the rally stalls here, it tells us the bounce is weak and the broader downtrend is likely to resume in force.

However, another scenario is a continued squeeze toward the 105 zone. This area represents serious overhead supply—a confluence of key retracement levels and anchored VWAPs.

If DXY rips through that zone with strength, we’ll have to reassess the whole weak dollar theme.

I don’t see it happening, though. More and more foreign currencies are reversing the trend against the dollar with every passing day.

The Thai Baht and Philippine Peso are on the brink of completing textbook reversals.

The Brazilian Real is scooping higher after a failed breakdown.

European currencies like the Swedish Krona look better than they have in several years, with new primary uptrends underway.

Even the Mexican Peso is completing a tactical base and hitting new 6-month highs.

My point is that the dollar is getting killed all across the globe. This isn’t some regional phenomenon.

Currency market internals are clear as day, and they’re telling us to expect lower dollars for longer. We’ve been listening and positioning accordingly.

The best way to do it, in my opinion, is to overweight international stocks. I think this trend is just getting started.

A weaker dollar and non-dollar investment alternatives were among the biggest themes of our Portfolio Accelerator conference this week.

I just love it when all my smartest friends are thinking the same way I am.

You need to have a subscription to access this content in full.

Log in or subscribe today to unlock new features and receive Member Benefits.