Own Something

A Paradigm-backed technology called Across dropped a proposal to dissolve its decentralized organisation (DAO), kill its cryptocurrency, and convert into a traditional U.S. corporation. Holders could swap their ACX cryptocurrency for equity in the new company, or cash out at a 25% premium.

The token doubled on the announcement of its own death.

The team basically said, "hey, this token thing isn't working, want actual equity instead?" And everyone enthusiastically said yes.

That tells you everything about where we are right now.

Six weeks ago I called for The Ownership Cycle. The argument was simple: most cryptos don't entitle you to anything real: revenues, cash flows, or legal claim on anything the team builds. The only reason to hold is the belief that someone else will pay more later. And I said the gap between tokens that represent genuine ownership and tokens that are just along for the ride was about to get very, very wide.

Across just proved my thesis.

The product wasn't the problem because Across had moved $35 billion in volume. The problem was the structure; enterprise partners need enforceable contracts and revenue deals need a legal counterparty. The kinds of partnerships that would drive the next phase of growth require a setup that a DAO simply can't provide.

And they're not alone. More teams are having this exact conversation behind closed doors. What we've been watching for half a decade now is decentralization theater. Teams adopting DAO structures as regulatory camouflage, not because distributed governance was the right model for their product. Now the camouflage is coming off.

While some projects are ditching tokens entirely, others are proving that tokens can work beautifully, if you design them to actually capture value.

Enter Hyperliquid.

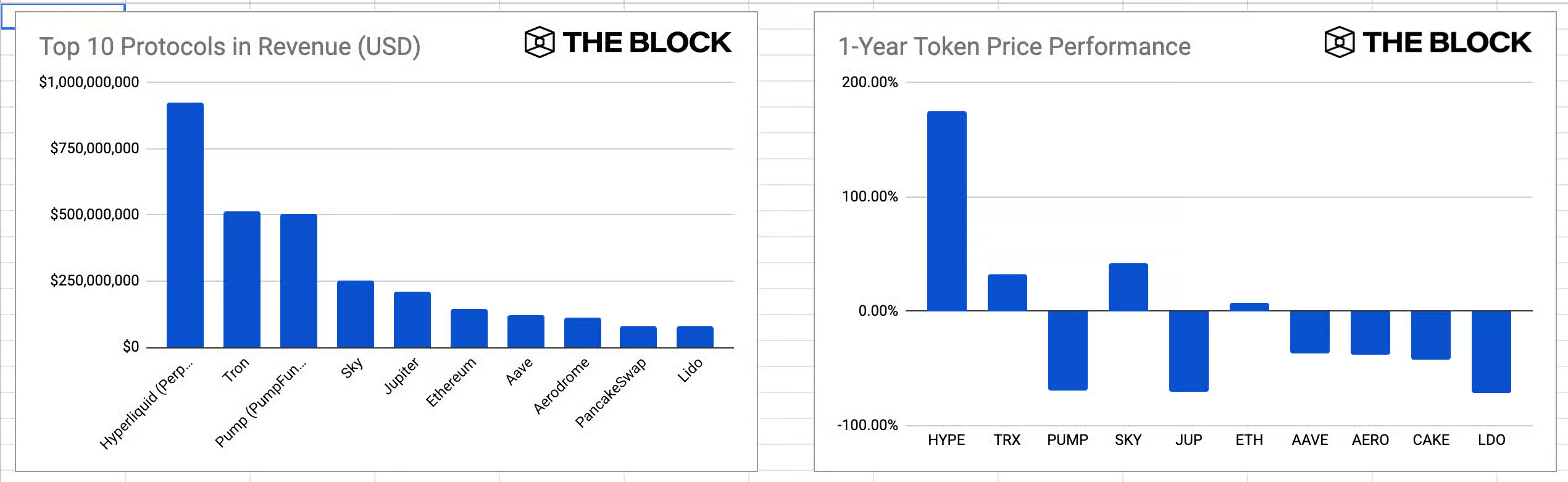

While nearly every major DeFi token has bled out over the past year, Hyperliquid has been a wrecking ball. Hyperliquid is printing $1B in annualized revenue and funneling over 90% of it into buying back and burning it's cryptocurrency.

Just look at the difference between Hyperliquid and the other DeFi coins in terms of its price performance (left) and revenue (right).

When a massive Hyperliquid token unlock hit on March 6, the kind of event that normally craters a price 15-20%, HYPE went up. The buyback machine absorbed the sell pressure in real time.

And three days ago, Grayscale filed with the SEC to launch a HYPE ETF on Nasdaq. They're the fourth major issuer to file, behind Bitwise, 21Shares, and VanEck. Four asset managers racing to give traditional investors access to a DeFi token that's barely eighteen months old. If any of those get approved, it would be the first spot ETF for a DeFi-native token in history.

Nobody's filing ETFs for AAVE, UNI, or LDO. They're filing for the one with the buyback engine. The one that actually returns value to holders.

This is the repricing I was talking about. Not everything going up. The gap blowing wide open between tokens that function like ownership and tokens that function like receipts for a donation.

I used this analogy last time and it still holds. Imagine buying Apple shares, except you have zero claim on revenue, zero claim on assets, and your only right is to vote on proposals that management ignores anyway. You'd call those "shares" a bad joke. That's the deal most token holders have right now, and the market is finally waking up to how absurd it is.

For years, the reason cryptos couldn't share revenue was fear of securities classification. That fear created a generation of deliberately useless investments because doing something might attract the SEC. That excuse is evaporating fast.

So here's the takeaway, same as last time, just louder now.

The crypto market is splitting into two buckets.

- Tokens with explicit value accrual (buybacks, burns, revenue share, fee capture) where when the protocol makes money, you make money.

- And tokens with none of that. Governance rights to a treasury you'll never touch, attached to a product you have no economic stake in.

The first bucket is going to attract institutional capital, ETF wrappers, and long-term holders. The second is going to keep bleeding until there's nothing left. There are too many tokens in this market. What comes out the other side will be fewer names, but higher quality.

Invest in the technologies that accrue value. If a technology generates $500 million and you get none of it, that's not a red flag.

The ownership cycle I proposed isn't a theory anymore.

Across just showed you what happens when a team admits the token isn't working. Hyperliquid is showing you what happens when a team builds one that does. And four asset managers filing ETFs for a single DeFi token is showing you exactly where the smart money wants to go.

If you're on the right side of it, you have the potential to make a lot of money.

Cheers,

Louis Sykes

Senior Crypto Analyst, All Star Charts