Yesterday was a friendly reminder that price is the only thing that pays.

April 2, 2026

The S&P 500 kicked off the first trading session of Q2 with a strong move higher, the kind of start bulls were hoping for as a new quarter gets underway.

But underneath that strength, the earnings tape told a very different story.

We heard from Conagra Brands $CAG and Nike $NKE, and despite what looked like respectable results on paper, both stocks were met with heavy selling.

The market didn’t hesitate... it just sold them relentlessly.

Let’s talk about what happened, starting with the Beat Sheet.

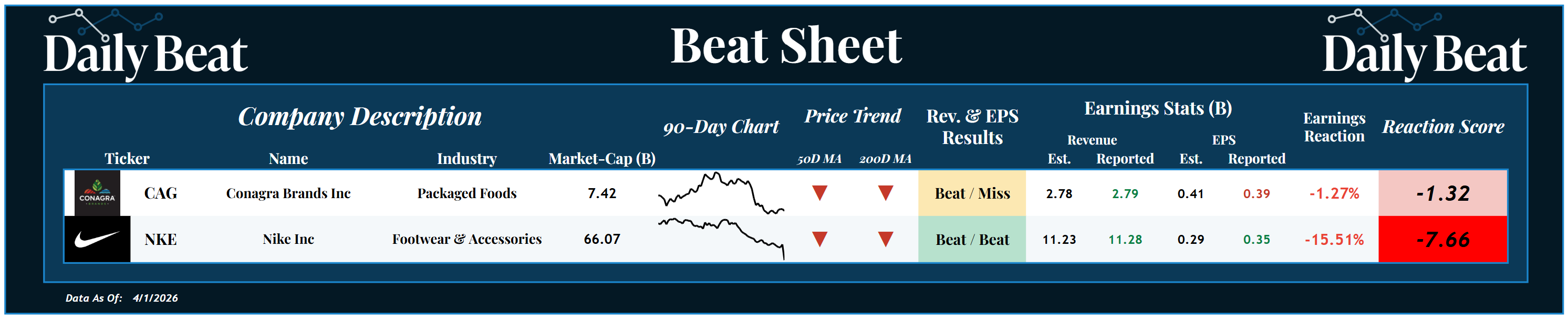

*Click the image to enlarge it

On the Beat Sheet, Conagra delivered a slight revenue beat but came up short on earnings. This resulted in a reaction score of -1.3.

On the other hand, Nike posted a clean double beat, exceeding expectations on both revenue and EPS, yet the stock was punished by more than 15%.

When a company beats across the board and still gets hit like that, it’s not about the quarter anymore. It’s about positioning, sentiment, and most importantly, the primary trend.

Price is telling us everything we need to know.

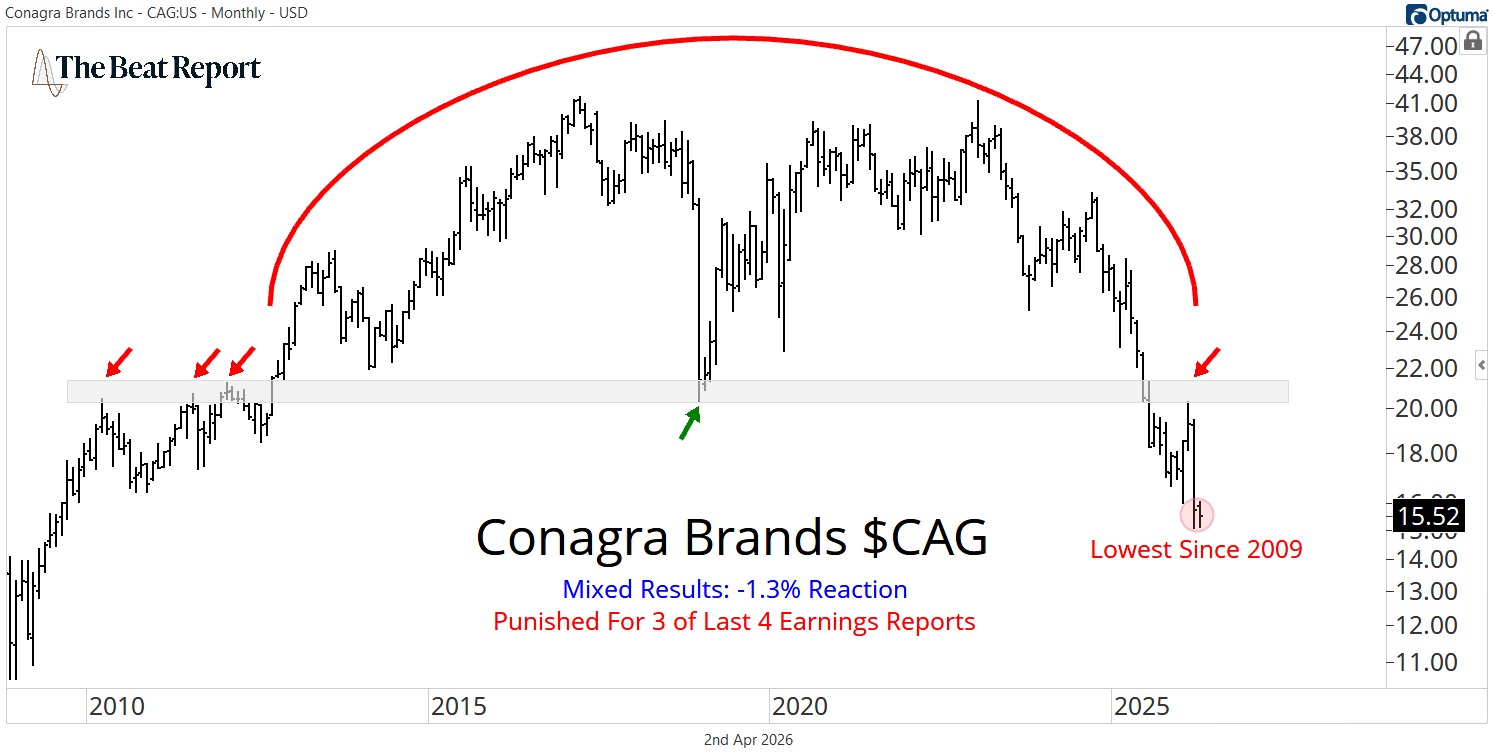

Starting with Conagra, the pattern is becoming undeniable.

Wednesday marked the 3rd negative earnings reaction in the last 4 quarters, and that consistency matters. Markets build habits, and right now the habit is to sell this name every time it reports earnings.

The stock is now trading at its lowest level since 2009, which is staggering, given that it was flirting with new all-time highs just a few years ago.

Nearly two decades of price history have been unwound, and that kind of structural damage doesn’t get repaired overnight.

The company has made progress in pockets, particularly in its frozen and snacks businesses, where volumes have been improving, and organic sales have returned to growth.

That said, the path to get there hasn’t been smooth...

Management has leaned into a volume-first strategy, accepting margin pressure along the way, and they continue to emphasize flexibility as inflation and consumer behavior remain uncertain.

When you combine weakening fundamentals with a stock already in a confirmed downtrend, the outcome tends to be the same. Lower highs and lower lows.

And until something materially shifts, there’s no reason to expect anything different.

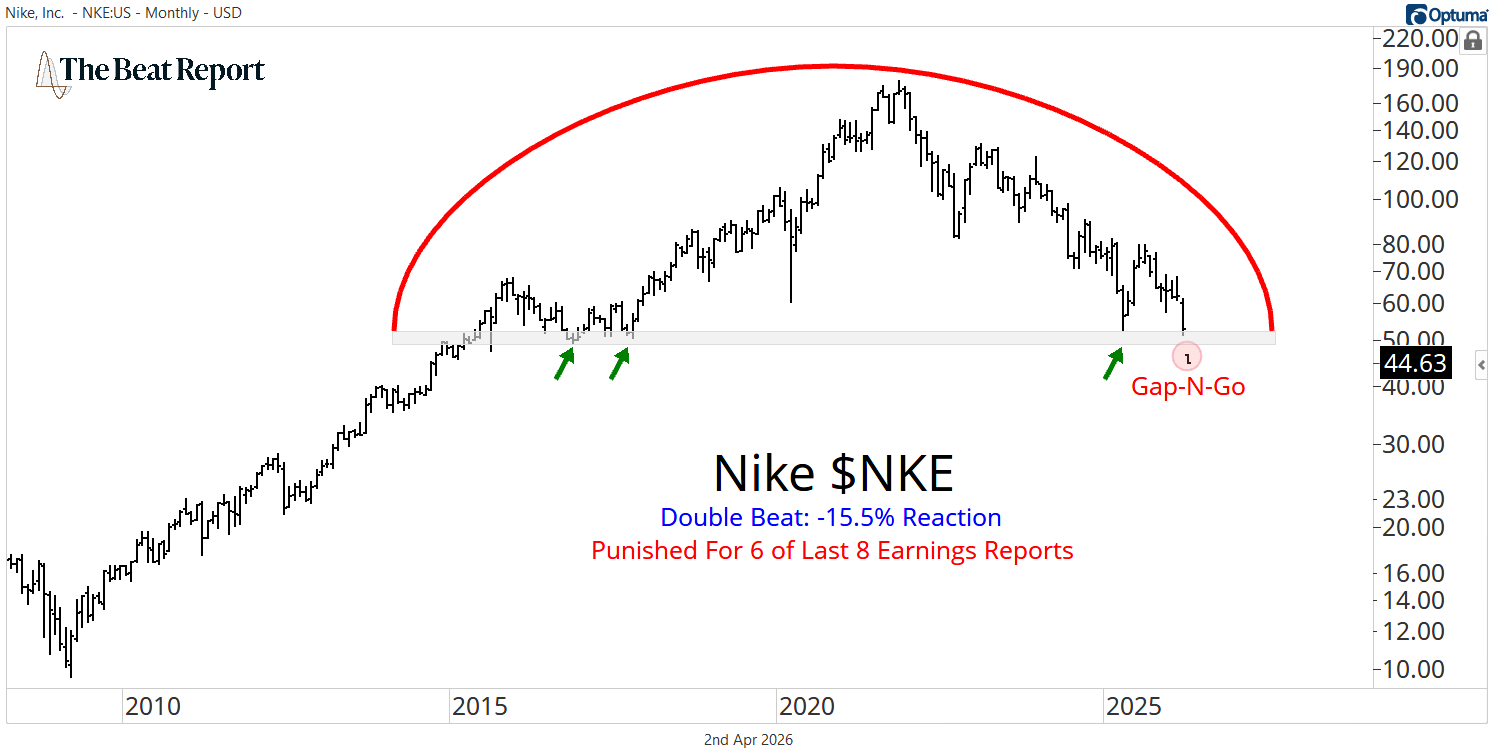

Nike tells a similar story, but in a much more dramatic way.

At first glance, the quarter looked solid. Revenue came in ahead of expectations, earnings beat estimates, and management continues to articulate a clear turnaround plan.

But the market didn’t care...

The stock dropped sharply, extending an already persistent pattern of negative earnings reactions.

And technically, the damage is severe.

Nike has spent the better part of the last decade carving out a massive topping formation, and that structure has now resolved to the downside.

The former support around 50 has been decisively broken, and as long as the stock remains below that zone, it represents overhead supply rather than a floor.

This is not a correction within an uptrend. It's the early stages of a new primary downtrend, and those tend to last longer than most participants expect.

The fundamentals help explain why the market is so unforgiving.

Management is in the middle of a deliberate reset, removing excess inventory from the marketplace, which created a significant headwind this quarter.

It’s a necessary move to clean up the business, but it comes at the cost of near-term performance.

At the same time, profitability has declined meaningfully, with net income falling from roughly $794M to $520M year-over-year despite relatively flat revenue.

In other words, this is a transition period.

The foundation may be improving, but earnings power hasn’t caught up yet, and the market isn't willing to wait while that process plays out.

That’s the common thread between these two names.

The broader market may be rallying, but when stocks are in established downtrends, earnings become catalysts for selling rather than buying.

People lie, narratives change, management teams spin their stories, but price cuts through all of it.

And right now, price is pointing lower for CAG and NKE.

That’s exactly why we focus on the intersection of earnings and primary trends in the Premium Beat Report.

We’re not interested in guessing which turnaround might work or which narrative sounds compelling. We want the stocks where the fundamentals and technicals are aligned and moving in the same direction.

Because those are the ones that pay.

Thank you for reading,

-The Beat Team

P.S. Sam Gatlin and Jason Perz will be joined by JC Parets for a live session called "Making Money from Inflation" today at 2 pm ET.

It's all about trading commodities. It's free, live, and we’ll have plenty of time for Q&A at the end.