Earnings reactions are making the playbook simple again.

April 30, 2026

Yesterday was the most action-packed session of earnings season so far.

We heard from 49 S&P 500 companies, and the reactions were all over the map.

Some stocks barely moved, others exploded higher, and plenty got absolutely crushed.

It was a clean split between winners and losers, but more importantly, it was a reminder that this market is getting increasingly selective.

With trillions in market cap already reporting and even more still to come, price is doing a phenomenal job of telling us exactly which stories deserve higher prices and which ones don’t.

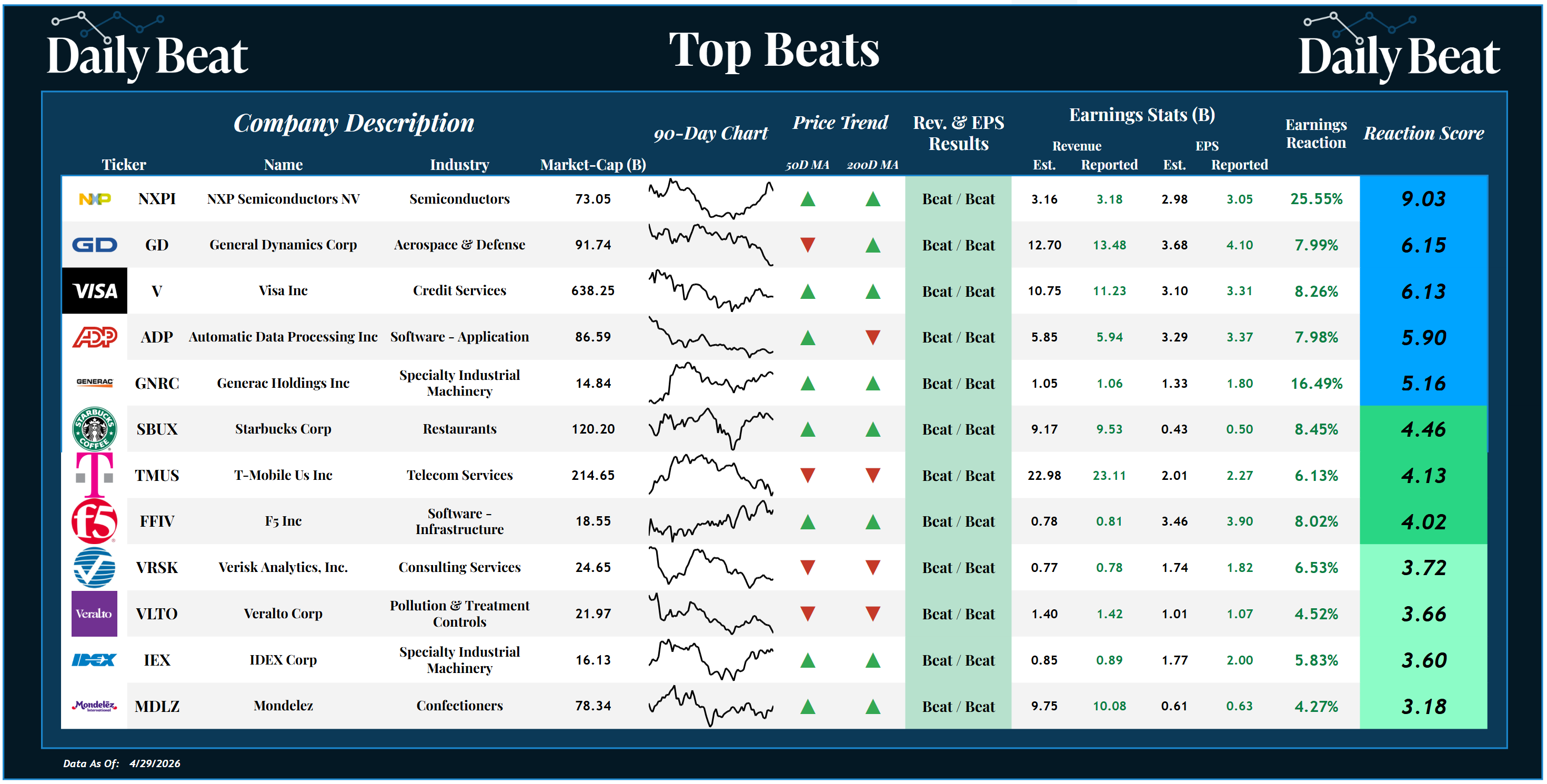

Looking at the Top Beats sheet, one thing stands out immediately. Every single name on that list beat expectations on both revenue and earnings.

*Click the image to enlarge it

That’s not a coincidence...

When the fundamentals are strong across the board, the market is far more willing to reward those stocks, and we saw that with some very important names.

Aerospace and defense showed up with strength in General Dynamics $GD, payments held firm with Visa $V, enterprise software and services delivered through Automatic Data Processing $ADP and F5 $FFIV, and even consumer-facing names like Starbucks $SBUX participated.

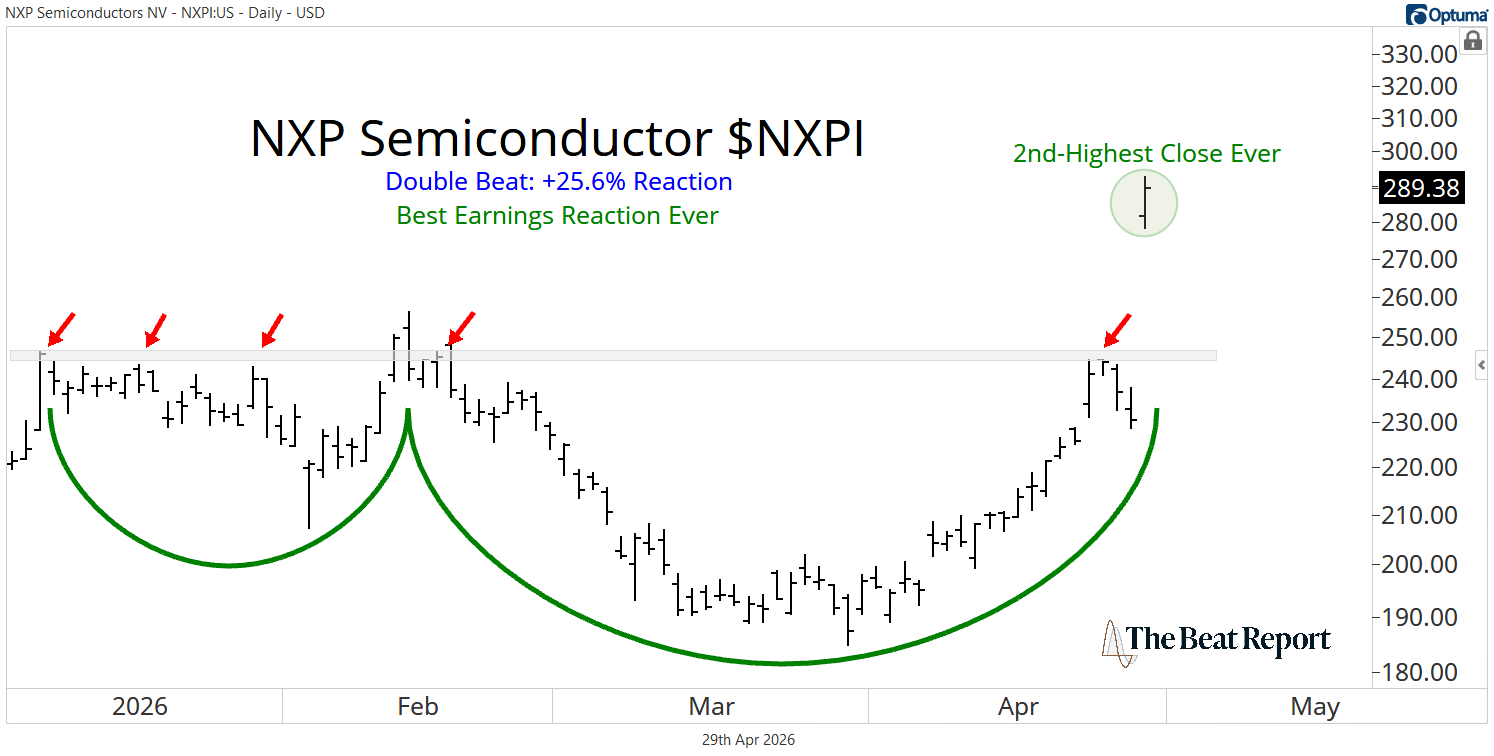

But the most important reaction, by far, came from NXP Semiconductor $NXPI.

NXPI rallied more than 25% for its best earnings reaction ever and closed at the 2nd-highest price in its history.

From a technical perspective, this was a textbook gap-and-go move as the price cleared a well-defined shelf of highs from earlier this year and never looked back.

And what makes this even more compelling is how actionable it is. The 2024 peak is a clean and clear level to define risk against and take a swing at NXPI.

Yes, the stock is extended in the very short term after a move like that, but structurally, this looks like the early innings of something much bigger.

Now layer in the fundamentals, and the story only gets stronger.

NXP delivered12% year-over-year revenue growth and showed broad-based strength across all of its end markets.

What’s really important here is that the growth isn’t coming from one isolated segment. It’s expanding across automotive, industrial IoT, communications infrastructure, and even data center exposure, which management highlighted as an increasingly meaningful opportunity.

The automotive segment continues to benefit from software-defined vehicles and electrification trends.

Meanwhile, the industrial segment is seeing a surge driven by automation and physical AI, and data center exposure is ramping up faster than expected.

So when you combine a powerful fundamental backdrop with a clean technical setup and a historic earnings reaction, you get a stock that has the potential to trend much higher over the coming months.

NXPI is the kind of stock we want to be involved with here at The Beat Report.

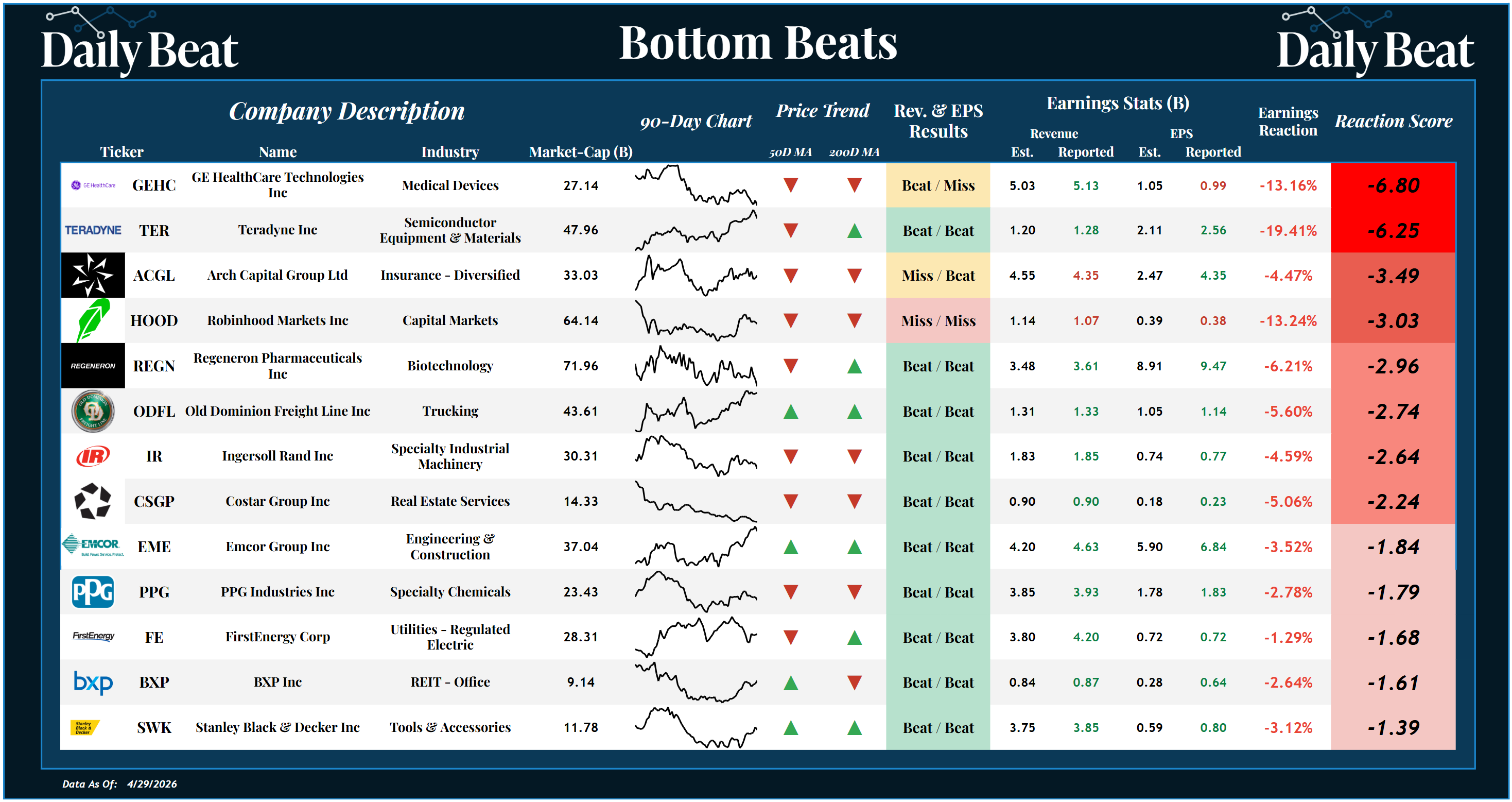

On the other side of the spectrum, the Bottom Beats sheet told a much different story.

*Click the image to enlarge it

There were plenty of ugly reactions across a wide range of industries, and interestingly, several of them came from companies that actually beat expectations.

This tells us the reaction had less to do with the numbers and more to do with positioning, expectations, and the market's interpretation of the story.

The most notable example of that was GE HealthCare $GEHC.

After reporting mixed results, GEHC collapsed by more than 13%, marking its 2nd-worst earnings reaction ever.

And from a technical perspective, this couldn’t have come at a worse time.

GE HealthCare has been carving out a massive distribution pattern over the past year, and now it's on the cusp of breaking down.

In the very short term, could this level hold and produce a bounce? Sure.

The stock is extremely oversold after a move like that, and it wouldn’t be surprising to see some kind of relief rally.

But stepping back and looking at the bigger picture, the trend is clearly lower, and the sellers remain in control.

And when you look under the hood, the fundamentals help explain why.

Yes, the company delivered solid top-line growth, with revenue coming in at the high end of expectations and strength across key segments like imaging and pharmaceutical diagnostics.

Demand remains healthy globally, with strong order trends and backlog supporting future growth.

But the problem isn’t the revenue... It’s profitability.

Margins came under pressure due to rising input costs, including a roughly $100 million increase in memory chip pricing and another $100 million tied to oil and freight costs. This forced the management team to lower its full-year profit and free cash flow guidance.

That’s the kind of shift the market does not take lightly, especially for a stock that was already struggling.

So while the business still has solid demand and long-term innovation potential, the near-term headwinds are very real, and the market is repricing the stock accordingly.

If GEHC breaks below last year's low, we expect it to fall another 10% and retest its all-time low at $53.

At the Premium Beat Report, we’re tracking these reactions in real time using our proprietary reaction score to identify the stocks where technicals and fundamentals are aligned.

These are the trends we’re actively trading, and they’re the ones that can generate 3x, 5x, even 10x returns over time.

We hope you're enjoying this earnings season as much as we are,

-The Beat Team

Editor's Note: What if you could make a day's pay before lunch, with as little as $2,000?

That's exactly what Kenny Glick is showing traders on Wednesday, May 6th at 4:15 pm ET in a FREE live training.