Following a big double beat, Ross Stores $ROST rallied more than 8% for its fourth consecutive positive earnings reaction. The posted YoY sales and earnings per share growth of 21% and 37%, respectively. And the management team raised its forward guidance across the board.

Despite beating the headline expectations, Take-Two Interactive $TTWO fell 4.4%, marking its fifth consecutive negative earnings reaction. With the upcoming release of Grand Theft Auto VI, the management team expects 2027 to be a record year. But the market isn't buying the story...

After reporting mixed headline results, AutoZone $AZO cratered 9% for its sixth consecutive negative earnings reaction. The stock is now trading at the lowest level since 2024.

Net sales rose 8.4% YoY, which was the company’s largest sales increase in more than three years. However, the market isn't rewarding that growth right now.

There were no new S&P 500 earnings reactions to cover, so we highlighted one of our favorite opportunities in the consumer discretionary sector.

Lindblad Expeditions $LIND is breaking out of a massive base and printing fresh all-time highs after posting one of its best earnings reactions ever on May 5. In the report, occupancy jumped to 93% from 89%, and net yield per available guest night climbed 7% to $1,631, which was a new record for the company.

In reaction to a big double beat, Agilent Technologies $A rallied nearly 17% for its best earnings reaction since 2002. The company expanded its operating margin by 130 basis points YoY, while increasing revenues by 10% over the same period. And the management team raised its forward guidance across the board.

Despite reporting a double beat, Synopsys $SNPS fell 8.6%, marking its seventh negative earnings reaction out of the last eight quarters. This company is a critical pick-and-shovel business in the chip design world, but earnings sentiment has been a major headwind over the past two years.

What's happening next week 👇

Next week will be lighter than what we have grown used to over the past month, but it will not be quiet.

The busiest stretch of earnings season is behind us. The mega-cap flood has passed. The S&P 500 has already heard from the vast majority of its components, and the market has given us a pretty clear message about what it wants to reward.

AI infrastructure is still leadership.

Cybersecurity is still leadership.

Software is trying to reassert itself.

And the best charts in those groups are not merely holding up. They are pushing to new all-time highs heading into their next earnings reports.

That makes next week a very useful test.

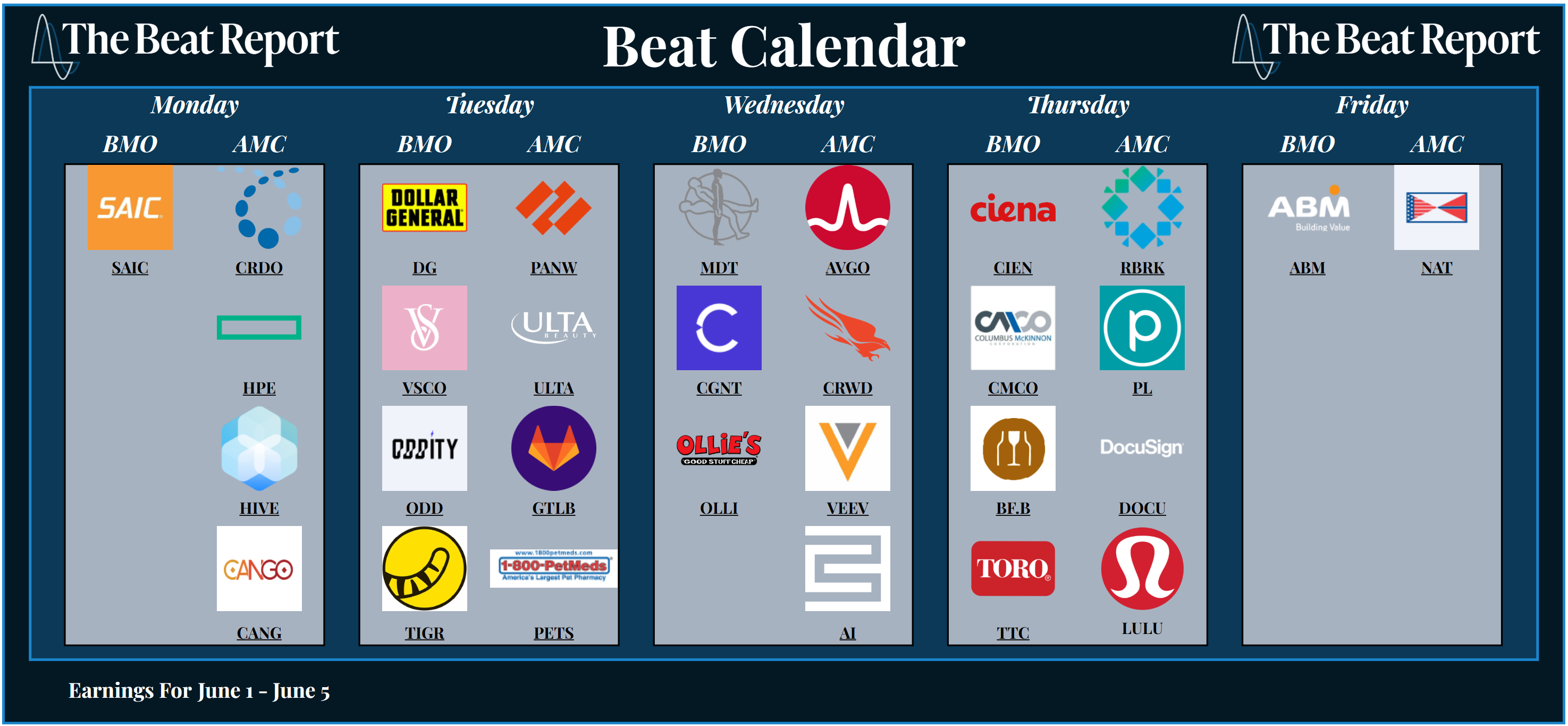

Here's a look at next week's Beat Calendar.

On Monday, we'll hear from Credo Technology $CRWD, and Hewlett Packard Enterprise $HPE.

Then on Tuesday, Dollar General $DG, Palo Alto Networks $PANW, Ulta Beauty $ULTA, GitLab $GTLB, and more will step into the earnings spotlight.

Wednesday brings some of the biggest reports of the week with Medtronic $MDT, Broadcom $AVGO, CrowdStrike $CRWD, and C3 AI $AI.

Thursday will also be action-packed with fresh reports from Ciena $CIEN, Rubrik $RBRK, Planet Labs $PL, DocuSign $DOCU, and Lululemon $LULU.

There will be plenty to monitor, but the three reports you must keep an eye on are AVGO, CRWD, and PANW.

Those are the names that should tell us whether this AI infrastructure and cybersecurity leadership can keep pressing higher, or whether expectations are beginning to get a little harder to satisfy.

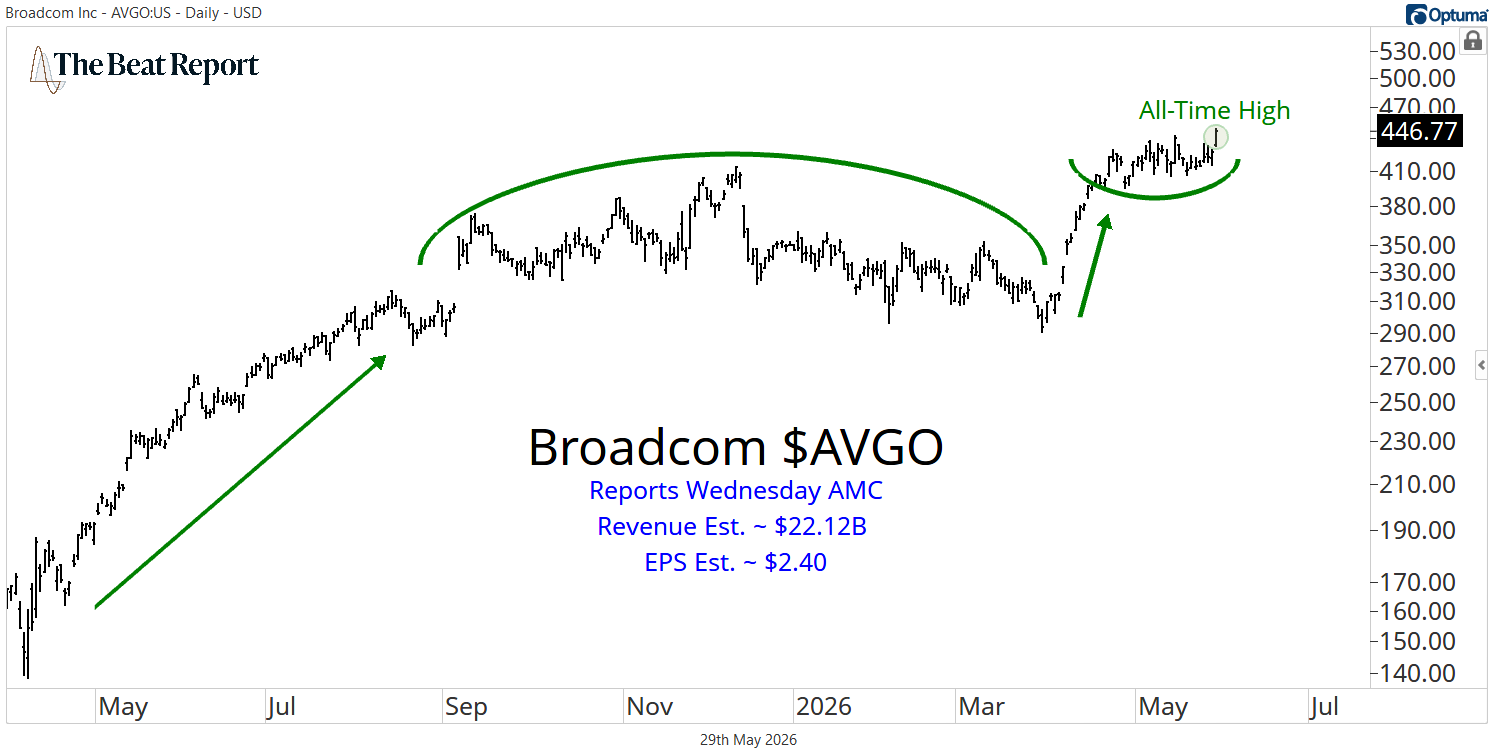

Broadcom reports Wednesday after the close, and the market is looking for $22.12 billion in revenue and $2.40 in earnings per share.

This is one of the best long-term compounders in the market, with a market capitalization of over $2 trillion.

And after exploding higher last year, Broadcom spent September through March churning sideways.

Then at the end of March something changed...

AVGO started ripping higher again and went on to print fresh all-time highs.

And now, after several weeks of churning sideways, AVGO is breaking out to new highs again ahead of Wednesday's report.

Turning to Broadcom's fundamentals, it's clear why the market treats this stock so well.

Last quarter, Broadcom reported record revenue of $19.26 billion, up 29% YoY.

AI semiconductor revenue was the real standout, growing 106% YoY to $8.4 billion, and management guided AI semiconductor revenue to exceed $ 10 billion.

Broadcom is one of the most important infrastructure companies in the AI buildout, with exposure to custom AI accelerators, AI networking, infrastructure software, and the rails that connect the modern data center.

Management said visibility into 2027 has improved dramatically, with a line of sight to more than $100 billion in AI chip revenue next year.

The only concern for us is earnings drift.

Last quarter, Broadcom saw negative pre- and post-earnings drift for the first time since June of 2024.

That does not make the chart bearish, and it certainly does not change the primary trend.

But it's something worth watching because the last time that happened, the next earnings reaction was one of the worst in years.

This week, we want to see buyers keep control.

If Broadcom gaps higher and holds new highs, the AI infrastructure trade is still alive and well. If it fails to rally on another strong report, that would be the first real sign that expectations are beginning to catch up with the fundamentals.

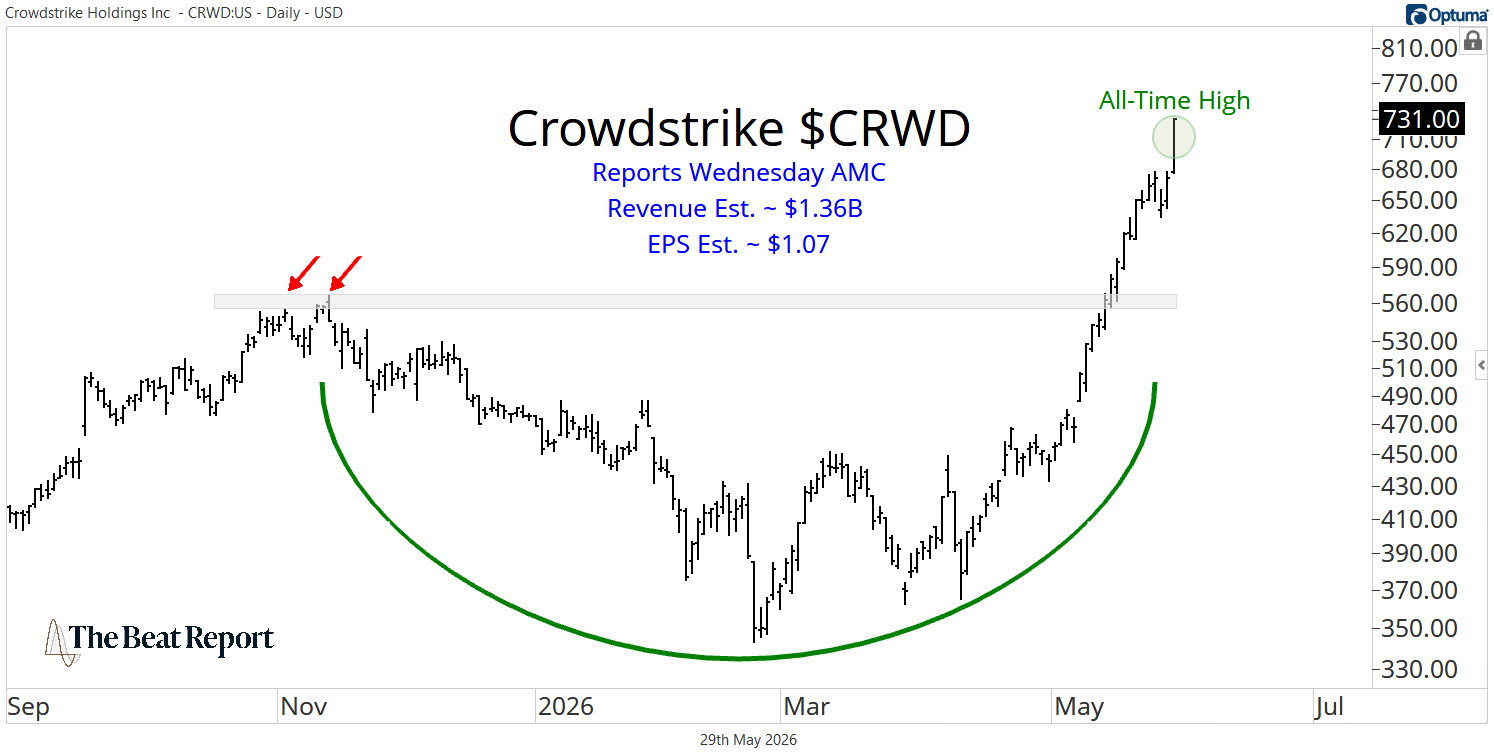

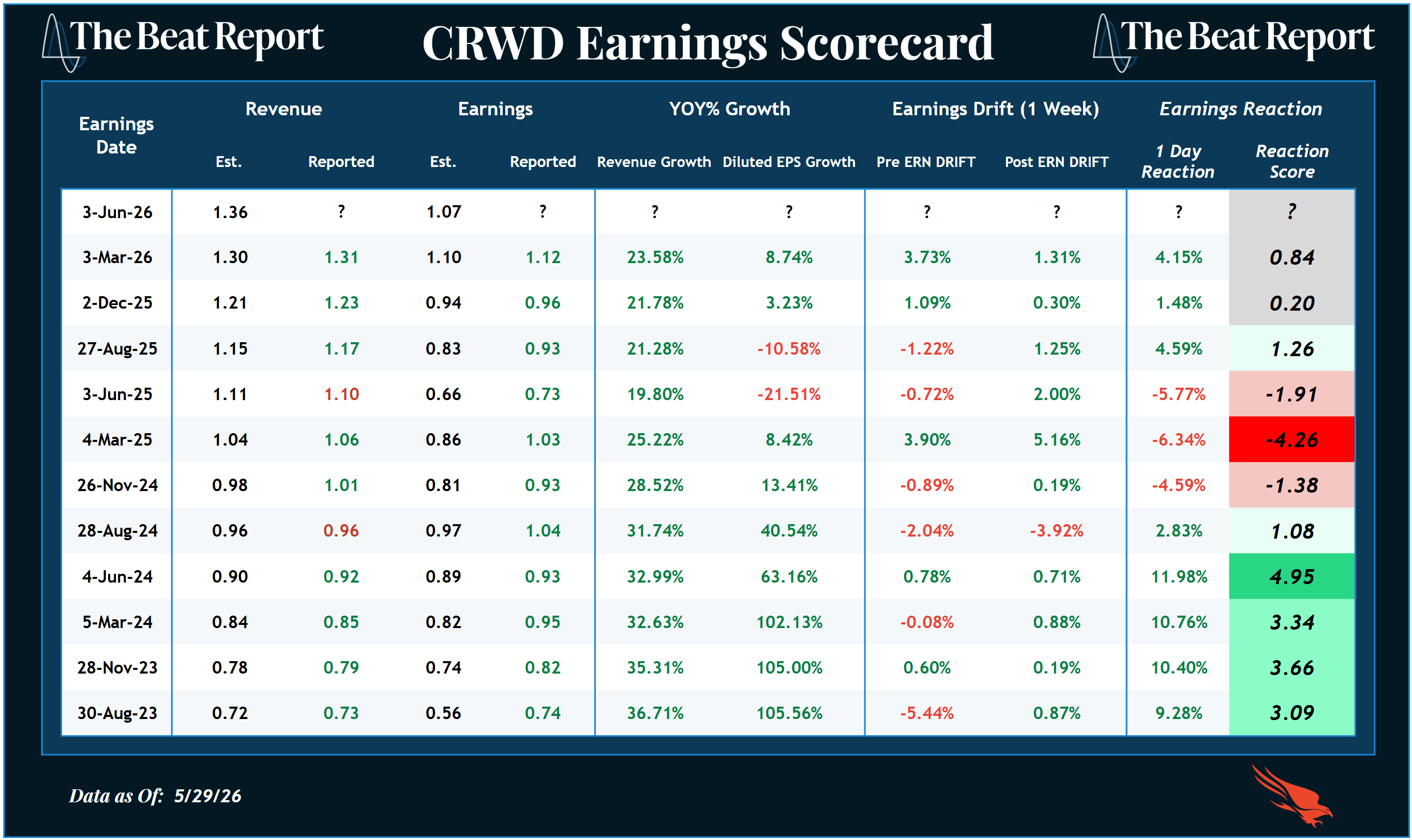

Next up is CrowdStrike, which also reports after Wednesday's closing bell.

The market is looking for $1.36 billion in revenue and $1.07 in earnings per share, and this chart is about as strong as it gets in software.

CrowdStrike bottomed near $350 earlier this year and has since doubled, reaching a new all-time high.

That is a massive move in a very short period of time, but the price action is not random.

The company is executing, the cybersecurity theme is red hot, and earnings sentiment has become a major tailwind.

The scorecard is among the best you'll find in the software industry.

CrowdStrike has been rewarded for three consecutive earnings reports, while also posting back-to-back quarters of positive pre- and post-earnings drift.

That tells us buyers are accumulating ahead of the event and continuing to support the stock afterward.

And the fundamentals explain why...

Last quarter, CrowdStrike surpassed $5 billion in ARR, with 24% YoY growth.

What's more, net new ARR grew 47% YoY to a record $331 million, and the company generated record free cash flow of $376 million in the quarter.

Falcon Flex also continues to scale, with ending ARR from Falcon Flex accounts up more than 120% year over year to $1.69 billion.

CrowdStrike has mission-critical infrastructure for the AI era, and the management is making that point clearly.

CrowdStrike is positioning Falcon as the security layer for AI across GPUs, hyperscalers, neoclouds, AI applications, agents, and the broader enterprise stack.

The real question is whether this report finally gives shareholders a reason to take profits.

Based on the chart, the earnings scorecard, and the fundamentals, CRWD remains one of the strongest software stocks in the market heading into next week.

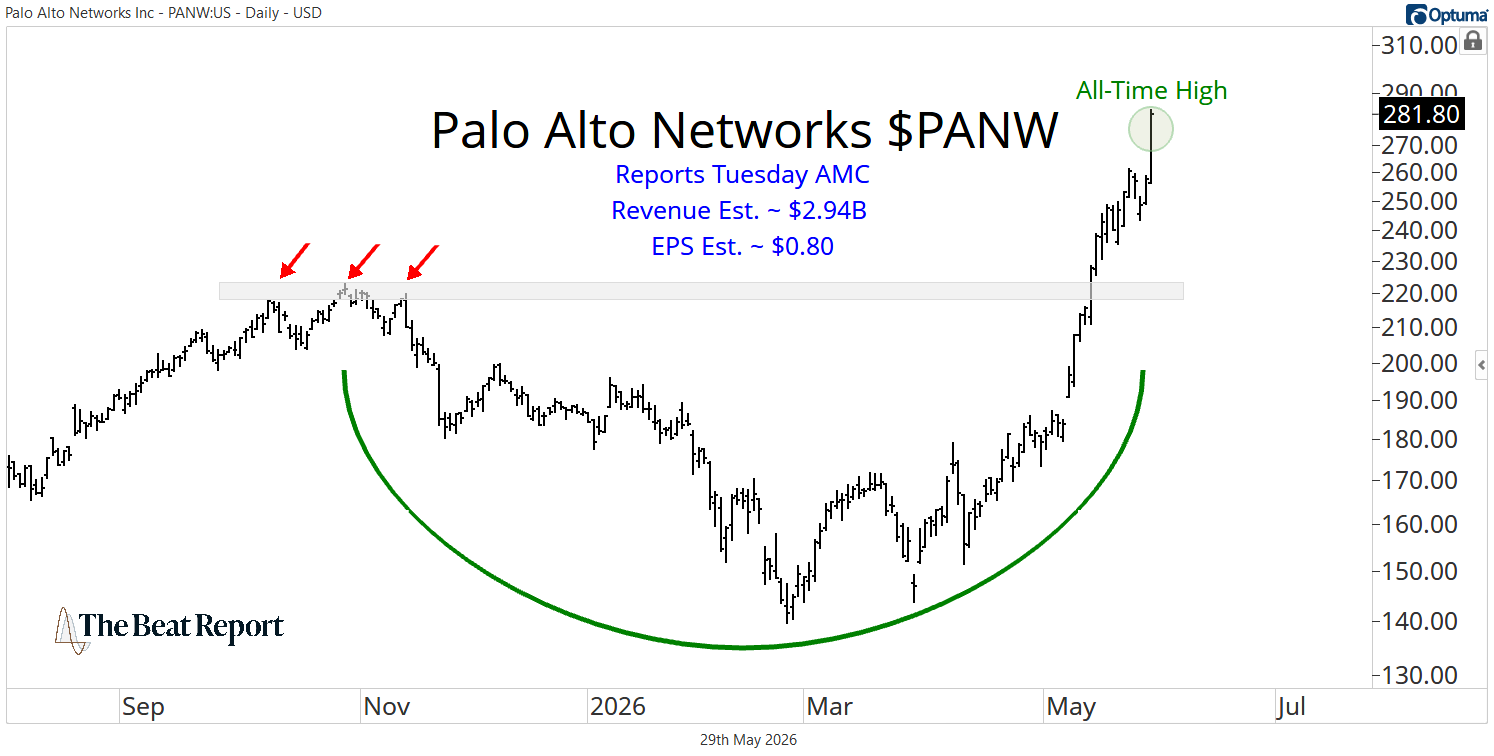

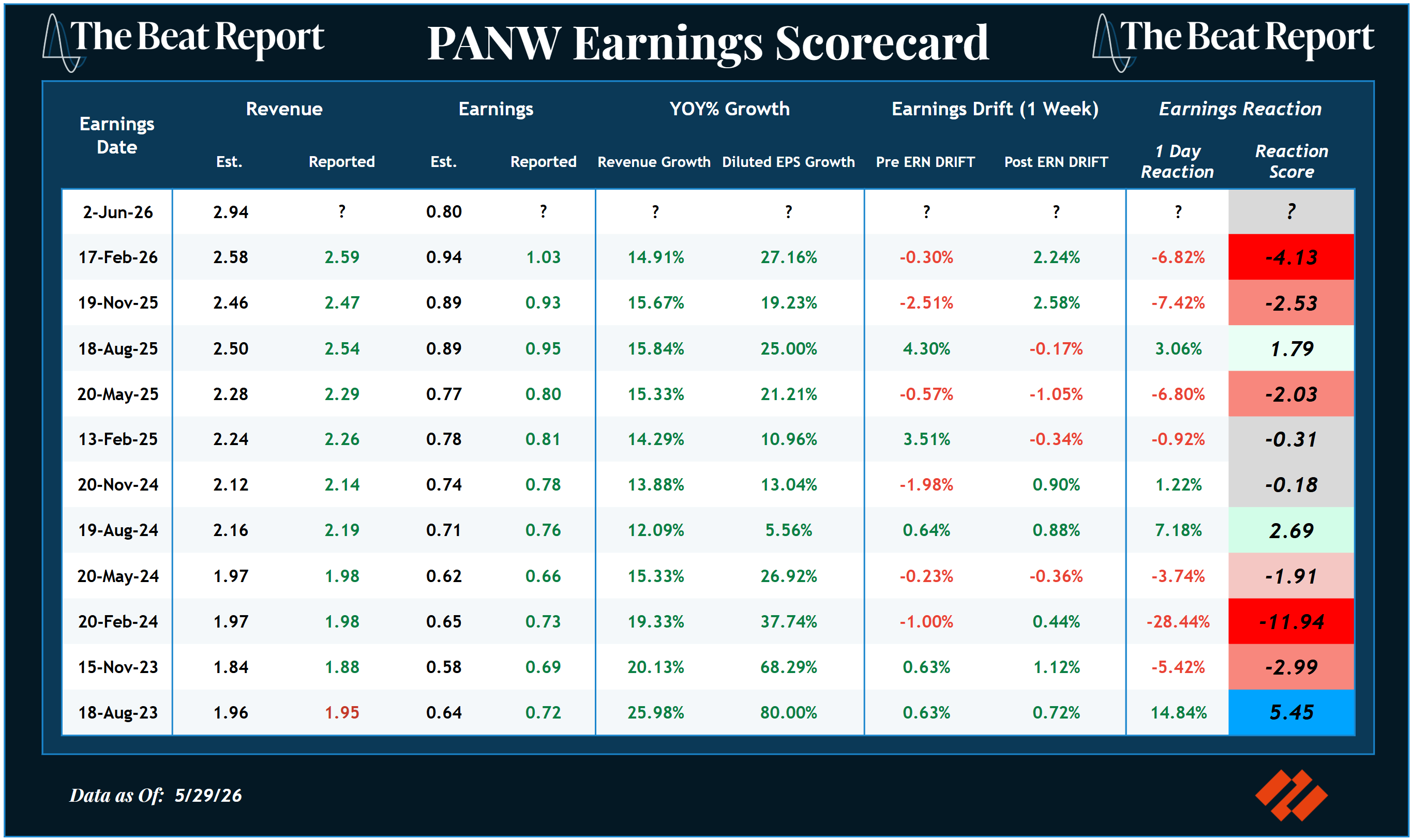

Finally, we have Palo Alto Networks, which reports after Tuesday's closing bell.

The market is looking for $2.94 billion in revenue and $0.80 in earnings per share.

Just like CrowdStrike, Palo Alto Networks is ripping to new all-time highs ahead of its report.

The stock has doubled from its early-year lows, climbing from roughly $140 to more than $280 in just a few months.

And the upside momentum is accelerating, with PANW rallying more than 9% on Friday, its best day since the April 2025 bottom.

The only problem?

Palo Alto Networks' earnings scorecard is nowhere near as good as CrowdStrike's.

Palo Alto Networks has been punished for back-to-back earnings reports, in stark contrast to CrowdStrike's streak of three consecutive positive reactions.

Revenue and earnings growth remain solid, but the market hasn't been willing to reward the company for its earnings events.

And that's what makes Tuesday’s report especially important.

Last quarter, Palo Alto grew revenue by 15% YoY to $2.6 billion, while Next-Generation Security ARR grew by 33% over the same period.

Management also highlighted continued momentum in its platformization strategy, with approximately 1,550 platformized customers, up 35% YoY, and a 119% net retention rate among those customers.

They also said large enterprises are moving beyond experimentation and beginning to integrate foundational models into real workflows, thereby expanding the attack surface and making security a critical control layer.

So the setup is simple...

The chart says buyers are in control, and the fundamentals are improving.

Now all we need to see is earnings sentiment flip from a headwind to a tailwind.

If Palo Alto Networks delivers a strong report and the stock rallies, that would mark a meaningful shift in earnings sentiment and confirm the new highs.

If it fails to rally again, we'll be more cautious with PANW, even if the long-term trend remains higher.

Recently, we've made a lot of portfolio moves at the Premium Beat Report as earnings season has provided us with a bunch of new signals.

If you want access to our next trade, join our growing community at the Premium Beat Report.

We hope you enjoyed this post,

-The Beat Team

Editor's Note: Most investors won't pay attention until this trend is obvious.