The Wall Street Journal Just Confirmed My Entire Thesis

The Wall Street Journal just published an exclusive that is the most important confirmation of my entire tokenization thesis.

I've been pounding the table that $100 trillion of assets are about to move onto this new tokenized technology, taking the financial system from the 1970s to the 2020s.

We've seen a lot of progress this year to bring securities like stocks and bonds onto this new technology. But in order for this $100 trillion trade to fully play out, we need both securities AND cash to live on the same rails. You can't settle a trade if only one side of the transaction is tokenized.

Today, the Wall Street Journal confirmed the other missing side, the cash leg, is coming and will be live next year.

There's a reason I've pivoted hard from crypto to tokenization over these last few months.

For years, we've heard all about how crypto was going to change the world. Most of it was bullshit. NFTs, DeFi, trustless and permissionless infrastructure. It was neat and novel, but it was never gonna fly with anyone bigger than the average retail pleb.

That's why when I first learned that financial institutions can convert securities and cash into tokens that live on this crypto technology, it all clicked for me.

They didn't need to build an alternative system. They could just take this new technology and use it to make the existing system operate more efficiently. Not replace the banks. Upgrade them.

But for this whole thing to work, financial institutions can't just tokenize securities like stocks and bonds. To reach its full potential, they need to tokenize the other side of these transactions: cash.

There were a few solutions proposed. A central bank digital currency was one idea. That got killed in the CLARITY Act because, for some reason, people didn't want the government tracking what everyone is spending their money on at all times.

Can't imagine why.

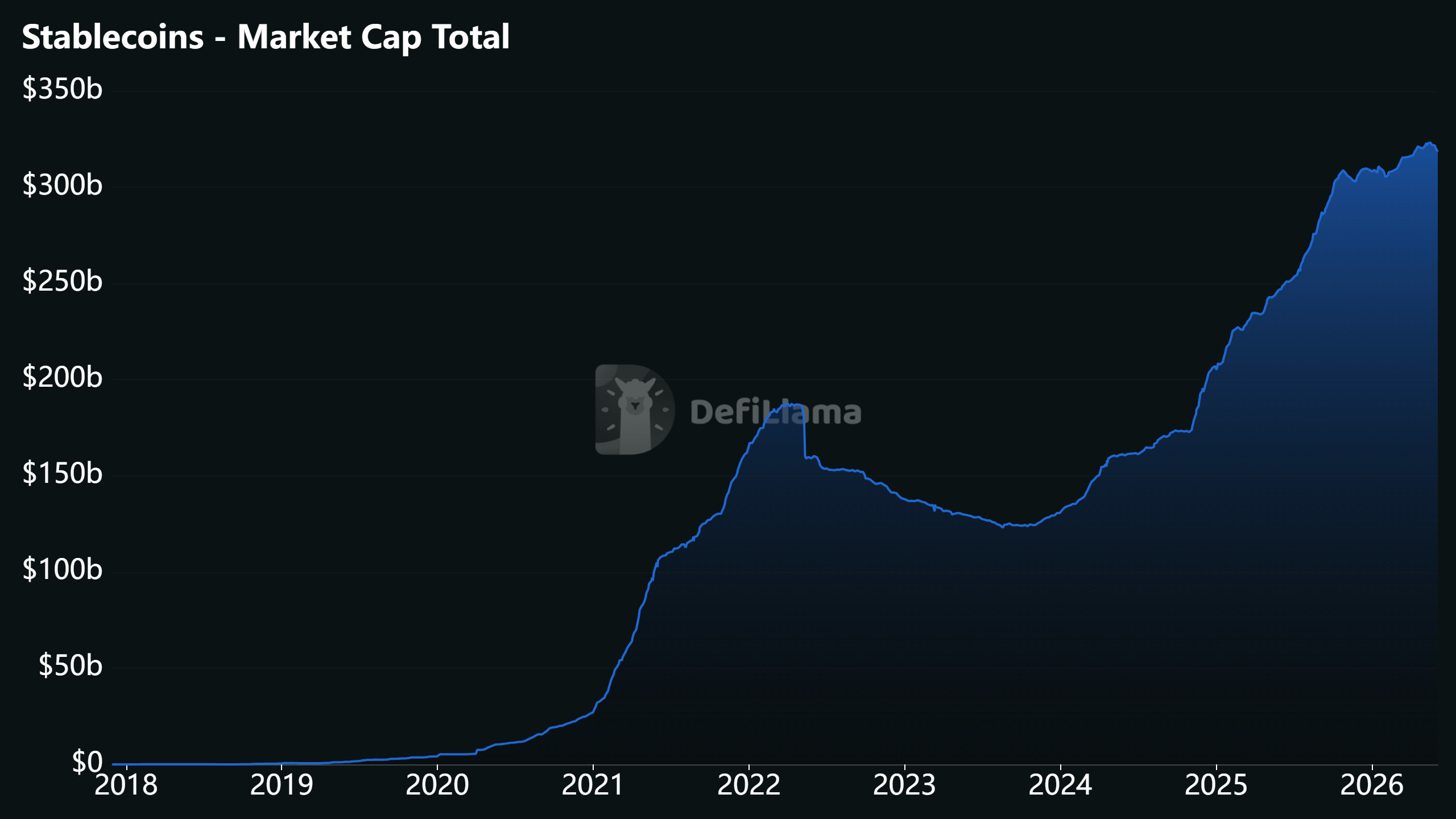

Stablecoins then came around, and they've grown into a $328 billion market.

But banks don't want their entire payment systems dependent on companies like Tether and Circle. If the cash leg of the entire financial system runs on USDC, that means Circle holds the deposits and earns the interest. The banks lose. That's not something JPMorgan and Bank of America are gonna sign up for.

So then tokenized deposits came around and this made the most sense. Banks could take the cash they already have sitting in their vaults and represent it using a token that lives on this new technology. Same deposits, with the same FDIC insurance. Just on new rails that settle instantly, 24/7, without waiting a full business day for ownership to actually transfer.

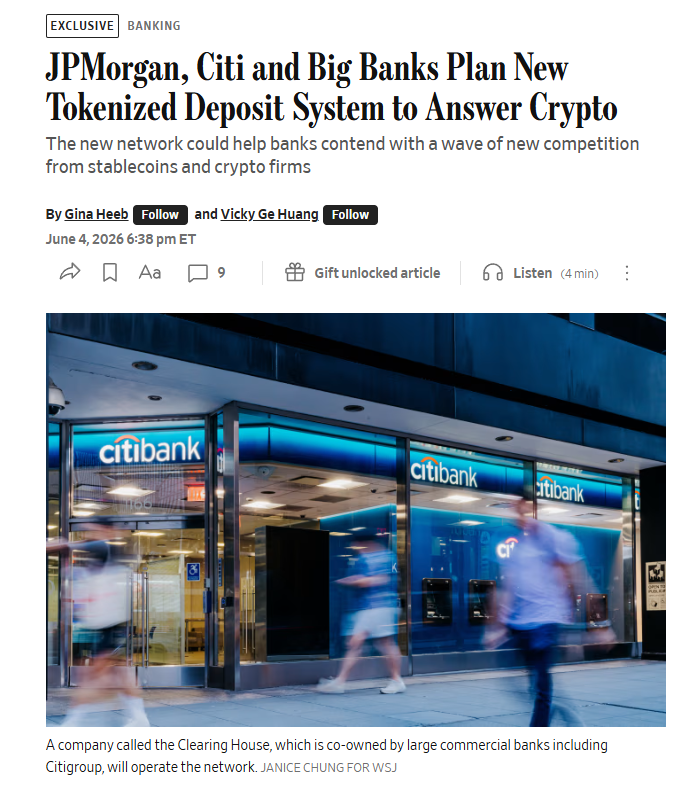

And that's precisely what the Wall Street Journal just reported on today. The largest banks in the United States are collaborating to develop their own tokenized deposit platform, which will be managed by a company they co-own called The Clearing House.

JPMorgan, Bank of America, Citi, Wells Fargo, all of them. Building this together. Target launch: first half of 2027.

But here's the part of the story that tells us where the real opportunity is going to be.

Yes, these banks are going to see efficiency gains and become more capital efficient from this transition. But the biggest investment returns won't come from owning the banks themselves. The biggest returns will come from the vendor providing the underlying blockchain technology that these banks are going to build on.

In the article, the Wall Street Journal said that the banks are not building their own network from scratch. The underlying blockchain will be an existing network provided through a vendor. That vendor hasn't been chosen yet.

But here's what I know about this decision.

First, it won't be Ethereum, Solana, or any other mainstream crypto blockchain.

I've written extensively about why these networks don't work for institutional finance. They have a fundamental privacy problem where every transaction is visible to the entire world. Goldman Sachs is not going to broadcast its deposit flows on a public ledger. That problem isn't getting fixed before these institutions need the technology ready.

Second, it likely won't be a private blockchain built and controlled by one of the banks, like JPMorgan's Kinexys chain.

In order for that to work, every other bank in America would need to plug into a blockchain managed by their largest competitor. That's how infrastructure rollouts have always worked in finance. No single company gets to own the underlying rails. The DTCC is industry-owned and independent for exactly this reason. On top of that, if the other banks refused to integrate with JPMorgan's systems, which they would because that's how banks think about competitive dynamics, it would create a fragmentation problem. Separate systems that can't talk to each other. Which is literally how we got into this situation in the first place.

Third, it will need to be a blockchain network that is neutral.

It has be independent, allows every bank to build their own system on their own terms with their own rules, and still lets all of them compose and settle with each other when they need to.

I think I know which network that is. It's the same one the DTCC chose for its tokenization service. The same one Goldman Sachs settles billions in repos on every day. The same one JPMorgan is deploying its deposit token on. The same one that Japan's clearing house chose for government bond collateral management. And it's the reason my entire account is concentrated the way it is right now.

Members of the Tokenization Report can read my full report on this network here:

Here's what I want you to take away from today.

For months I've been telling you that the $100 trillion trade requires two things to happen. Securities need to move onto this new technology. And cash needs to move onto this new technology. Both sides of every transaction need to live on the same layer for this to reach its full potential.

The securities side has been building all year. The DTCC launches its tokenization service in July. The NYSE is building a 24/7 tokenized stock trading platform. The SEC just released its innovation exemption. Broadridge is already processing $350 billion a day on this infrastructure. Paxos just became the first blockchain company to receive SEC approval as a clearing agency.

Today, the cash side just showed up.

The four largest banks in the United States confirmed they are building the other half of this equation together. And it launches next year.

Both sides are now coming together. Securities and cash. On the same technology. When you put both sides of a transaction on the same shared layer where they can interact directly, you eliminate the need for the dozens of intermediaries and separate databases that the current system requires to process a single trade. That's where the $100 billion a year in savings comes from.

That's my whole thesis.

When JPMorgan, Bank of America, Citi, and Wells Fargo move together on something like this, they're not experimenting. These banks have survived every financial crisis for over a century by being deliberate about infrastructure decisions. If they're building this together through an entity they've co-owned since 1853, they've already decided this is the future. They're not asking if tokenization works. They're asking who provides the technology.

And they're moving now because stablecoins are coming for their deposits. Stablecoin supply has grown from $236 billion to $328 billion in the ten months since the GENIUS Act was signed. That's a 39% increase. The Federal Reserve published research showing that banks with stablecoin exposure are already experiencing deposit pressure. The banks see the numbers. They know what happens if they don't respond. Tokenized deposits are the response.

The window to get positioned ahead of this trade is getting smaller every week. The securities side launches in weeks. The cash side launches next year. By the time this story hits the mainstream financial media in a way that regular investors actually understand what's happening, the early money will already be sitting in the names that matter.

That's why I built the Tokenization Report. To find the specific companies and tokens at the center of this infrastructure shift before the rest of the market catches on. Every pick in the report is tied to this thesis. And today's Wall Street Journal story is the strongest confirmation yet that the thesis is playing out exactly the way I said it would.

If you're not a member yet, now would be a good time to fix that.