What the SpaceX headlines aren't telling you

People buying the SpaceX IPO today deserve to lose their money.

Not because SpaceX is a bad company, it might be the most impressive company on Earth, but because of what this transaction actually is. The media is calling it the biggest IPO in history. They should be calling it the largest exit liquidity event in history.

And if you're a retail investor lining up for shares at $135, you need to understand the one role you've been cast in: the bag holder.

I'll show you exactly why in a minute, including the numbers on what happened to the last batch of "can't-miss" mega IPOs (spoiler: the median one was underwater a year later). But the SpaceX circus isn't even the real story today. There's a much bigger shift happening underneath this IPO, one that explains why deals like this may soon be relics and why the people who understand it will never need to fight for scraps at an IPO window again.

The largest exit liquidity event in history

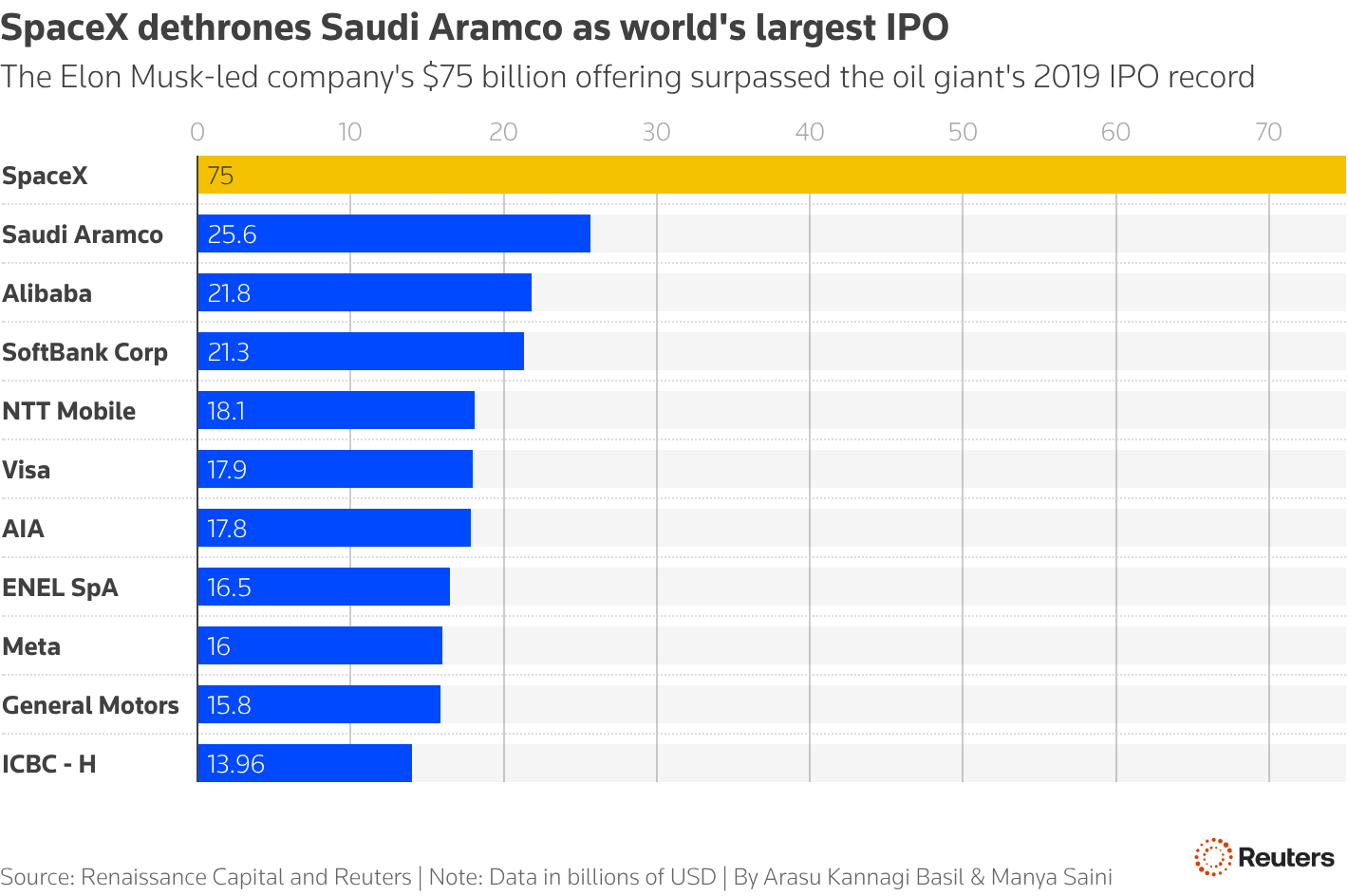

On Friday afternoon, SpaceX lists on the Nasdaq under the ticker SPCX at $135 a share with 555.6 million shares, a $75 billion raise, and a valuation of roughly $1.77 trillion. That makes it the largest IPO ever, dwarfing Saudi Aramco's $25.6 billion record.

Now ask yourself the only question that matters: who is selling, and who is buying?

The sellers are SpaceX itself and the private investors who got in years ago; funds that bought at a $400 billion valuation in mid-2025, at $800 billion in December, some at a tiny fraction of that a decade back. The buyers are... retail.

Ordinary investors serve exactly one purpose in this deal: to hold the bags so private money can take profits, and to hand SpaceX cash at the highest valuation the underwriters could possibly squeeze out of the market.

And about those underwriters, Goldman Sachs leading, with Morgan Stanley, Bank of America, Citigroup and JPMorgan behind them. Their incentives are in direct competition with yours. Their fees scale with the size of the raise. Their most important clients are the institutions getting allocations, not the retail trader buying the open. Every force in this deal pushed the price as high as it could go before the doors opened to you.

Here's the twist: I think it doubles first

The IPO is reportedly multiple times oversubscribed. Demand massively exceeds supply, the float is tiny relative to the company, and index funds will be forced buyers. That's a recipe for a violent squeeze higher. I wouldn't be surprised to see SpaceX double or more from $135 in the early going.

But that's the trap.

My call is that by this time next year, SpaceX will trade at a market cap below $500 billion. That's a decline of more than 70% from the IPO valuation, and something like 85% from whatever euphoric peak it hits first.

If you think that sounds extreme, it's not.

It's the pattern.

The graveyard of "biggest IPOs ever"

Look at the most hyped debuts of the last five years:

- Rivian, the biggest IPO of the decade, an $11.9 billion raise priced at $78 in late 2021, briefly worth more than GM and Ford combined. Today it trades around $15. Down roughly 80%.

- Coupang, the "Amazon of South Korea," a $4.6 billion raise priced at $35 in 2021. Today: around $16. Down more than half, five years on.

- Didi, a $4.4 billion mega-listing in 2021 that shed over $56 billion in value and delisted from the NYSE entirely within a year.

- Lineage, the biggest IPO of 2024, priced at $78. Today: around $38. Down roughly 50% in under two years.

- Venture Global, the biggest IPO of 2025, priced at $25. It now trades far below that, with Wall Street's average target sitting near $16.

- Airbnb and Snowflake, the decade's "winners." Both doubled from their IPO prices… which you were never allowed to buy. Retail bought the open: Airbnb opened day one at $146 and trades around $134 today. Snowflake closed day one above $250 and trades around $240 today. The day-one buyers of the two most successful mega-IPOs of the 2020s are flat to underwater more than five years later through one of the great bull markets in history.

These aren't all bad companies. They were good companies sold to the public at the worst possible price, at the moment of maximum hype.

That's why a few weeks ago, when I flagged Securitize as a company sitting at the dead center of the tokenization revolution, a potential major winner, I also told you I wasn't touching the stock at its debut. (It's going public via a Cantor Fitzgerald SPAC, listing on the NYSE as SECZ, with the shareholder vote set for June 29.) The best way to play almost any public debut is the same: let the day-one buyers absorb the losses, and swoop in months later at a far better price.

The real story: the IPO itself is becoming obsolete

Here's the part nobody will talk about today on CNBC.

By the time a company IPOs, the wealth has already been created. SpaceX went from a $27 million bet in 2002 to $1.77 trillion, a return of tens of thousands of times, entirely in private markets. The people who made life-changing money never bought a single share on an exchange. By the time you're allowed in, the company is mature, the risk is mostly wrung out, and the explosive returns belong to someone else.

For a century, that was just the rule: private markets were for institutions and the ultra-rich. Public markets were for everyone else. You got the leftovers.

Tokenization breaks that rule.

In plain English: tokenization lets financial institutions convert securities (public or private, equity or credit) into digital tokens that can be issued, traded, and settled on blockchain rails. It strips out major inefficiencies and costs that have kept trillions of dollars trapped. But the part that matters for you and your family is this: it cracks open the door to private markets, fractional ownership of the kinds of assets that used to demand seven-figure minimums and the right phone numbers.

Larry Fink, the CEO of BlackRock, has made this the centerpiece of his annual letters. In his words: "Every stock, every bond, every fund, every asset can be tokenized." He's argued that fractionalization increases access to previously out-of-reach assets like private equity and private real estate, and in this year's letter he framed tokenization as nothing less than an update to the plumbing of the entire financial system. BlackRock already runs the largest tokenized fund in the world.

The banks underwriting Friday's IPO are simultaneously building the rails designed to replace it.

That's the story.

The SpaceX IPO isn't the future of investing, it's the past, throwing itself one last, enormous trillion dollar party.

So no, I'm not buying SpaceX.

But I am going to be watching every tick of it, because a day like this moves the entire market. There's real money to be made around this event without being the bag holder at the center of it.

That's why we're going live TODAY at 2:00pm ET for a free live trading event.

SpaceX becomes a $1.75 trillion stock this afternoon, so don't trade it blind and don't watch the market event of the year through a headline feed. Sit in the room with six pros the moment SPCX opens. We'll react in real time, tell you exactly how we're playing it short term and long term, and hand you the sympathy stocks set to run alongside it.

The broadcast is free.

The private link is one email away.

Click here to claim Your Link to the Live Room.

A quick personal note.

Admittedly, I've been slightly removed from the noise this week. I've been under the weather and getting plenty of rest.

Here was me this morning getting my sunshine in while writing this, lol.

And you know what still managed to reach me holed up at the bottom of the world?

SpaceX.

My favorite contrarian indicators (my friends and family) have been texting me asking if they should buy the IPO.

When a deal generates that much FOMO that it finds you even when you're hiding from the market, that's usually the exact moment you should be most suspicious.

The loudest deals are rarely the best ones.