The Dumbest Selloff I've Seen All Year

The Wall Street Journal published a piece this weekend about how perpetual futures are "shaking up Wall Street." CME is suing the CFTC. Exchange stocks are getting hammered and Terry Duffy is on CNBC comparing perps to the 2007 housing crisis.

And I'm sitting here in New Zealand looking at this selloff thinking this might be the most mispriced reaction I've seen in a long time.

Let me back up.

I've been trading perpetual futures since 2020. I was 18 years old, interning at All Star Charts, and I opened my first perp position on FTX. Living in New Zealand, US markets open at 1:30am and close at 8am for me. I had two options: set an alarm for 1:30am and trade like a zombie, or don't trade US stocks. I chose the latter.

But perps never close. I could trade whenever I wanted regardless of what timezone I was in. Once you experience 24/7 markets, you never go back to business hours. The product is just better. There are no expiry dates to manage, no rolling contracts and paying fees every month, no gaps where the market moves against you while you sleep and you can't do a thing about it.

Now that product is landing in the United States and the reaction from the incumbents has been entertaining to watch.

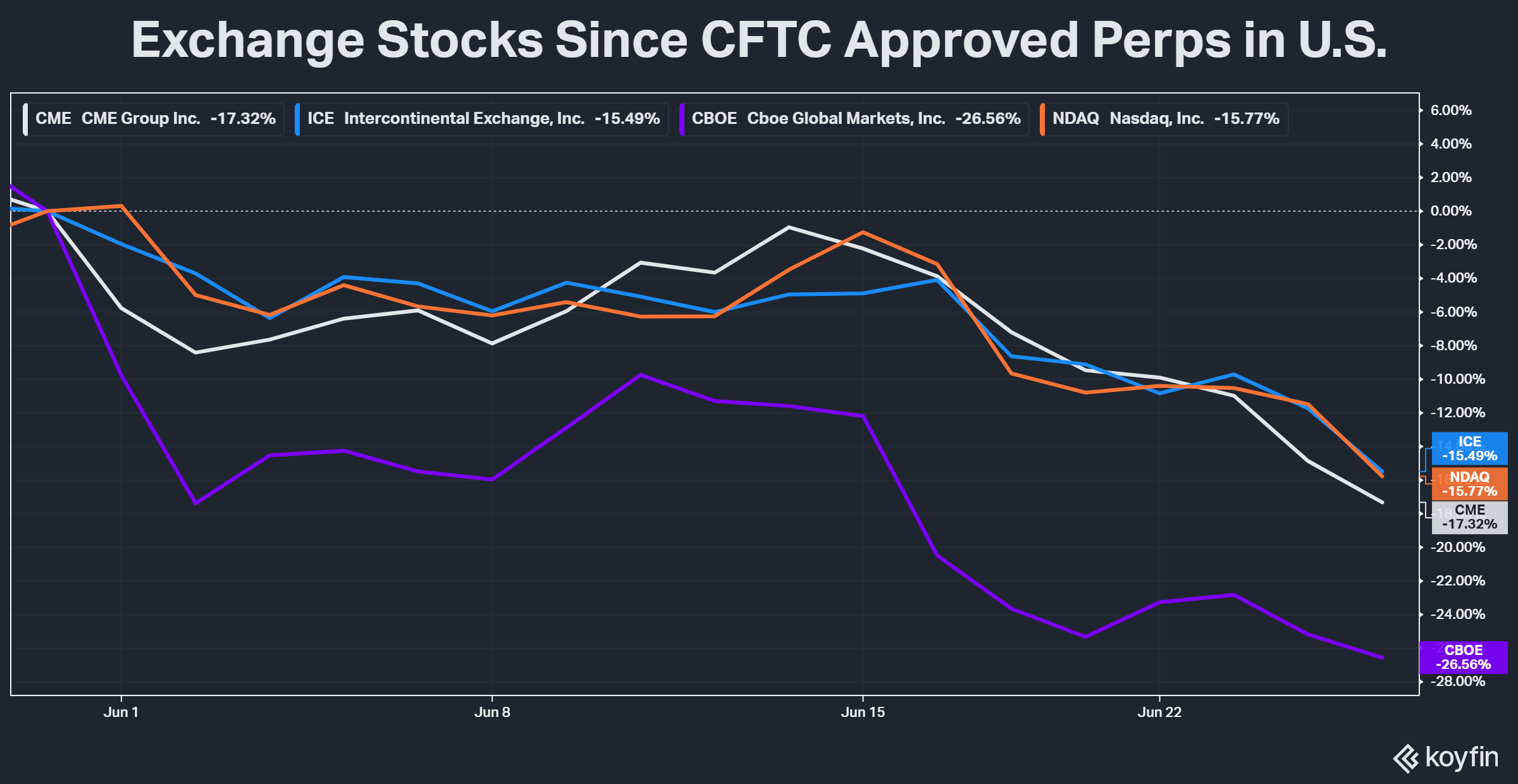

Since the CFTC approved perps on May 29:

- CME is down 17%

- Cboe is down 27%.

- ICE is down 15%.

- NDAQ is down 16%.

Billions of dollars in market cap wiped out because a prediction market called Kalshi did $8.5 billion in crypto perp volume and Coinbase opened up access to its global perpetuals for US customers.

Terry Duffy, the CEO of the CME, sued the CFTC. His own regulator. He went on CNBC and said "this is 2007 for retail" and that he doesn't want "casinos in exchanges."

And he's not entirely wrong. Mismanaged perpetual futures have been a disaster because of a mechanism called ADL (Auto De-Leveraging). In traditional exchanges, you receive a margin call and have time to add more capital to your account.

With perps, the exchange automatically liquidates your position instantly. Imagine if this is how traditional markets ran.

We could have multiple flash crashes every single year.

The core of Duffy's argument is that these perpetual futures are better classed as perpetual swaps. Which when BitMEX first introduced perps as a new way to trade markets, they actually introduced them as perpetual swaps NOT futures.

These things are extraordinary complex, and I don't see these exchanges being disrupted because Kalshi, a prediction market gambling website, is offering perpetual futures.

The CME generated $6.5 billion in revenue last year. Roughly $180 million of that, about 3%, came from crypto-related products. The other 97% comes from interest rate futures, equity index futures, energy, agriculture, and FX. These are massive institutional markets where banks hedge interest rate exposure, airlines hedge jet fuel, farmers hedge corn, and pension funds manage risk.

That business is not moving to Kalshi. It's not moving to Coinbase. It's not moving to Hyperliquid. Those platforms don't have the regulated clearing infrastructure, the margin frameworks, or the institutional counterparty protections that a pension fund requires to trade interest rate derivatives. The CME's core moat is institutional clearing, not retail crypto access. Perps threaten the retail edge of the business. The institutional core is completely untouched.

The market is pricing CME as if Kalshi doing $250 million a day in Bitcoin perps somehow threatens the $6.3 billion in revenue that comes from institutional derivatives. It doesn't.

And here's the part that actually made me laugh. The CME launched 24/7 crypto futures on the exact same day the CFTC approved perps for Kalshi and Coinbase. May 29. They did over 7,200 contracts the first weekend. They saw what Hyperliquid was doing with oil and the S&P 500 during the Iran conflict and they copied the market structure.

The CME isn't being disrupted by perps.

The CME is going to offer perps. They have to. The product is too popular to ignore. Cboe is already considering converting its continuous crypto futures into perpetual futures. ICE said they're "open to doing so if they see demand." Nasdaq is "watching the development." Every single incumbent is going to end up offering this product because the economics are too good to pass up.

When the CME eventually launches its own perps with their existing clearing infrastructure, their existing institutional relationships, and their existing regulatory standing, they're adding a new revenue stream on top of the $6.5 billion they already generate.

The Coinbase comparison is instructive. Coinbase has done $211 billion in notional perp volume since launching perpetual-style futures in July 2025. That's real revenue being generated from a product that didn't exist on their platform two years ago. When the CME launches the same product category with their brand and their institutional distribution, the revenue contribution will dwarf what Coinbase or Kalshi is doing.

Perps are no longer just a crypto product. Hyperliquid has oil trading on it. The S&P 500 is officially licensed for 24/7 perpetual trading on Hyperliquid. There are rumours the CME will extend 24/7 trading to gold and oil. FOMO, a retail trading platform which is introducing perps, just raised $75 million because the demand is that obvious.

If perps expand beyond crypto into commodities, equities, and FX as perpetual contracts, the total addressable market for the CME gets bigger, not smaller.

I think this selloff in the exchanges is so incredibly stupid, and there are some bargains to be had here.

The fact you're reading this far must mean I said something that intrigued you.

So if that's the case, I think there's something else worth your time. And that's Steve's recent investor briefing where he walked through his view that there's about to be a melt-up in the stock market and the time to get positioned is incredibly narrow.

I happen to agree with him, and that's why I'm personally allocating all my cash into buying stocks.

I come at markets from a different perspective to Steve, where I'm focused on the rollout of new technologies looking out multiple years. But Steve is all about capturing the highest possible returns in the shortest amount of time.

And if this melt-up in stocks is beginning, which I think it is, Steve will make a lot of money with his system.

He walked through exactly how he's planning to increase his account by more than 10x by the time Trump leaves office.

You can read all about by clicking here.

Cheers!