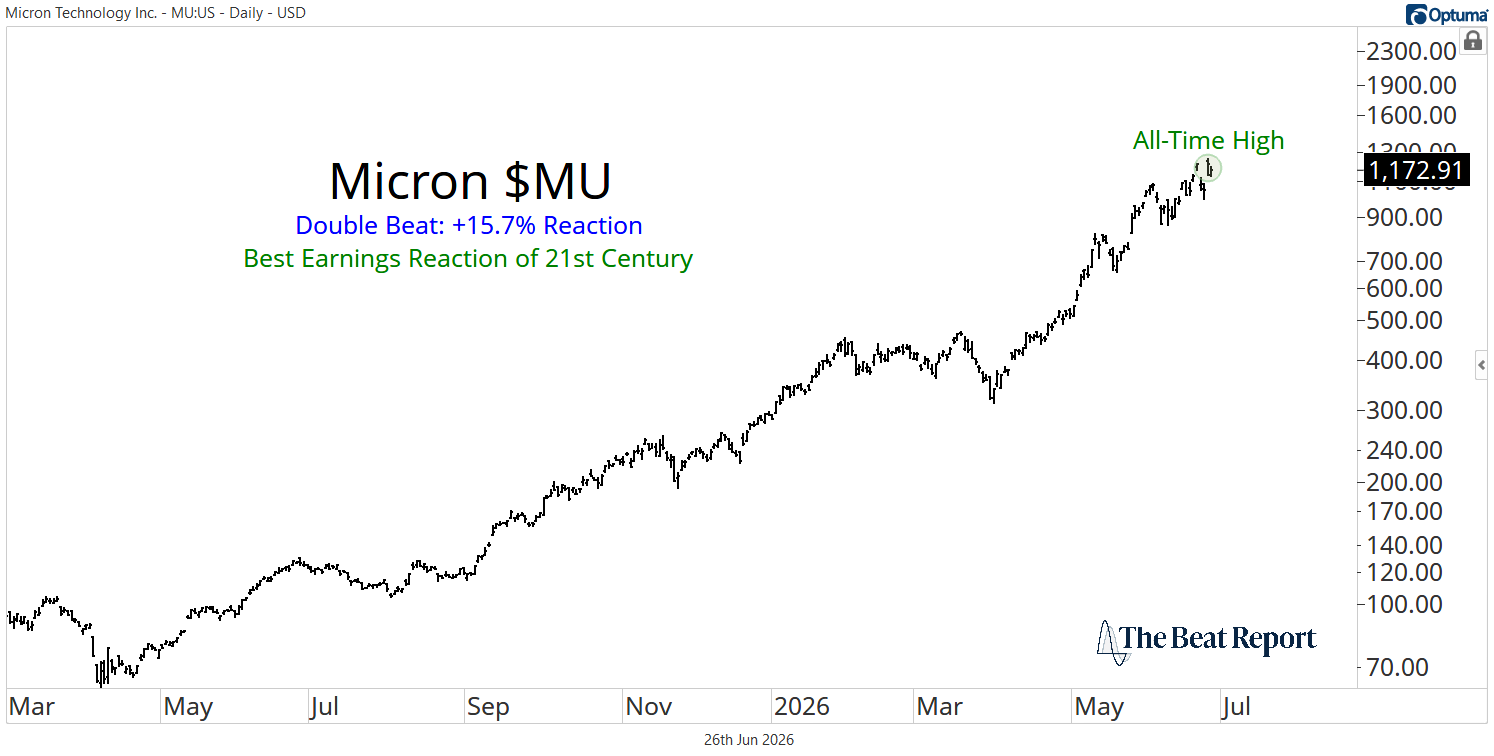

A historic reaction from MU gave semiconductors fresh life.

June 26, 2026

The semiconductor trade was starting to look tired after one of the strongest runs in market history.

Then Micron $MU walked in and kicked the door open.

On Thursday, Micron reported a monster double beat and rallied 15.7%, marking its best earnings reaction of the 21st century.

That is a big deal for any company, but it matters even more when the company is worth more than $1.3 trillion and sits right in the middle of the AI infrastructure buildout.

Micron is one of the most important AI hardware stories in the market, and the chart reflects it.

Since last April, MU has rallied from roughly $70 to more than $1,000 per share, putting it among the strongest primary uptrends in the market.

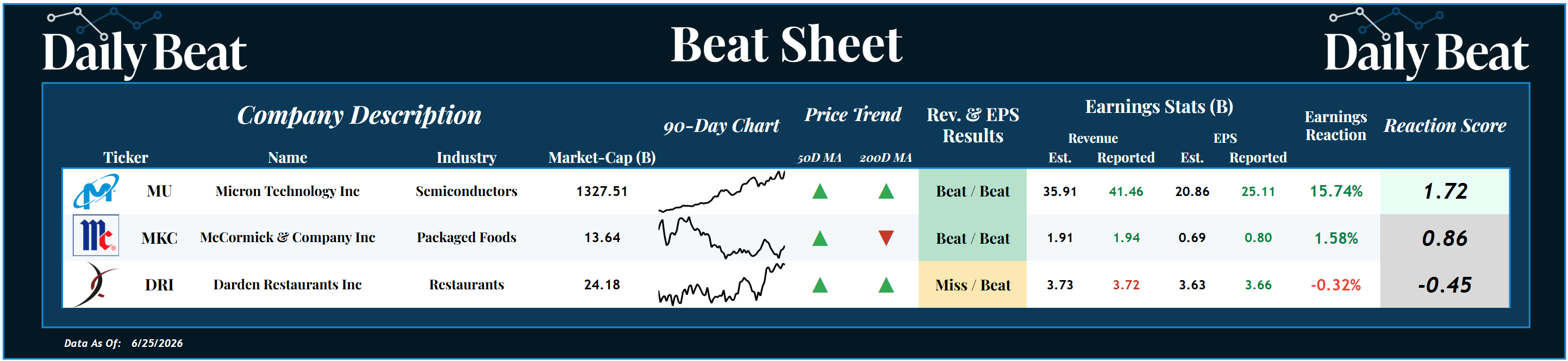

Turning to the Beat Sheet, Micron was the obvious story of the day.

*Click the image to enlarge it

The company reported $41.46 billion in revenue versus estimates of $35.91 billion, while earnings per share came in at $25.11 versus estimates of $20.86.

That's what it looks like for a company to knock the cover off the ball.

McCormick $MKC had a decent reaction, and Darden Restaurants $DRI was mostly quiet, but Thursday belonged to Micron.

When a trillion-dollar stock beats expectations by that much, gaps to new all-time highs, and posts its best earnings reaction in decades, we pay close attention.

The fundamental story is just as impressive as the chart.

In its latest report, Micron delivered record revenue, gross margin, and earnings per share.

Data center revenue exceeded $25 billion, which puts the business on an annualized run rate north of $100 billion, while data center SSD revenue more than doubled sequentially and exceeded $5 billion.

For years, investors treated memory like a commodity.

Demand would boom, supply would catch up, pricing would collapse, and everyone would wait for the next cycle.

And maybe that's the way it still is... But we don't seem to be at the end of the current cycle.

Management said DRAM and NAND demand continues to outstrip supply significantly, and tight conditions are expected to persist beyond calendar 2027 as AI demand collides with structural supply constraints.

In plain English, AI systems cannot work without more memory, faster memory, and higher-capacity storage.

GPUs and CPUs may get all the headlines, but memory is quickly becoming one of the most important bottlenecks in the entire AI buildout.

And that's why Micron matters.

Now, this doesn't mean MU has to go straight up every day from here.

The stock has already had a monster move, and some digestion would be perfectly normal.

But there is a big difference between a stock being extended and one in a primary downtrend.

Micron is extended because buyers cannot get enough of it, which is a high-class problem.

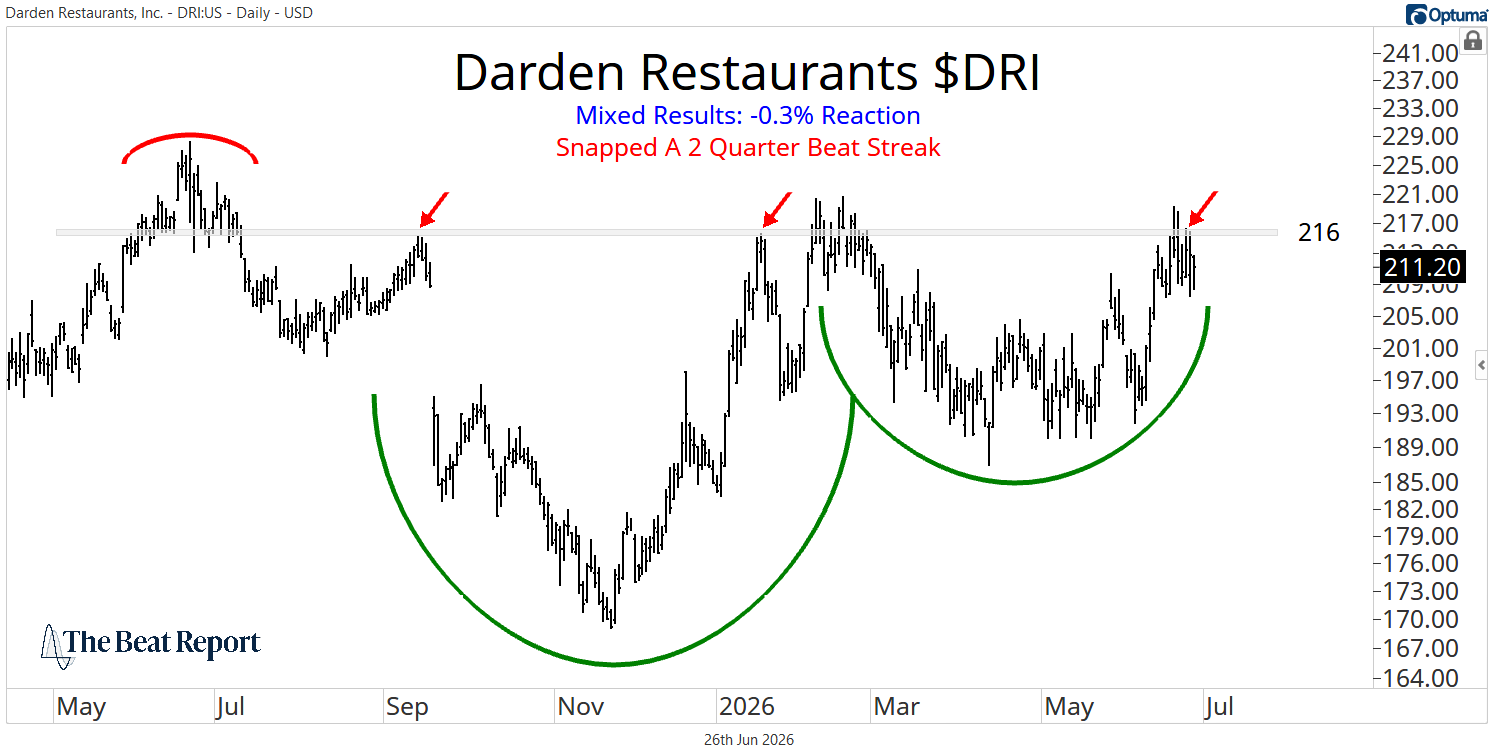

Turning to Darden Restaurants, the story is much quieter, but still worth watching.

Darden is the parent company behind Olive Garden, LongHorn Steakhouse, Yard House, Ruth’s Chris, The Capital Grille, Cheddar’s, Chuy’s, Seasons 52, and Eddie V’s.

And yesterday, the company reported mixed headline results, missing revenue estimates by a hair while beating earnings expectations.

As a result, the stock fell 0.3%, snapping a two-quarter beat streak.

Overall, it was pretty close to a nothingburger.

What really stands out to us is the textbook accumulation pattern price has carved out over the past year.

But for now, DRI remains stuck below overhead supply.

And until buyers can push the stock above $216 and hold it, this remains a range-bound setup.

The good news is that the fundamentals aren't broken.

Darden reported total YoY sales growth of 13.7% and adjusted EPS growth of 22.8%.

LongHorn Steakhouse remains the standout, with same-restaurant sales up 9.5% in the quarter, while every brand delivered positive same-restaurant sales.

Management also increased the dividend, authorized a new $1.5 billion buyback program, and guided for 75 to 80 new restaurant openings in fiscal 2027.

So this is a high-quality operator with strong brands, solid execution, and improving fundamentals.

The issue is the chart.

During our Portfolio Accelerator members' call yesterday, the team discussed how restaurants are quietly becoming one of the most compelling areas of the market, especially now that sentiment toward the group looks washed out.

Darden fits that theme.

But it still needs to break out.

If DRI holds up, drifts higher after earnings, and finally clears $216, we'd like it a helluva lot more as a long idea.

For nearly two and a half hours, the Beat Team pitched its highest-conviction trade ideas and debated them live with Steve Strazza in front of our members.