The Consumer Shows Up! WSM, ANF and Kohl's Report Cards

A quick breakdown of what you need to know about today's earnings

August 27, 2025

Kohl's, Williams-Sonoma beat! Abercrombie is a tale of two companies. Foot Locker is barely trying ahead of Dick's takeover.

Here's my instant-reaction to this morning's retail earnings.

Kohl's: Comps still negative, traffic up. Shares MURDERING shorts

Last night in a headfake $KSS shorts (of which there are many) will be complaining about for years, Kohl's traded 7% lower after-hours on rumors the company was delaying payments to vendors.

The topic is no where to be heard on this morning's conference call. Comps are still shrinking but Kohl's says traffic is up. Denim is strong in men's and women.

Bold Traders can try to ride this to $20 but I wouldn't chase it today.

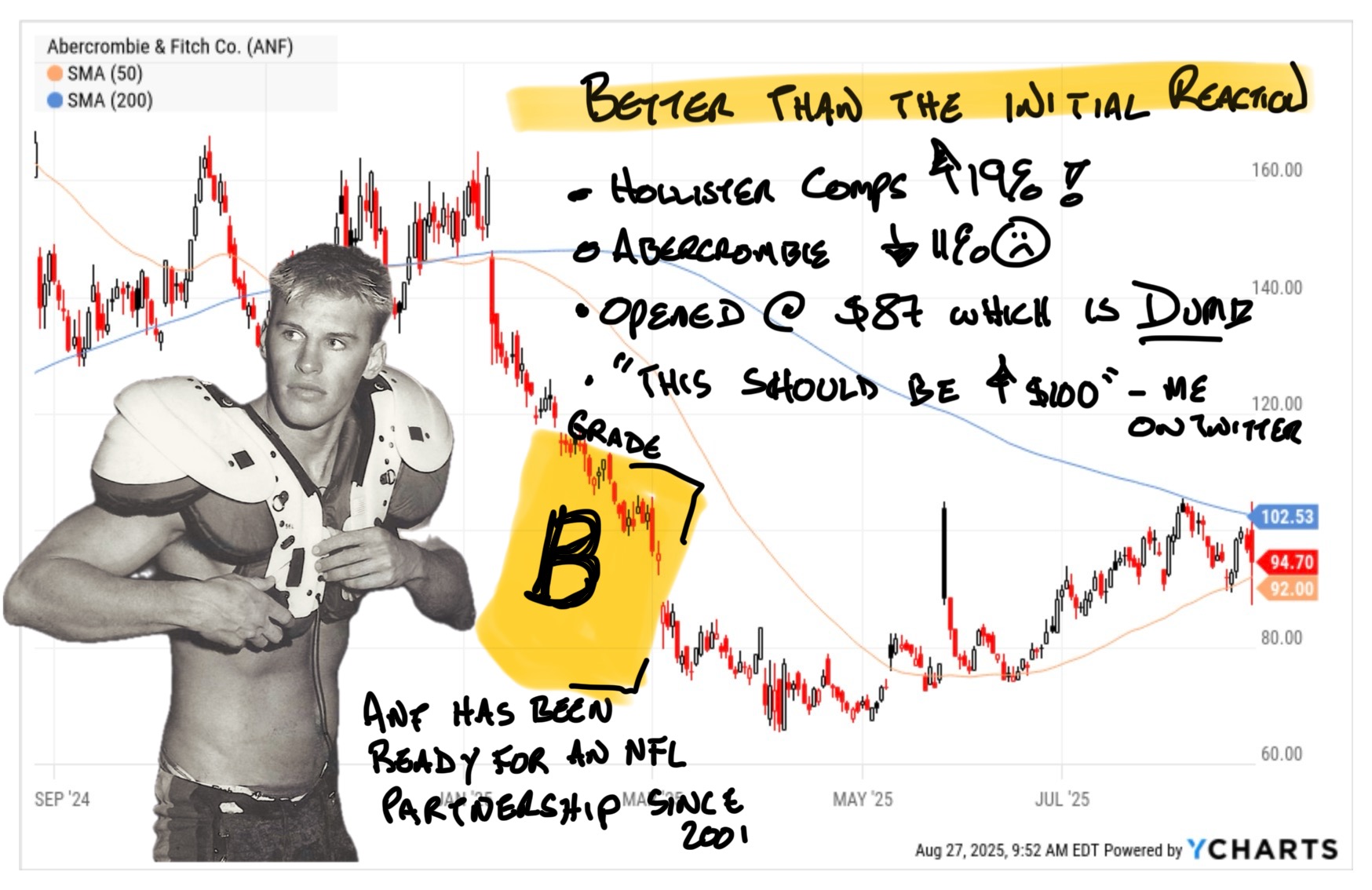

Abercrombie & Fitch: Hollister is on fire, Abercrombie still getting worse

The bears tried to whack ANF at the open and they had plenty of ammo. This is the 3rd Q in a row where Hollister crushed while Abercrombie tries to find its footing. The comp splits were +19% for Hollister (a record) and an 11% decline at Hollister's preppy brother.

The bear case is Hollister is about to run into tough comps and peak margins. The bull case is ANF just raised FY guidance to $10 - $10.50. 8.5x earnings is a reasonable price for a growing merchant because they shaved some pennies off Q3? C'mon.

Other news: ANF now has a non-specified deal with the NFL and Denim is rocking; leading to the FY revenue hike.

ANF now trading slightly higher at $98 (it bounced as I wrote). Below $100 is cheap.

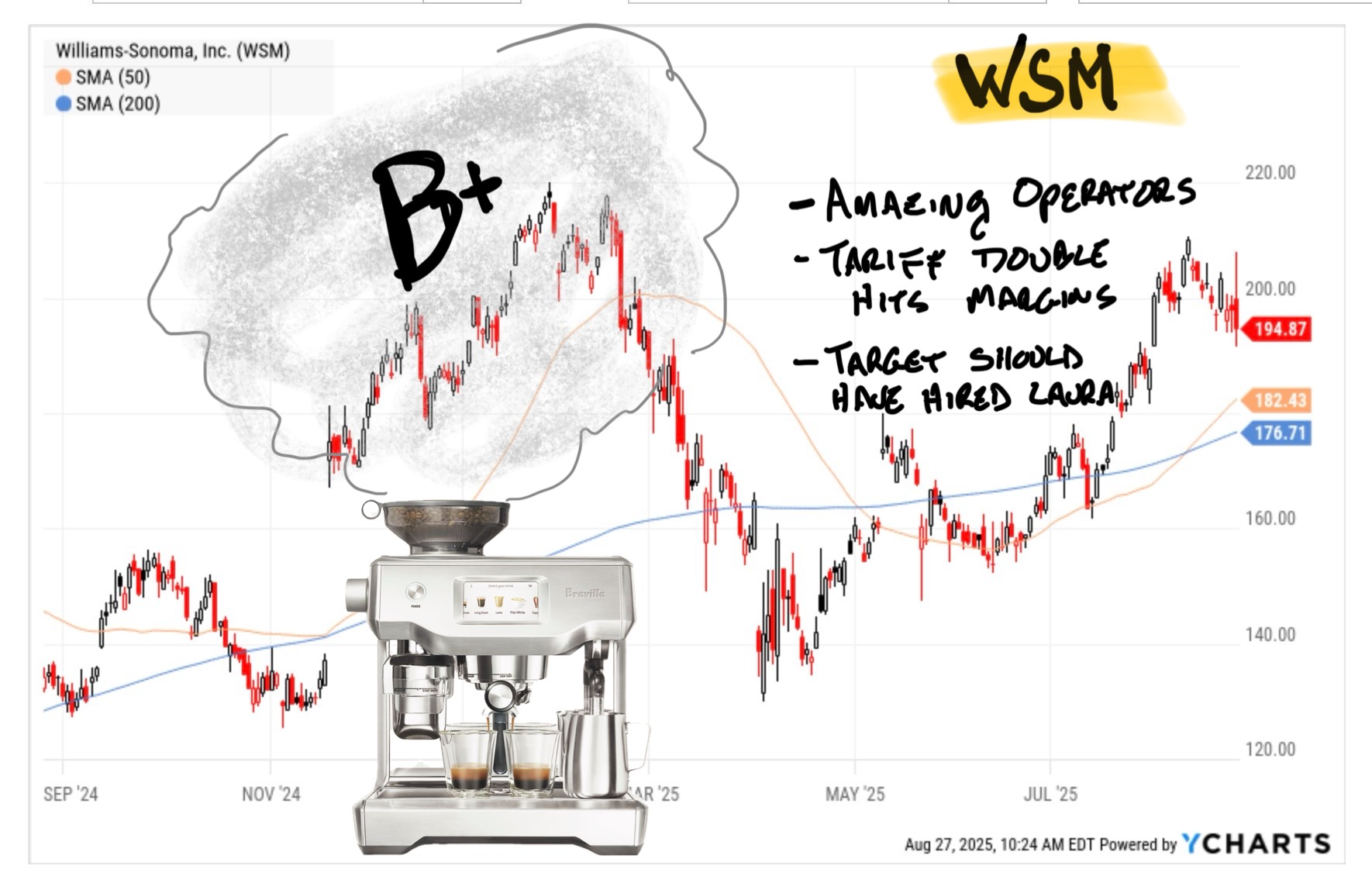

WSM: All comps positive for 2nd Q in a row. Tariff rate doubled over the Quarter. Crushes Estimates, guides

WSM would be trading about $220 right now if not for the Tariff Bomb dropped by the administration last Friday.

Positive comps in every division and HUGE EPS beat. CEO Laura Aber (I'm a huge fan) sounds "not happy" about the tariff hikes. Not the levels, not the randomness and especially not the insane levels of uncertainty.

On the call now, the co says it's being conservative on Q3 guide because (paraphrasing) "Who the hell knows what happens next to COGS? Honestly, the government could just steal 20% of the company without even asking. So leaving the EPS guide where it is gives us a little flexibility".

(The call operator went silent and Aber challenge the analysts to "unmute your lines and ask me something. Just go". She is the Jamie Dimon of specialty retail CEOs as far as I'm concerned.)