A number of people have reached out recently, asking in various ways if I have suggestions for riding out portfolio volatility.

I get it. When you're sitting on large gains or holding predominantly bullish positions, every market wiggle feels amplified. The stress is real.

Let's talk about hedging.

The only perfect hedge is cash. But of course, being in cash means missing opportunities, so that's not really viable if you're trying to actually make money in the markets.

Here's what most traders don't fully appreciate: if your options portfolio is mostly long premium and overweighted with bullish positions, you're exposed to more than just a market selloff. You're also exposed if we go sideways for any extended period. Time decay doesn't care about your thesis—it just grinds away at long premium whether the market drops or treads water.

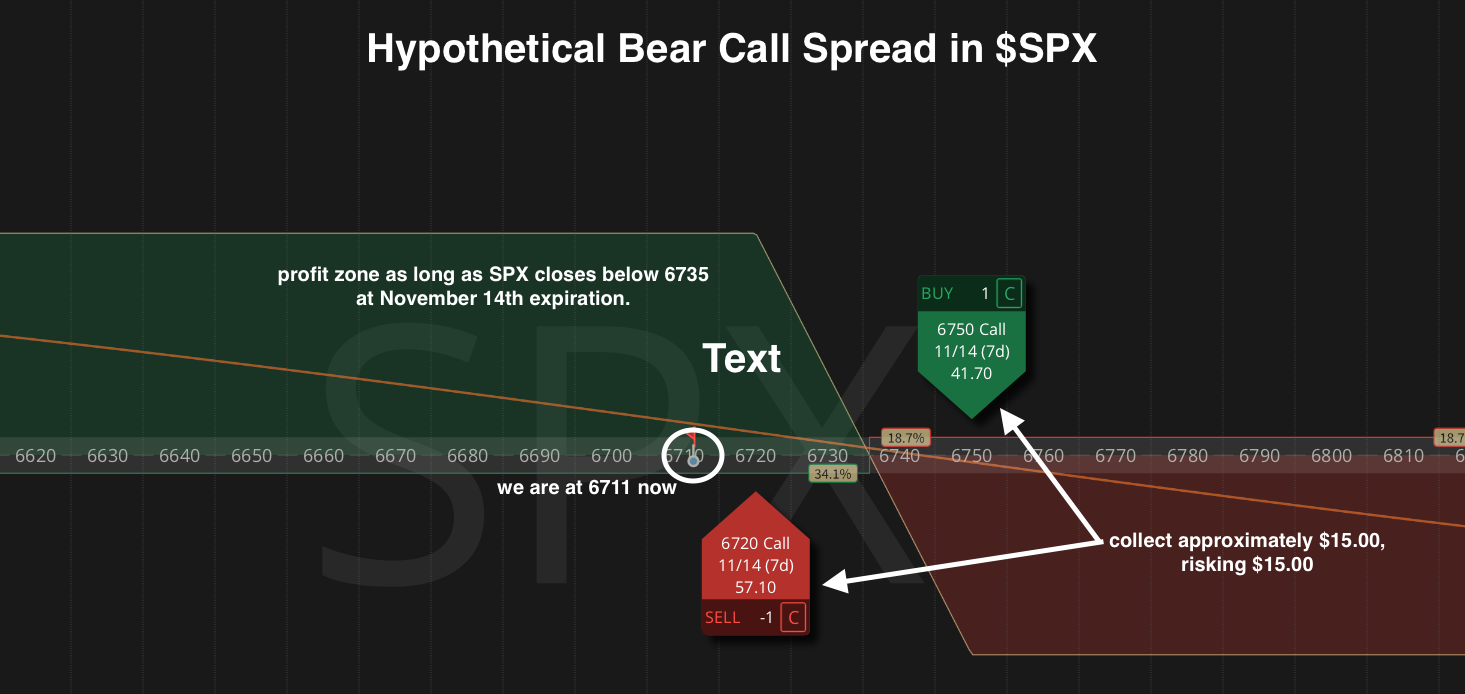

So if you don't necessarily want to exit your positions, consider selling call spreads in indexes like SPX.

A bearish call vertical spread—often called a "bear call spread"—profits in both down markets and sideways markets. It consists of a slightly out-of-the-money short call paired with a further out-of-the-money long call. These trades are put on for a net credit.

If both options expire worthless, you keep all the premium you collected at initiation. That can happen if the market falls or even if it just stays right where it is.

These trades lose if markets rise. But you'll probably be okay with that because your portfolio of long positions will likely make up the difference—and then some.

I invite you to experiment with short call vertical spreads in SPX. You could also use XSP. I prefer these instruments over SPY or QQQ because they're cash-settled with no early assignment risk. One less thing to worry about.

Play around with these. Start small. Experiment with different strike widths and expirations to see how the "hedge" feels for your specific portfolio.

But let's be clear: these aren't perfect hedges. In a sudden market collapse, the most we can earn is the premium we collected for these spreads. There's only so much protection on offer. But in your run-of-the-mill market drawdown or sideways chop? These are excellent vehicles that I find tremendous value in.

They won't save you from a 1987-style crash. But they'll cushion the blow during normal volatility and actually make you money when the market goes nowhere—which happens more often than people realize.

The psychological benefit is underrated too. Knowing you have some protection in place can help you hold your winners longer and make better decisions when volatility spikes. You're less likely to panic-sell at exactly the wrong time if you've already built in some downside cushion.

Start experimenting. Find what works for your portfolio size, risk tolerance, and sleep-at-night factor.

And if you're trying this approach, I'd love to hear how you're implementing it. What strikes are you using? What expirations? How much premium are you collecting relative to your portfolio size? Let me know—we're all learning together.

Sean McLaughlin | Chief Options Strategist, All Star Charts