The earnings spotlight is on the market's most explosive growth stories.

May 3, 2026

Editor's note: This week, the earnings spotlight is on the market's most explosive growth stories.

Many of these names have made huge moves over the past week and are trading at new highs.

Do you think the market has already priced in all the good news, or will these stocks find a way to surprise on the upside?

Write us at [email protected]. We value your input and may feature your responses in a future post.

This is the part of earnings season where things get fun.

We’ve already heard from a huge chunk of the S&P 500, and the market has given us plenty of information about what it wants to reward.

Semiconductors are still ripping.

AI infrastructure remains one of the strongest themes on the tape.

Mega-cap tech is splitting between clean execution stories and names where expectations are getting a little harder to satisfy.

And now, this week, we get another wave of reports that should tell us a lot about speculative growth, AI hardware, and the next phase of the infrastructure buildout.

But first, let's talk about what we learned last week.

Following a blockbuster report, Intel $INTC put the finishing touches on a .com bubble base by rallying 23.6%, marking its best earnings reaction of the 21st century. The company beat its revenue, margin, and EPS expectations, marking its 6th consecutive quarter of beating guidance, and management made it very clear that demand continues to outstrip supply across the business.

While INTC resolved a massive base, Charter Communications $CHTR broke down from a massive top on the heels of a mixed earnings report and its worst earnings reaction ever. Revenues are declining year-over-year, internet subscriber losses continue amid intensifying competition, and EBITDA is slipping as the business struggles to offset structural headwinds in video and broadband.

Despite reporting mixed headline results, Verizon $VZ rallied 1.5% for its 6th consecutive positive earnings reaction. Most notably, for the first time since 2013, the company posted positive first-quarter postpaid phone net adds.

In reaction to a double miss, Domino's Pizza $DPZ cratered 8.8% for its worst earnings reaction in 8 quarters. Same-store sales in the U.S. came in at just 0.9%, well below expectations. The management team blamed this on declining consumer sentiment, ongoing inflation, and increased competitive intensity in the pizza space, but the market wasn't willing to forgive them.

After crushing the market's headline expectations, Nucor $NUE rallied 4.7% to a new all-time high. The company is seeing record shipment volumes and a meaningful build in its backlog, with steel mill backlogs rising to 4.7 million tons, the highest level since 2021.

Following a big double beat, Corning $GLW tanked 8.9% for its worst earnings reaction since 2014. Heading into the report, the stock was attempting to breakout to new all-time highs. However, this breakout failed miserably, creating a textbook bull trap.

On the back of a historic earnings report, NXP Semiconductor $NXPI rallied 25.6% for its best earnings reaction ever. The company delivered 12% year-over-year revenue growth and showed broad-based strength across all of its end markets.

As a result of posting mixed headline results, GE Healthcare $GEHC cratered 13.2% for its 2nd-worst earnings reaction ever. The main issue with this company is profitability. Margins came under pressure due to rising input costs, including a roughly $100 million increase in memory chip pricing and another $100 million tied to oil and freight costs. This forced the management team to lower its full-year profit and free cash flow guidance.

In reaction to a much better-than-expected earnings report, Alphabet $GOOG rallied 10% for its best earnings reaction in 9 quarters. Until proven otherwise, this is the clear full-stack AI winner, and we expect it to be a market leader for the foreseeable future.

Despite reporting a double beat, Meta Platforms $META had a deeply negative earnings reaction. We believe this was largely due to the company's significant increase in CapEx forecast.

What's happening next week 👇

As you can see on this week's Beat Calendar, we're about to have another action-packed week of earnings.

Over the weekend, we heard from Berkshire Hathaway $BRK.A / $BRK.B, and we’ll get that reaction on Monday.

Then, after Monday’s closing bell, the spotlight shifts to Palantir $PLTR, Transocean $RIG, OnSemi $ON, and Duolingo $DUOL.

Tuesday brings Shopify $SHOP, PayPal $PYPL, Pfizer $PFE, Advanced Micro Devices $AMD, Super Micro Computer $SMCI, and MicroStrategy $MSTR.

Wednesday gives us Disney $DIS, Novo Nordisk $NVO, Uber $UBER, CVS $CVS, Arm Holdings $ARM, and AppLovin $APP.

Thursday is packed with Datadog $DDOG, McDonald’s $MCD, CoreWeave $CRWV, Iris Energy $IREN, Opendoor $OPEN, Coinbase $COIN, MercadoLibre $MELI, Rocket Lab $RKLB, Red Cat $RCAT, and several other high-beta names.

By Friday, the calendar cools off a bit, with TeraWulf $WULF standing out as one of the more important reports left on the board.

But for us, three charts matter most this week...

That is AMD, ARM, and PLTR.

These are some of the most important tell-tales for the AI trade, the semiconductor complex, and the high-growth software stocks that have been carrying so much speculative energy over the past year.

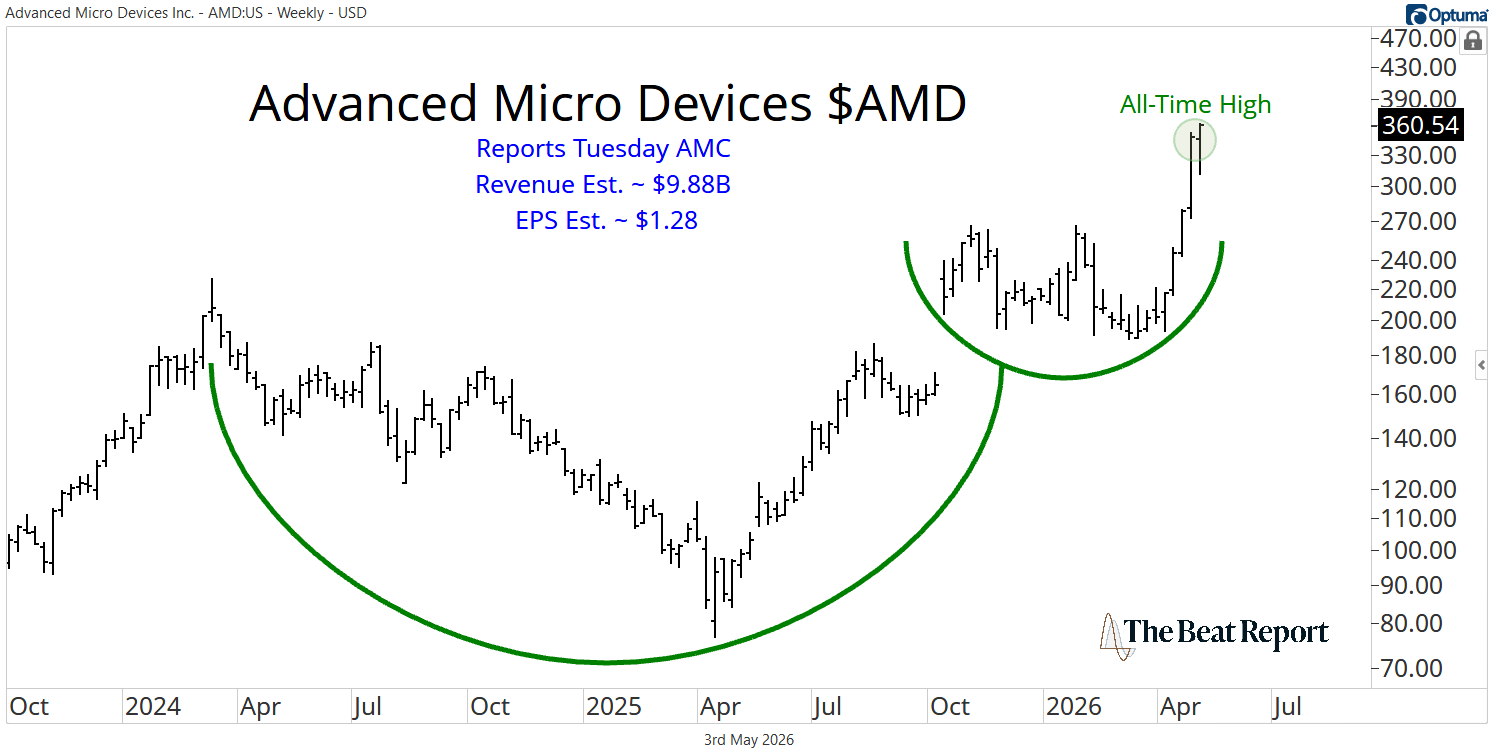

Let’s start with AMD.

The company reports Tuesday after the close, and the market is looking for roughly $9.88 billion in revenue and $1.28 in earnings per share.

Technically, Advanced Micro Devices could hardly look better heading into the event. The stock is resolving a massive base, trading at new all-time highs, and sitting on one of the strongest rallies in the market since last April's low.

After a nearly 400% move, this is one of the world's largest companies, with a market cap approaching $600 billion, and the market is clearly pricing it as a core winner of the AI infrastructure cycle.

And the fundamental story supports the move, at least on the surface.

AMD finished 2025 with record revenue, net income, and free cash flow, while fourth-quarter revenue grew 34% year over year to $10.3 billion.

Data center revenue rose 39% to a record $5.4 billion, driven by accelerating Instinct GPU deployments and server share gains.

That’s the good news...

The problem is that the stock has already priced in a lot of good news.

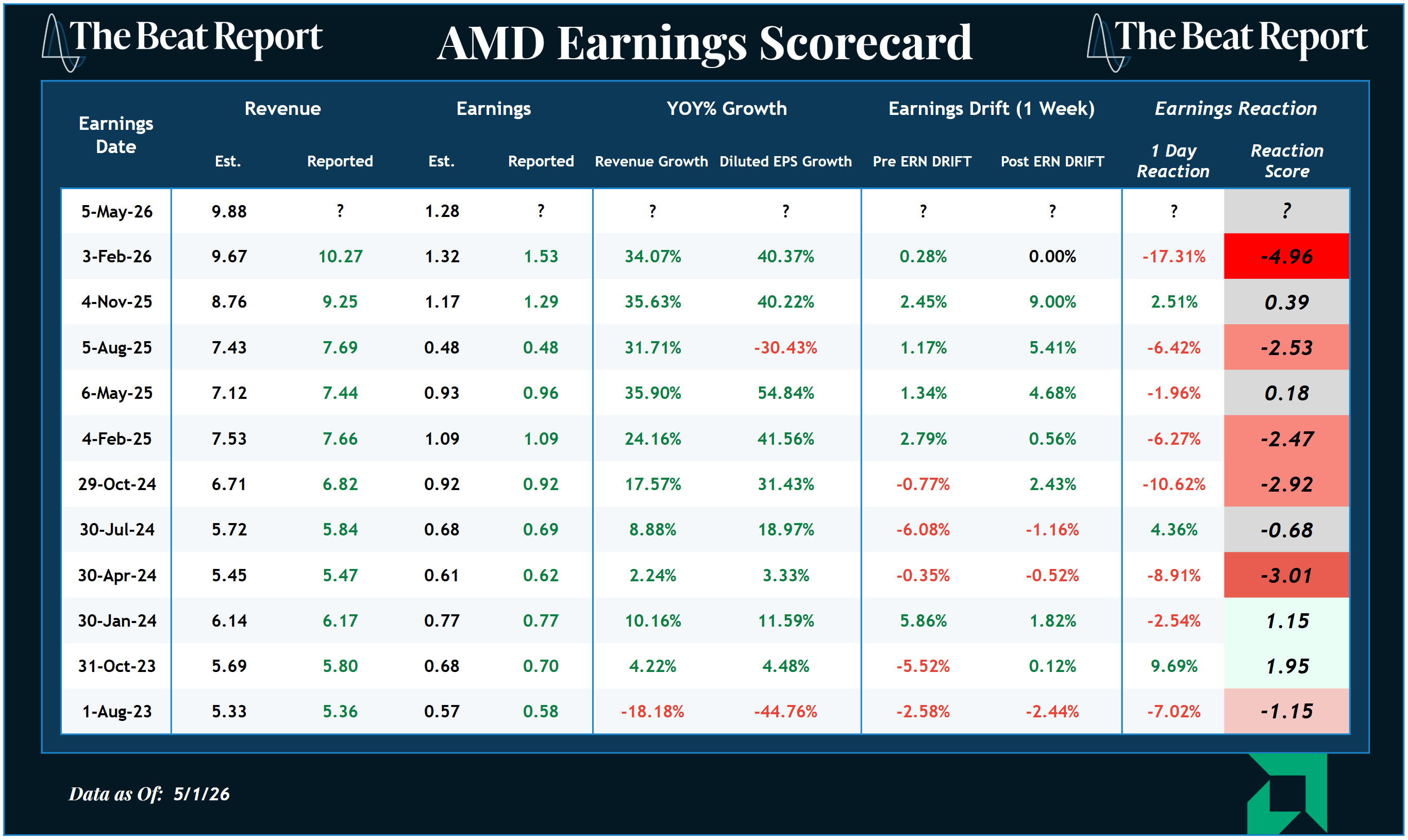

AMD’s earnings scorecard shows a stock that has been punished in 5 of the last 6 earnings reports, including a brutal 17.3% decline last quarter despite the company continuing to grow revenue by north of 30% and earnings by north of 40%.

That tells us expectations are extremely high, and even strong execution has not been enough to generate consistently positive reactions.

The market loves the long-term story, but it has been far less generous around the actual earnings events.

That is why we want to be careful with AMD this week.

The chart is outstanding, and the company is clearly benefiting from AI-driven demand. Still, when a stock has already rallied hundreds of percent and earnings sentiment remains a headwind, the bar is high enough that even a good report can trigger selling.

If AMD gaps higher and holds, that would be a huge confirmation for the entire AI hardware trade.

But if it beats and then sells off again, that would be another reminder that the market has already pulled much of future growth into the present.

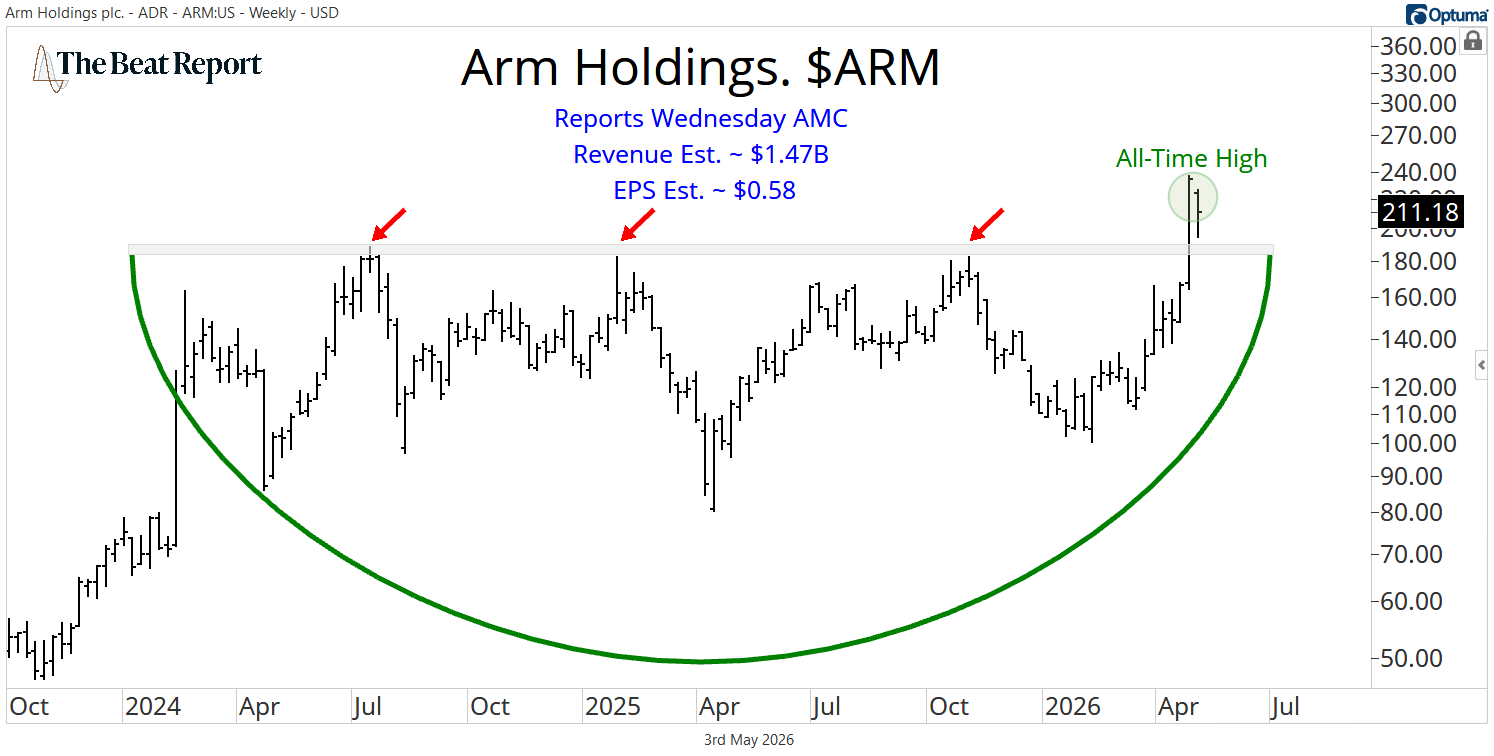

Arm reports Wednesday after the close, and this is probably the cleanest technical setup of the three.

The company reports after Wednesday's closing bell, and the market is looking for roughly $1.47 billion in revenue and $0.58 in EPS.

Heading into the report, Arm is breaking out to new all-time highs and looks poised to continue climbing higher.

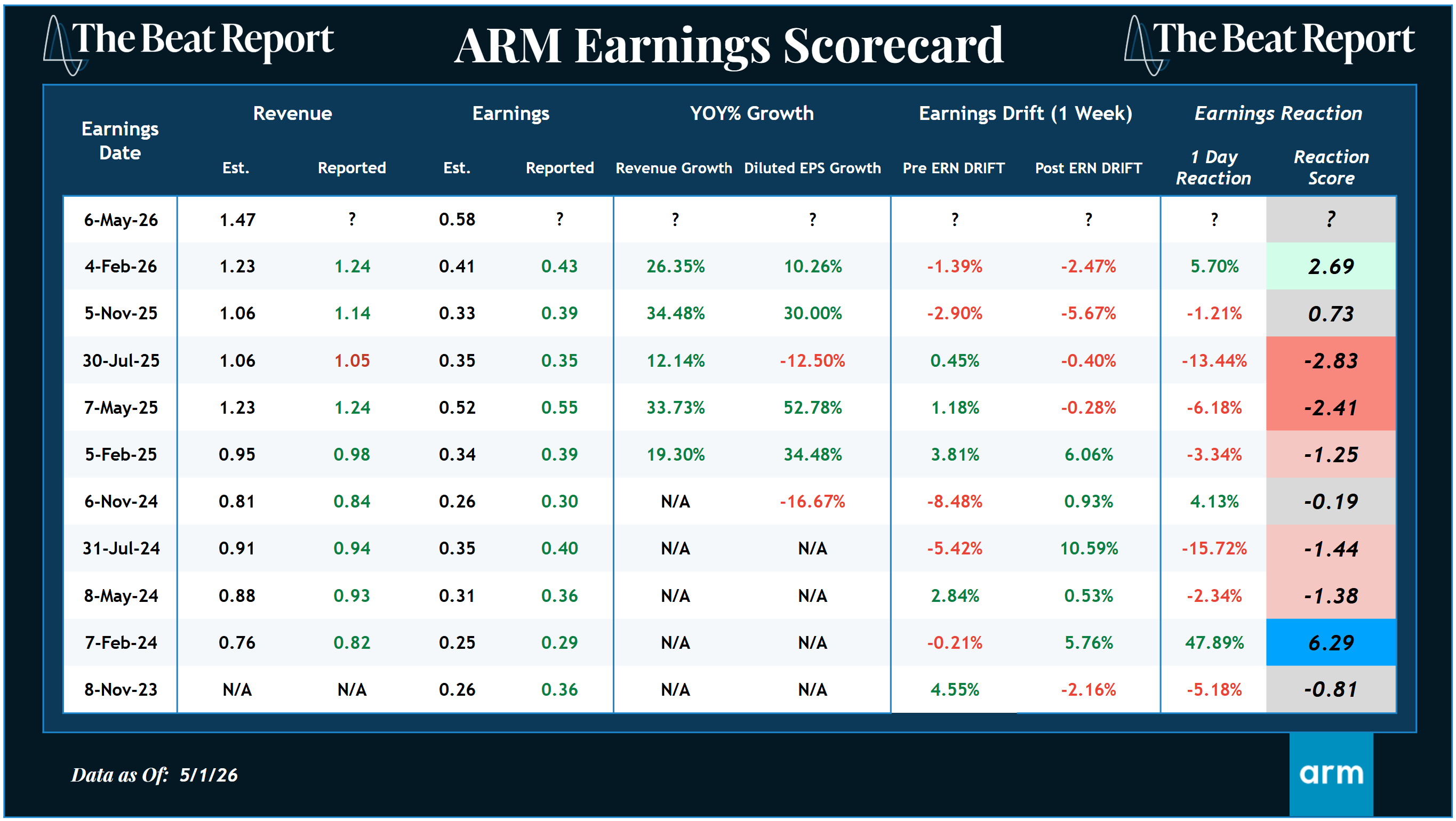

And unlike AMD, earnings sentiment has recently started to improve.

Heading into the last quarter, Arm had been punished for 4 consecutive earnings reports. Then it snapped that streak with a 5.7% positive reaction, and now the stock is pushing into blue-sky territory.

That is a major shift...

When negative earnings sentiment flips positive right as price breaks out to new highs, we pay close attention because we consistently see this precede the best primary uptrends.

Now, let's talk about Arm's fundamentals.

Last quarter, Arm delivered 26% year-over-year growth, marking its 4th consecutive billion-dollar quarter.

And the royalty revenue growth is off the charts... Last quarter, data center royalty revenue more than doubled year-over-year.

But the bigger story is where Arm sits in the AI stack...

There’s been a lot of talk about GPUs, and rightfully so, but agentic AI is also changing the CPU story in a big way.

Arm is arguing that as inference becomes more agent-based, workloads become persistent, always-on, and power-constrained. That makes CPU orchestration and power efficiency orders of magnitude more important.

What's more, Arm Neoverse CPUs have surpassed one billion deployed cores, and Arm’s share among top hyperscalers is expected to reach nearly 50%.

In other words, Arm is becoming a data center, edge AI, physical AI, and cloud AI story all at once.

The company has organized itself around those three AI domains, and compute subsystems are increasing the value Arm captures per chip as more customers choose to license deeper layers of the stack.

So when you pair that fundamental story with a breakout to new all-time highs and a recent flip in earnings sentiment, it is hard not to be constructive.

We're expecting the market to reward ARM with a big positive reaction and new all-time highs this week.

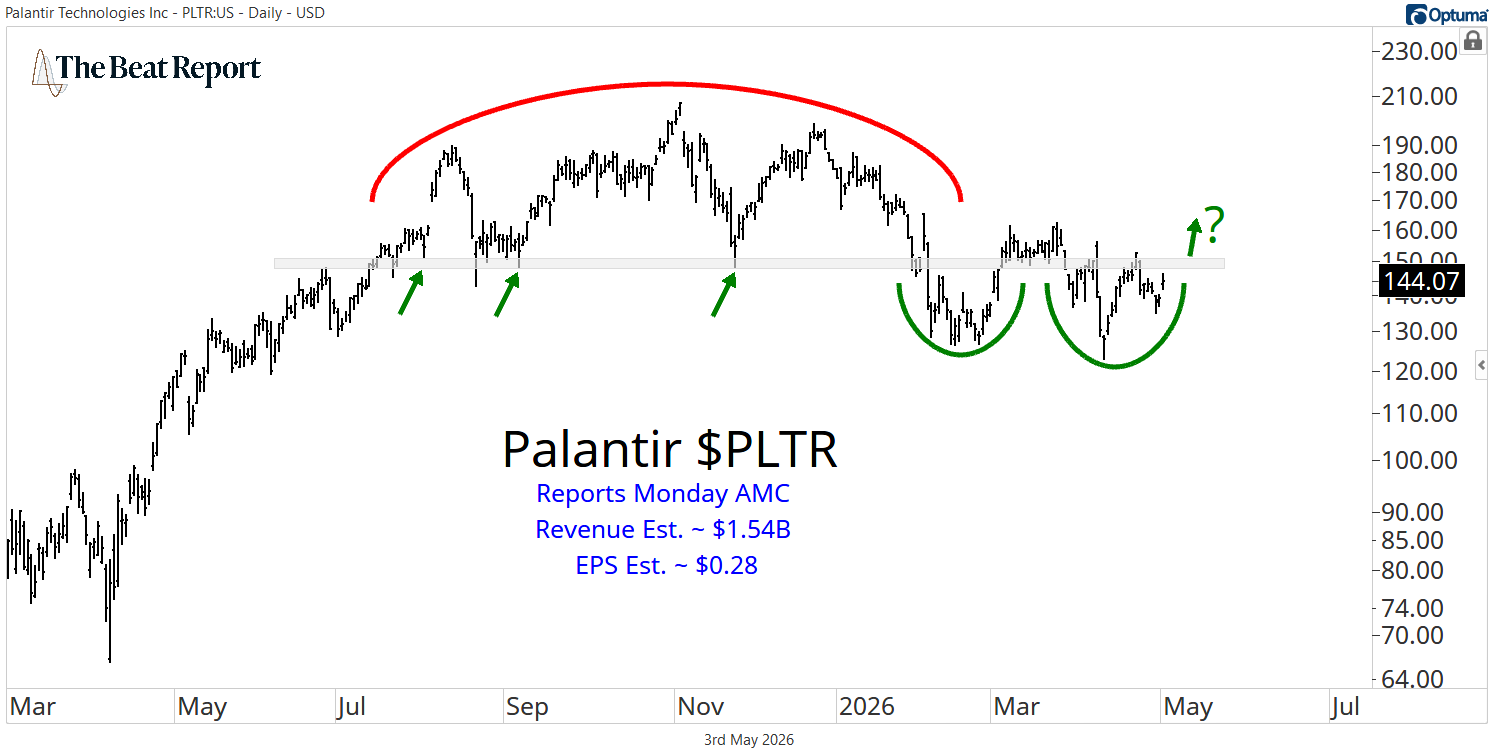

Then there is Palantir...

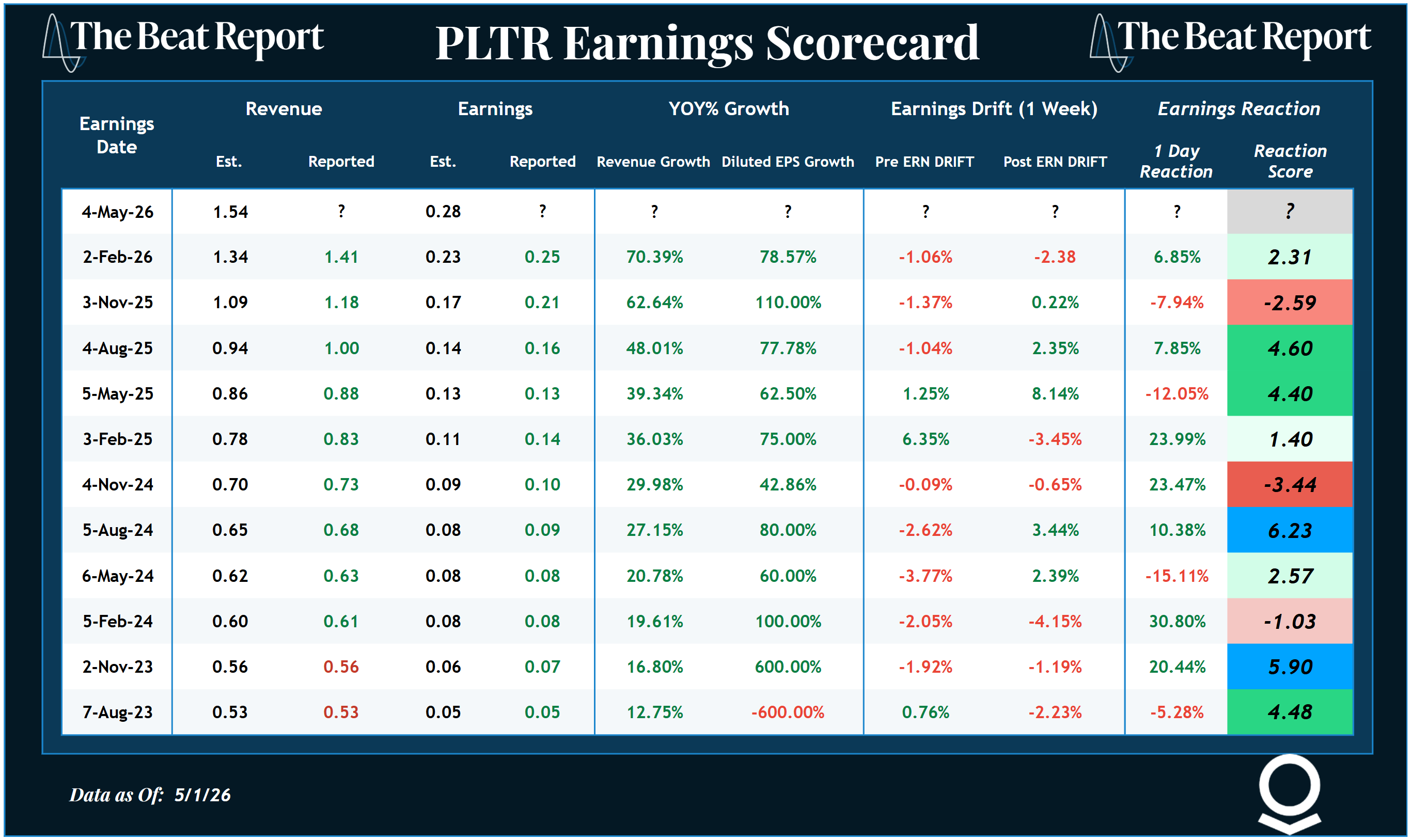

Palantir reports Monday after the close, and this is the most important report of the week for the speculative growth trade.

The market is looking for roughly $1.54 billion in revenue and $0.28 in EPS, and technically, the stock is sitting right below a key level of interest.

Earlier this year, Palantir looked like it had resolved a massive top, but instead of following through to the downside, the stock has spent the past several weeks churning sideways below the neckline.

If sellers were really in control, we should have seen downside acceleration by now. But we haven’t.

Instead, the stock is coiling right beneath resistance, setting up the possibility of a scoop-n-score move if earnings are strong enough.

What's more, the fundamentals are certainly not the issue here.

Palantir’s fourth quarter was ridiculous... Revenue grew 70% year-over-year, its highest growth rate as a public company, while U.S. revenue grew 93% and U.S. commercial revenue surged 137%.

The company also posted a Rule of 40 score of 127%, closed a record $4.3 billion in total contract value, and guided for 61% revenue growth in 2026.

This is hands-down the greatest growth story we've ever seen in software.

So again, the question is not whether the business is growing; it's what the market is willing to pay for that growth.

Palantir’s earnings reactions over the past year have not really established a clean trend. We've seen negative, positive, negative, positive.

But if the stock rallies after this report, it would establish a new positive earnings sentiment trend at exactly the right time.

Moreover, the stock is sitting just below a major technical level that could spark a massive squeeze higher.

As one of the poster children for the high-valuation AI trade, PLTR's earnings reaction will have ramifications for many other high-flying stocks.

Heading into the report, all eyes are on 150. Above there, the squeeze is on. Below it, and more consolidation is likely needed.

That's it for this week. Thank you for reading!

-The Beat Team

P.S. Every day, Spencer sits across from some of the smartest analysts and traders in the business and listens to their best ideas.

So we built the SMTV Portfolio to put real money behind these ideas.

This includes long-term core positions, swing trades, and options.