Earnings season is fading, but these reports could still tell us a lot about risk appetite and sector rotation.

June 14, 2026

WHAT ARE YOUR THOUGHTS? On Friday, SpaceX $SPCX completed the largest IPO in market history. It closed with a total market capitalization of $2.1 trillion.

Do you think SPCX will hit a market capitalization of $1 trillion or $4 trillion first?

Write us at [email protected]. We value your input and may feature your responses in a future post.

The busiest stretch of earnings season is behind us, but there are still plenty of big reports coming out.

Last week, we heard from some big names in the discretionary, staples, and tech sectors.

And the earnings reactions were all over the place!

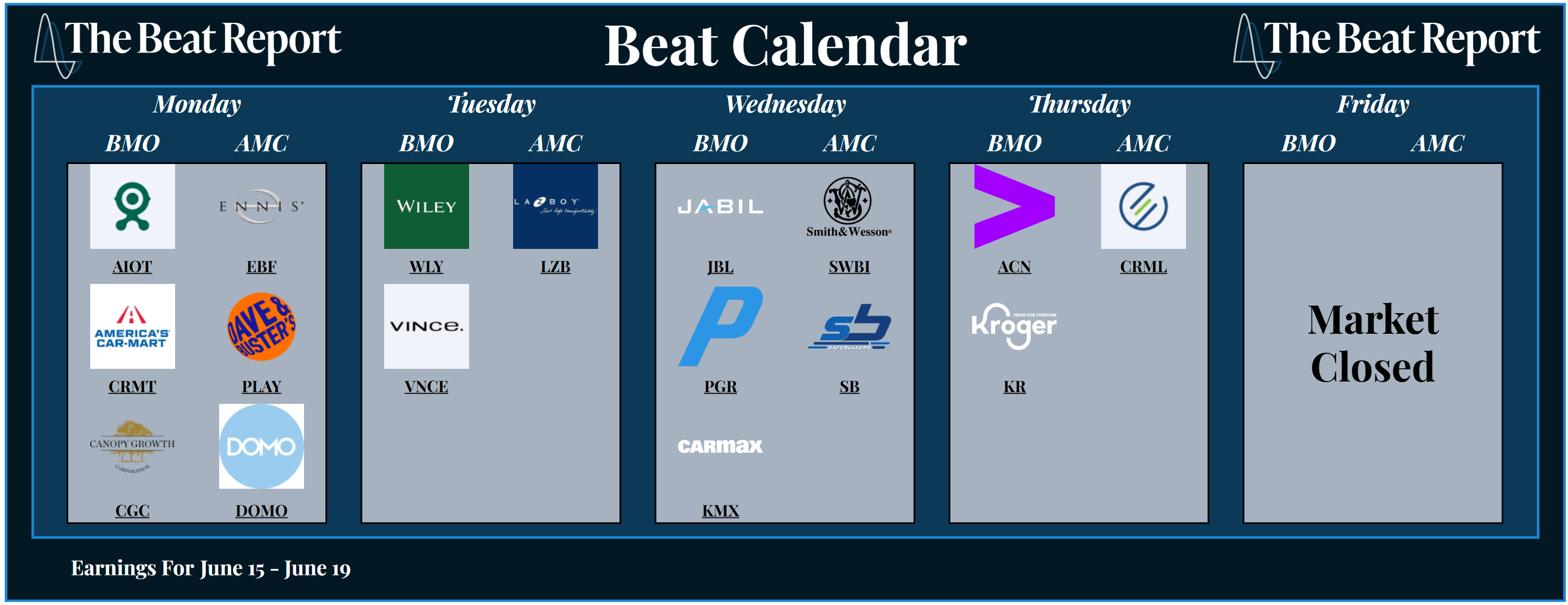

This week, we have the lightest earnings calendar since earnings season began in April, but there are still several key earnings reports to keep on your radar.

But before we look ahead, let’s review what we learned last week.

Following a big double beat, Cooper Companies $COO rallied 8.6% for its best earnings reaction in 8 quarters. The stock is hanging on for dear life at the lower bound of a massive potential distribution pattern.

Despite beating the headline expectations across the board, Lululemon $LULU fell 8.6%, putting the finishing touches on a massive top. Gross margin declined by 410 basis points YoY, and North American comparable sales dropped by 6% YoY.

Following a mixed earnings report, The Campbell's Company $CPB suffered its 3rd consecutive negative earnings reaction. However, the stock is now at the same level that marked the bottom in the early 2000s.

With CPB set to be kicked out of the S&P 500 on June 22, and a complete sentiment washout, we believe this name is one of the most interesting turnaround stories in the consumer staples sector.

After crushing the market's headline expectations, J.M. Smucker $SJM rallied 10.4% for its best earnings reaction since 2008. And while the technicals are still in a downtrend, we believe the stage is set for a major reversal.

In addition to the shift in earnings sentiment, diluted EPS growth snapped a streak of four consecutive quarters of contraction and is now at the highest level since 2023. So what we have here is a stock with improving fundamentals and earnings sentiment. Now all we need to see is the price confirm the shift.

Following a blockbuster earnings report, Casey's General Stores $CASY rallied more than 20% for its best earnings reaction since 2009. The stock closed at a new all-time high, confirming that the primary trend is unmistakably higher across all timeframes.

In the report, EPS growth accelerated to 66% YoY, the best we've seen in years. This is being driven by margin expansion across products such as pizzas, appetizers, non-alcoholic beverages, and more.

Despite reporting a big double beat, Oracle fell 8.5% for its worst earnings reaction since 2023. And while the stock is carving out a bearish-to-bullish reversal pattern, this earnings reaction was a major setback.

In the report, all of the key fundamental metrics improved, but earnings sentiment and the technicals are holding this stock back.

What's happening next week 👇

Earnings season is slowing to a crawl.

After the nonstop flood of reports we’ve been writing about since April, next week is shaping up to be the quietest stretch of the entire season.

There are still a handful of names on the calendar, but the big stories are much easier to isolate.

We’re watching three reports in particular: Jabil $JBL, Accenture $ACN, and Kroger $KR.

The first is a clear leadership stock.

The second is a broken former leader trying to repair.

And the third is a defensive consumer staples name testing a key support level, with one of the better earnings scorecards in its sector.

That gives us three very different setups, and all three reports should tell us something useful about where investors are still willing to put money to work.

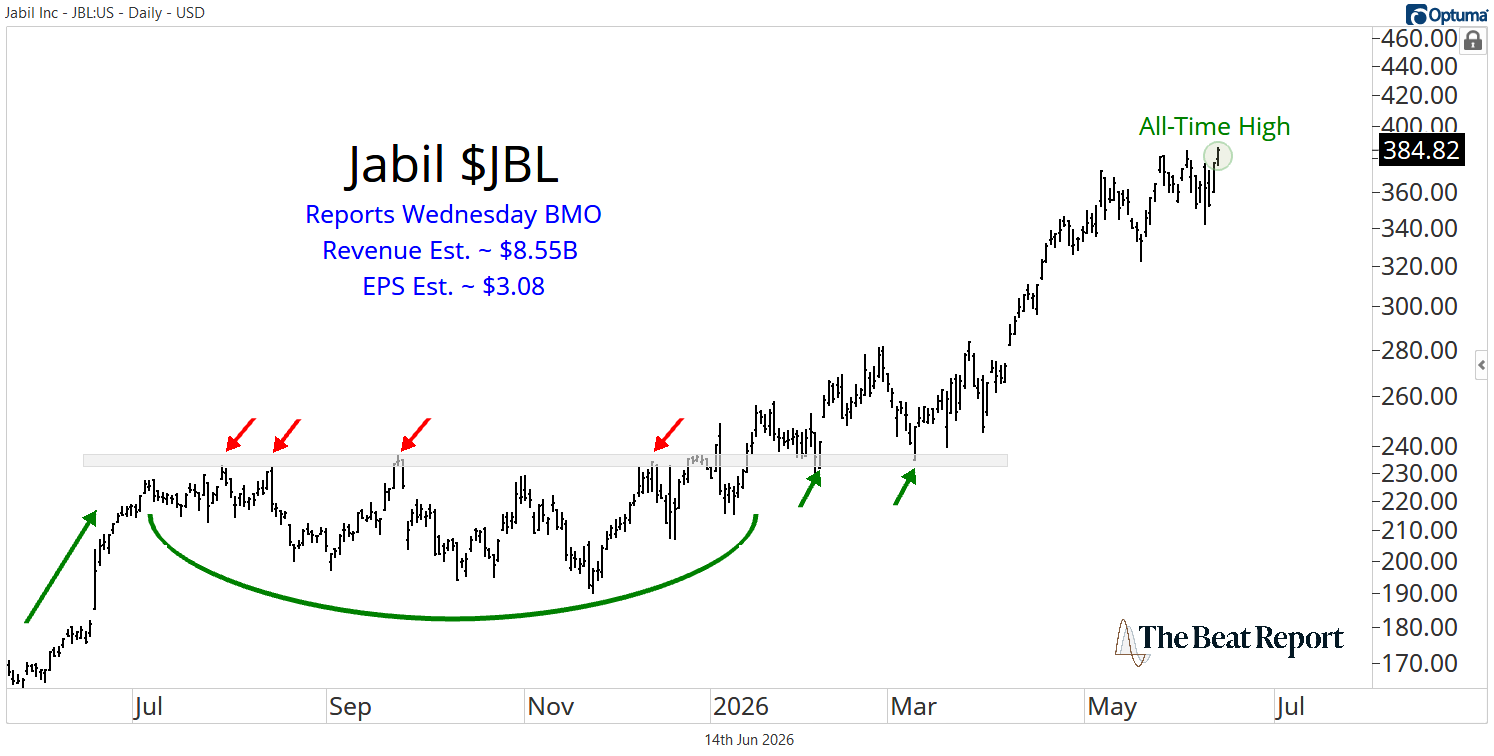

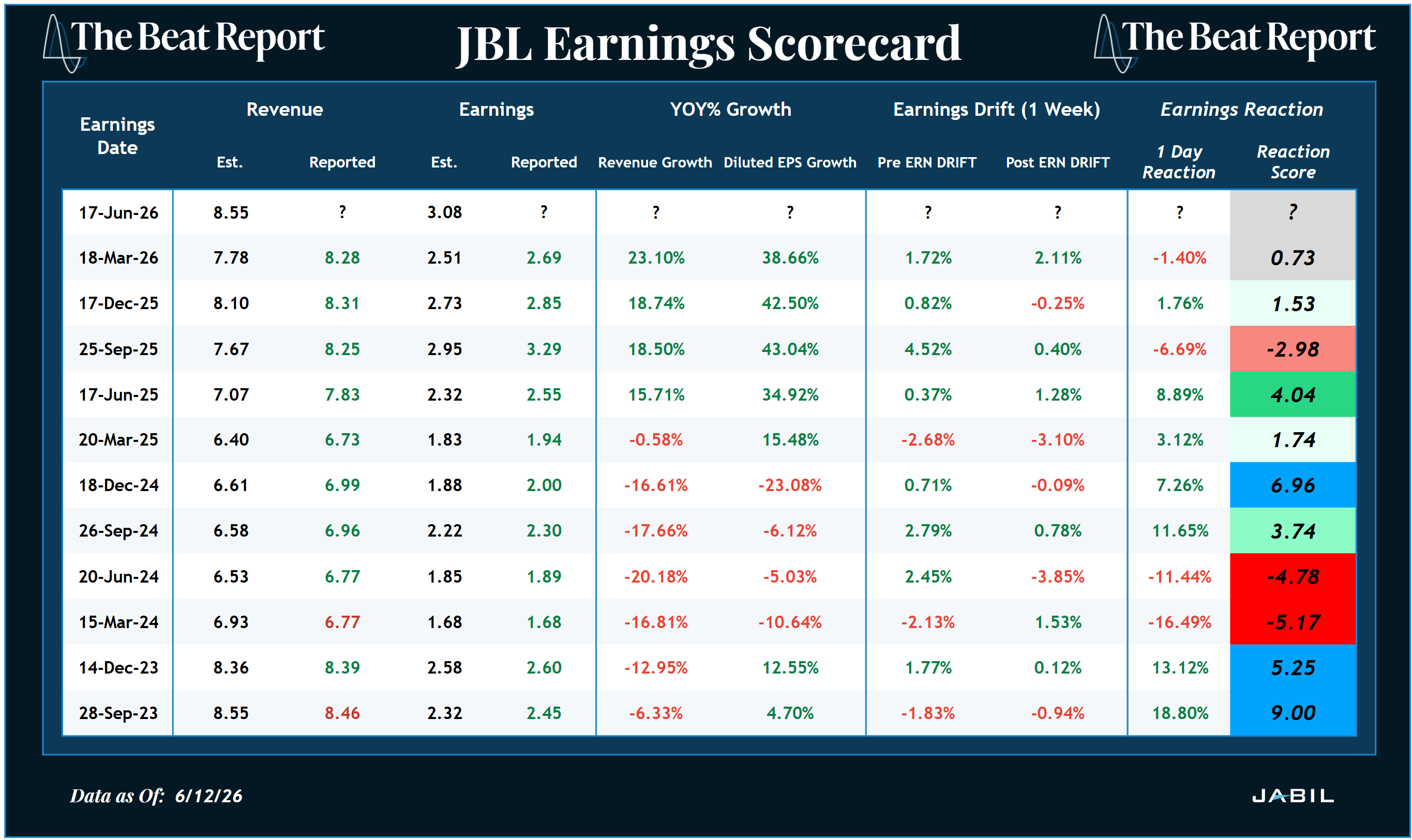

Jabil reports on Wednesday before the market opens, and the market is looking for $8.55 billion in revenue and $3.08 in earnings per share.

This is the strongest chart of the group by a mile.

After consolidating through the second half of 2025, JBL broke out at the beginning of 2026, entered a brand new primary uptrend, and has been ripping to new all-time highs ever since.

The stock closed Friday at another fresh record high, and there's nothing bearish about that kind of persistent demand.

The earnings scorecard is not perfect, but the fundamental trend is hard to argue with.

Revenue growth has been consistently strong, EPS growth has been even stronger, and buyers have been willing to accumulate the stock ahead of earnings.

And that makes sense when you look under the hood.

Last quarter, Jabil beat expectations across revenue, operating margin, and EPS, then raised its fiscal 2026 outlook.

The Intelligent Infrastructure segment remains the main growth engine, with strength across cloud and data center infrastructure, networking and communications, and capital equipment.

In other words, this uptrend is backed by solid fundamentals.

Jabil is directly tied to several of the market’s largest spending cycles: AI infrastructure, cloud data centers, networking, automation, renewables, healthcare, and advanced manufacturing.

And based on the alignment in technicals, fundamentals, and earnings sentiment, we expect JBL to be rewarded for its earnings report this week.

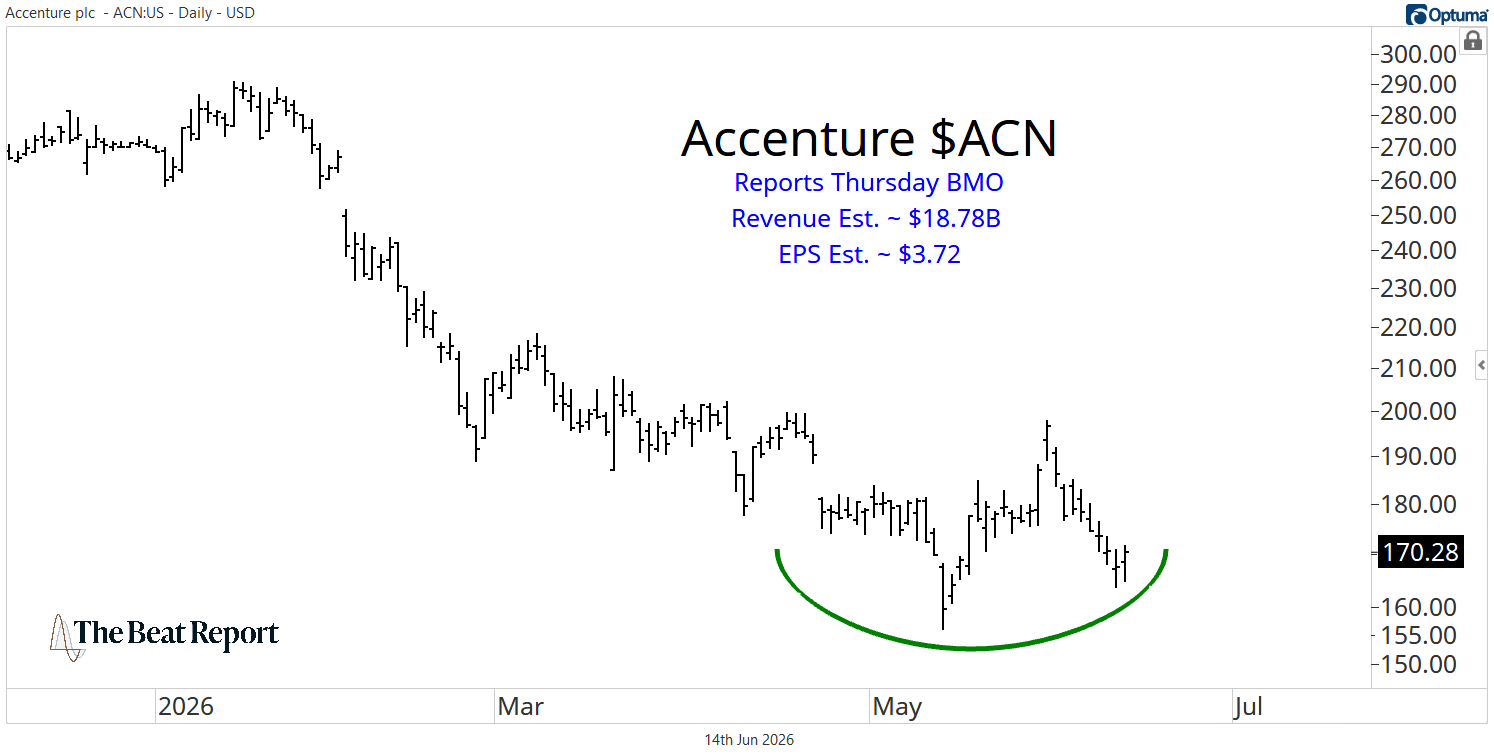

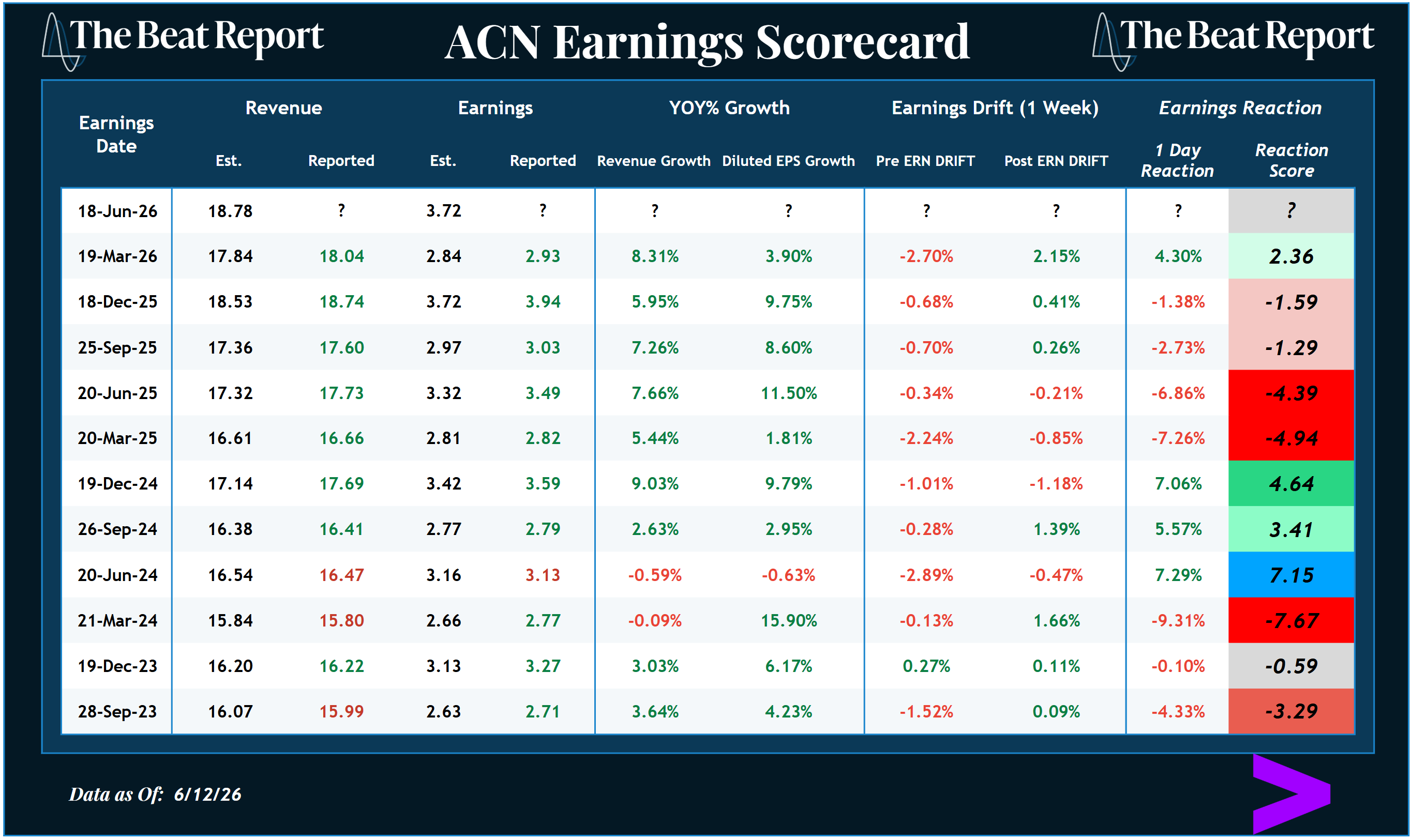

Next up is Accenture, which reports Thursday before the market opens.

The market is looking for $18.78 billion in revenue and $3.72 in earnings per share.

Accenture has been a disaster in 2026, falling from roughly $300 to almost $150 before finally stabilizing in recent weeks.

And while the stock is still in a primary downtrend, downside momentum has started to fade, and ACN is attempting to carve out the early stages of a bearish-to-bullish reversal pattern.

The earnings scorecard makes this one interesting.

After four consecutive negative earnings reactions, Accenture finally rallied last quarter, snapping its beatdown streak and giving bulls the first sign that earnings sentiment may be shifting from a headwind to a tailwind.

But that doesn't mean the stock is fixed.

Revenue and earnings are still growing, but the growth rate has been slowing, especially on the earnings side.

EPS growth fell from 11.5% a year ago to 3.9% last quarter, and the stock has now posted nine consecutive quarters of negative pre-earnings drift.

In other words, investors have been selling this stock before reports for more than two years.

Still, the business isn't broken.

Last quarter, Accenture delivered record bookings of $22.1 billion, expanded its operating margin, and generated strong free cash flow.

Management also continues to lean heavily into AI, data, cybersecurity, data centers, energy infrastructure, and enterprise reinvention.

What's more, the company already has more than 85,000 AI and data professionals, and revenue from its top 10 ecosystem partners continues to outpace overall growth.

So the setup heading into earnings is simple.

The chart is ugly, but improving. The fundamentals are solid, but slowing. And earnings sentiment has been terrible, but may have just turned.

If ACN rallies again this week, the bottoming case becomes much more compelling.

Meanwhile, if ACN is punished, the stock will likely need more time to carve out a base.

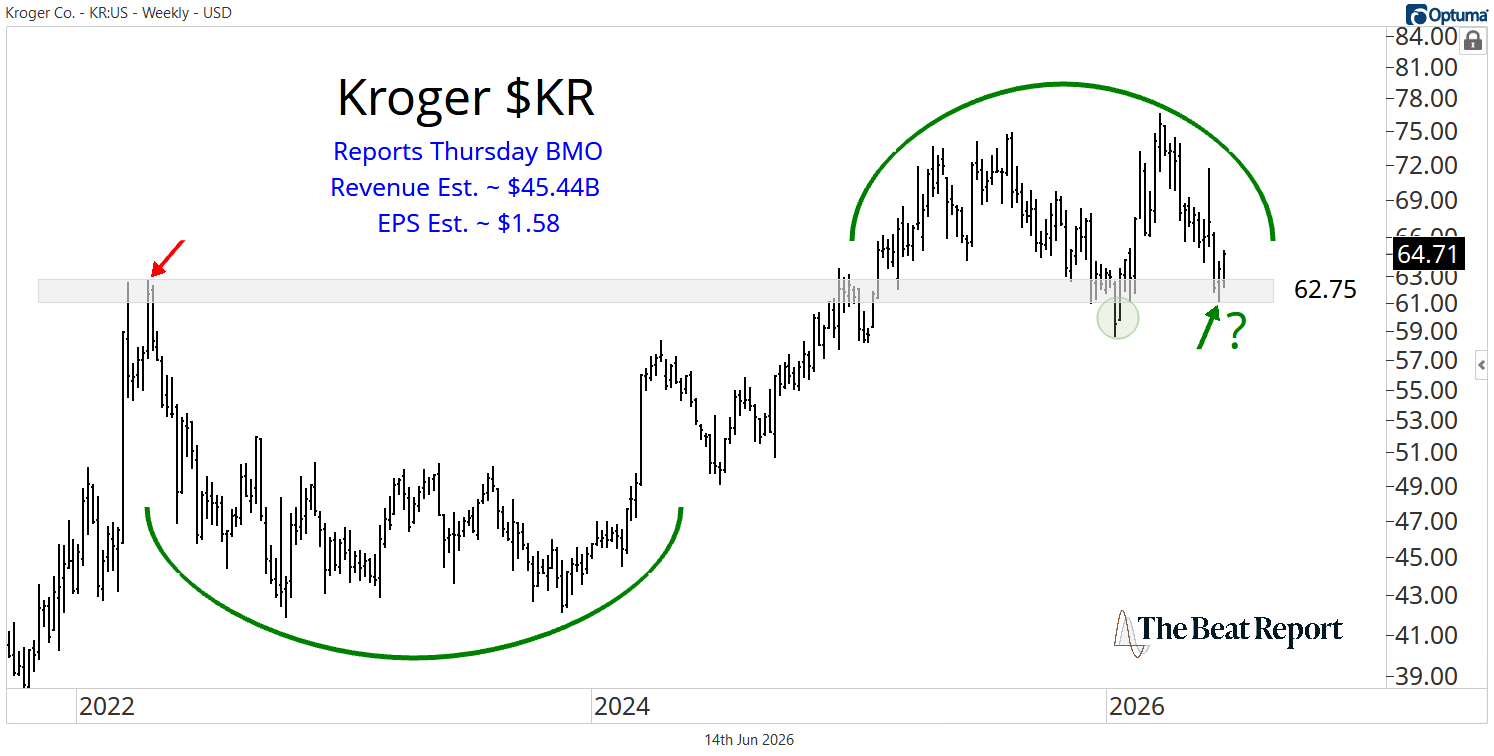

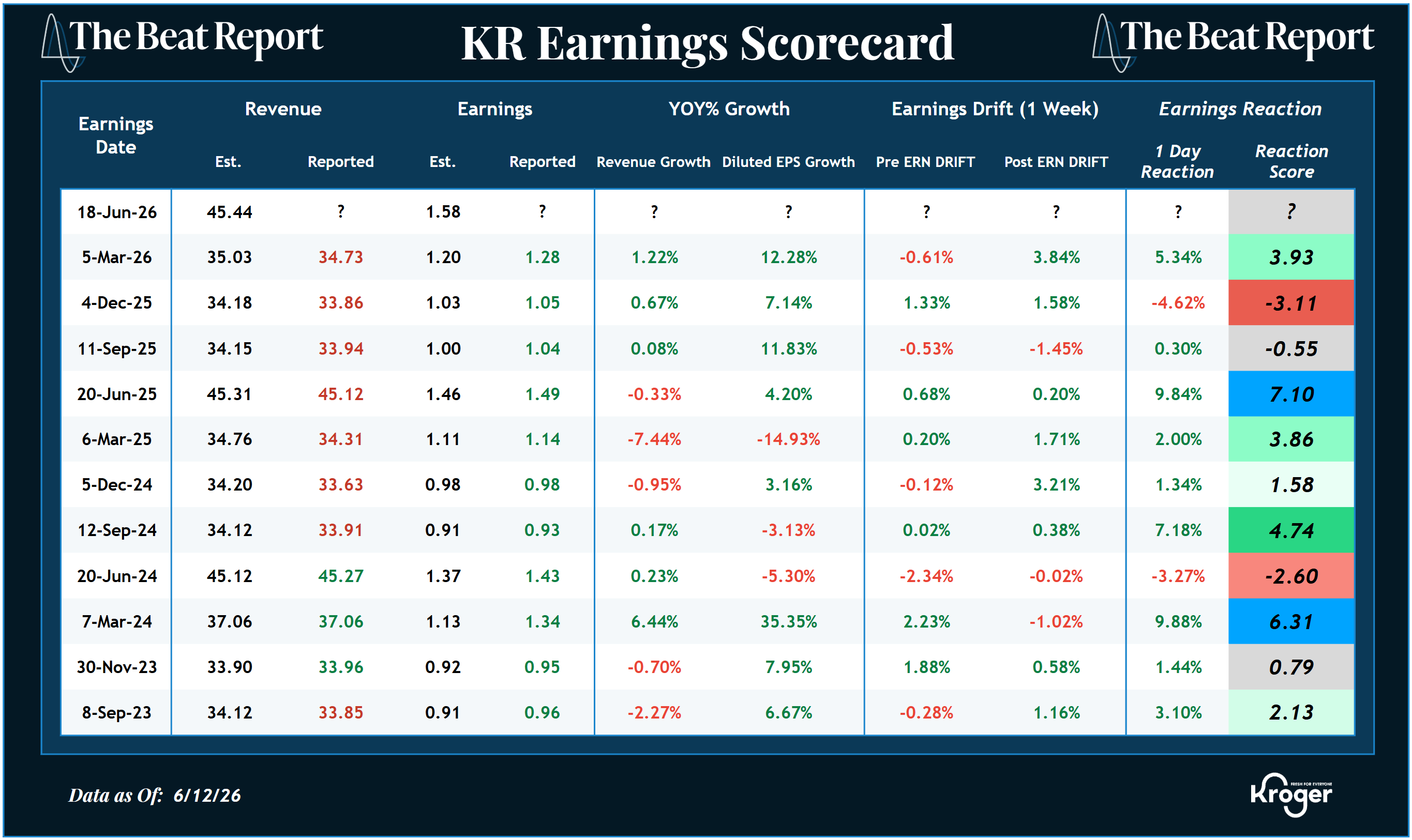

Finally, we have Kroger, which reports Thursday before the market opens.

The market is looking for $45.44 billion in revenue and $1.58 in earnings per share.

Kroger has been range-bound for the better part of the past year and a half, but the bigger picture is still constructive.

Early last year, the stock broke out above its 2022 peak, then spent the rest of 2025 and this year flipping that former resistance zone into support.

That level is roughly $62.75.

As long as buyers defend that area, this looks like healthy consolidation after a big advance.

But if Kroger loses it, there will likely be a big leg lower.

The earnings scorecard is the best part of the story and leads us to believe that buyers will maintain control of price action.

Kroger has been rewarded for six of its last seven earnings reports, which is some of the strongest earnings sentiment we have seen anywhere in consumer staples.

The company doesn't always beat revenue estimates, but it has consistently beaten earnings expectations, and the market has mostly rewarded that execution.

Last quarter, Kroger delivered identical sales growth without fuel of 2.4%, and adjusted e-commerce sales growth of 20%.

Management also highlighted improving market-share trends, better customer-value perception, stronger e-commerce execution, and continued progress in simplifying the business.

This isn't the sexiest story in the market, but we believe it's one of the most attractive in the consumer staples sector.

Heading into this week's earnings report, we're monitoring if KR can hold $62.75 and keep its positive earnings sentiment streak intact.

If it can, the odds favor this long consolidation eventually resolving higher.

But if it cannot, KR will probably stay stuck in the messy range for a while longer.

This is exactly why we built the Premium Beat Report.

In the free Weekly Beat, we show you the biggest earnings setups on our radar.

But in the Premium Beat Report, we go a step further and turn our best setups into actionable trade ideas.

We’re looking for stocks where the fundamentals, earnings sentiment, and technicals are all lining up.

When the next one triggers, Premium Beat Report members will hear about it first.

Editor's Note: More than a trillion dollars in new equity is about to hit the public markets, and Steve thinks most traders are about to be standing on the wrong side of it.

He's hosting a FREE live training on June 17th at 4:30 pm ET to show you where that money is actually headed.