These stocks failed their earnings tests as weak charts and bad sentiment kept sellers in control.

June 15, 2026

The mainstream was locked in on SpaceX Friday, and for good reason.

The largest IPO in market history is an event that deserves attention. When a company that important goes public, every investor on the planet wants to know what it means for the market, the economy, and the next generation of public equities.

But while everyone was staring at SpaceX, the earnings tape was sending another message.

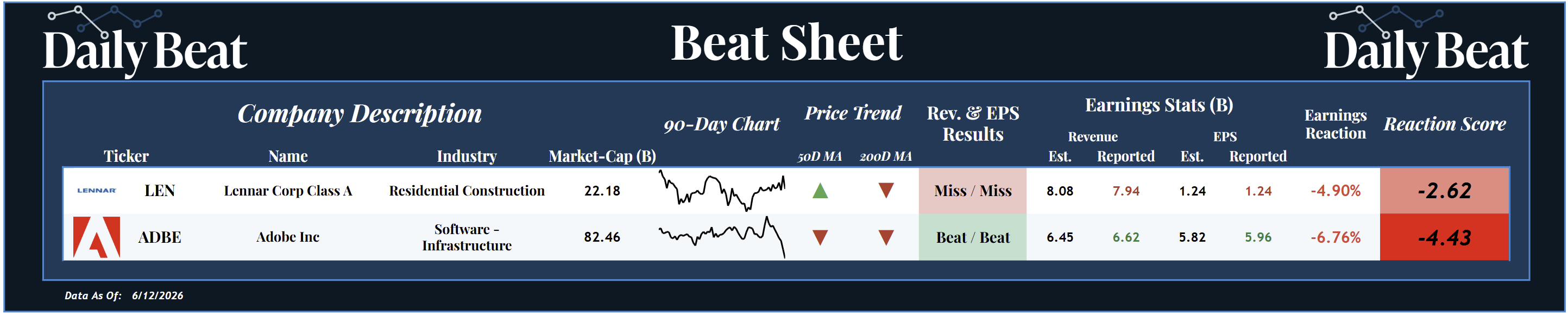

Friday gave us two S&P 500 earnings reactions, and neither one came from a leadership stock.

They came from Adobe $ADBE and Lennar $LEN, two names that have already spent the better part of the past year proving they are not where investors want to be.

That matters because earnings reactions do not happen in a vacuum.

A strong stock can absorb bad news and keep grinding higher.

A broken stock can report decent numbers and still get punished.

And that's why we do fusion analysis at The Beat Report, combining the technicals, the fundamentals, and the earnings sentiment to figure out whether a company is actually being rewarded by the market.

On Friday, the answer was clear.

The market wanted nothing to do with either of these stocks.

*Click the image to enlarge it

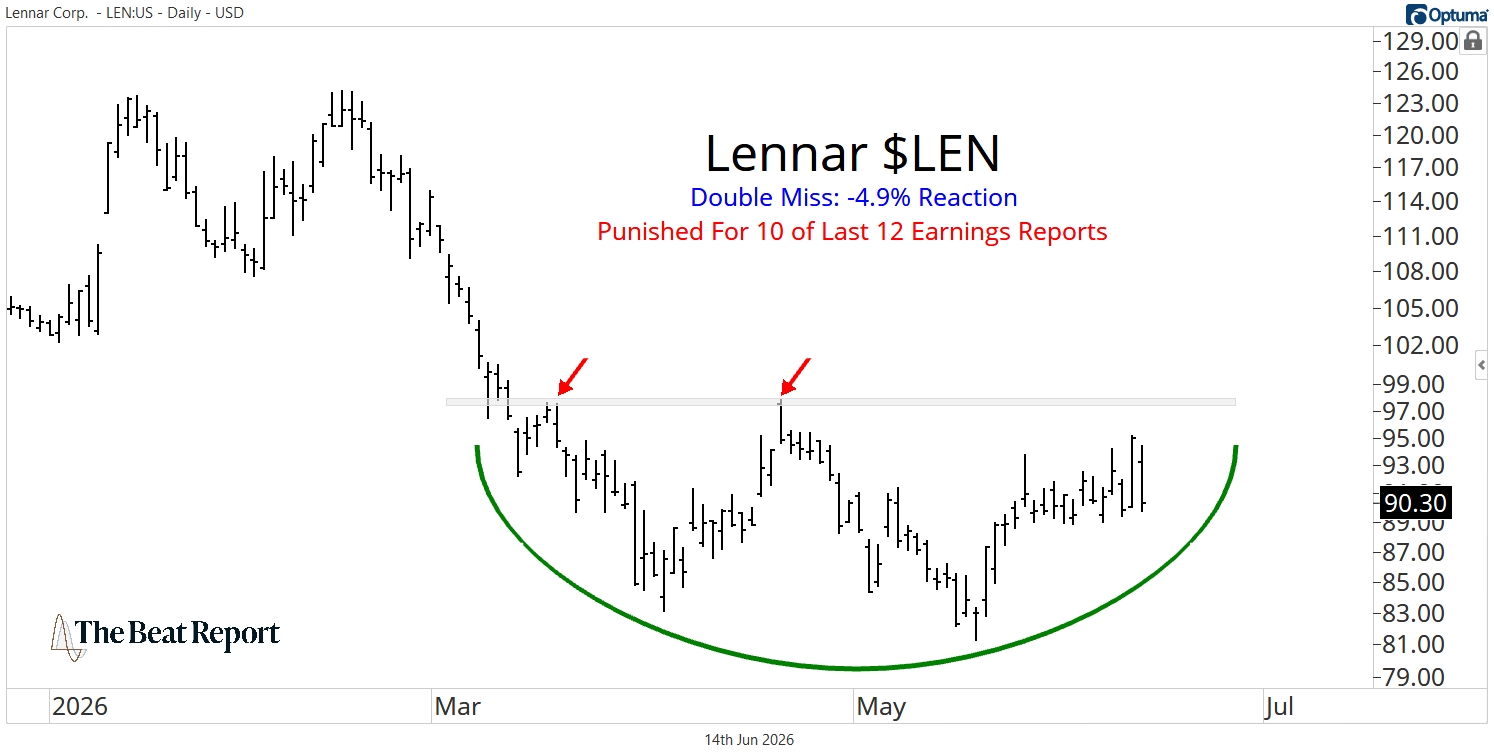

Lennar had the better reaction of the two, but that's not saying much.

The homebuilder missed headline expectations across the board, with revenue of $7.94 billion versus estimates of $8.08 billion and earnings per share of $1.24 versus estimates of $1.24.

As a result, LEN fell 4.9%, giving the stock a reaction score of -2.62 and continuing its trend of one of the ugliest earnings sentiment profiles in the S&P 500.

This stock has now been punished for 10 of its last 12 earnings reports.

And that's about as bad as it gets.

Technically, Lennar has been a mess all year.

Lennar suffered a sharp decline in early 2026, then spent the past few months chopping sideways and carving out what could eventually become a bearish-to-bullish reversal pattern.

The problem is that “could” is doing a lot of work.

Even if Lennar breaks above the upper bound of this short-term base, it would be hard to have much conviction because the other two pieces of the process are still missing.

The fundamentals are under pressure, and earnings sentiment remains firmly bearish.

In their latest report, Lennar delivered 20,519 homes, up 2% from last year, but new orders fell 4% to 21,749 homes.

At the same time, margins are contracting.

And while the management team is doing what it can, the bigger backdrop remains difficult, with elevated mortgage rates, stretched affordability, cautious buyers, and a housing market that still requires incentives to get deals across the finish line.

Lennar may eventually become a buyable stock, especially if rates fall, affordability improves, and the stock completes its reversal pattern.

But right now, Lennar is still a weak chart with weak earnings sentiment and fundamentals that aren't strong enough to change the story.

So we aren't interested in touching LEN.

If Lennar was bad, Adobe was worse.

Heading into the report, we knew exactly where the line in the sand was.

In a recent Weekly Beat note, we highlighted the 2022 bear market low near $275 as the key level for Adobe.

That zone had acted as support during the prior cycle, and over the past few months, the stock had been coiling beneath it.

Above $275, the squeeze was on, and below it, the stock remained vulnerable.

Friday answered the question.

Adobe reported a double beat, with revenue of $6.62 billion versus estimates of $6.45 billion and earnings per share of $5.96 versus estimates of $5.82.

On paper, that looks fine...

But the stock fell 6.8% anyway.

That decline pushed Adobe to its lowest level since 2018 and confirmed a fresh leg lower after months of failed attempts to reclaim that former support zone.

ADBE has now been punished in 10 of its last 12 earnings reports, which suggests the problem here is not a one-off reaction.

This is a deeply bearish earnings sentiment regime.

And the chart is even worse.

Adobe peaked in late 2023 and early 2024 at above $600 per share.

Today, it's trading near $200, having lost roughly two-thirds of its value while the broader software space has produced plenty of winners.

The frustrating part is that Adobe’s fundamentals are not terrible.

The company reported record Q2 revenue of $6.62 billion, up 13% YoY.

AI-first ARR more than tripled YoY and exceeded $500 million.

What's more, Adobe is still pushing hard into Acrobat, Express, Creative Cloud, Firefly, GenStudio, customer experience orchestration, and AI-powered workflows.

Management even raised its full-year revenue and non-GAAP EPS targets.

But the market did not care, and that's the whole point.

Adobe has a real AI product story, but none of that matters if the stock keeps failing at resistance and investors keep using earnings reports as an excuse to sell.

And that's why we want nothing to do with ADBE.

At The Beat Report, we are not here to buy famous names just because they look cheap.

We're here to find stocks where the fundamentals, earnings sentiment, and price action are all pointing in the same direction.

Adobe and Lennar are not there.

They may get there someday, but they are not there today.

This is exactly why we built the Premium Beat Report.

In the free Daily Beat, we show you what the market rewards and rejects after earnings.

In the Premium Beat Report, we turn that process into actionable trade ideas by focusing on stocks where fundamentals, earnings sentiment, and technicals all line up.

When the next setup triggers, Premium Beat Report members will hear about it first.

Editor's Note: More than a trillion dollars in new equity is about to hit the public markets, and Steve thinks most traders are about to be standing on the wrong side of it.

He's hosting a FREE live training on June 17th at 4:30 pm ET to show you where that money is actually headed.