The biggest wave of reports is behind us, but the earnings tape is still giving us actionable clues.

June 21, 2026

WHAT ARE YOUR THOUGHTS? This week, Kevin Warsh spooked the market with his hawkish tone during his first Federal Reserve meeting.

Do you think we'll see interest rate hikes before the mid-term elections?

Write us at [email protected]. We value your input and may feature your responses in a future post.

The earnings calendar is finally starting to slow down, but the market isn't

Last week gave us a little bit of everything: broken software stocks making new lows, small-cap healthcare waking up, space stocks stealing the spotlight, regional banks holding firm in a tough tape, and two major S&P 500 names getting absolutely smoked after earnings.

That's exactly why we track this stuff every day.

The major averages can tell one story, while the earnings tape tells another.

And right now, that tape is still giving us a clean read on where buyers are showing up, where sellers are taking control, and which stocks deserve our attention as we head into the next leg of this bull market.

Following a big double miss, Lennar $LEN fell nearly 5%, marking its tenth negative earnings reaction out of the last twelve. And while the homebuilders have been showing strength recently, this name remains a significant laggard.

One of the world's largest software providers, Adobe $ADBE beat the market's headline expectations, but cratered nearly 7% to its lowest level since 2018. AI-first ARR more than tripled YoY and exceeded $500 million, but the market didn't care. ADBE remains one of the worst-performing software stocks in the market.

There were no S&P 500 earnings reactions to cover, so we highlighted one of our favorite themes right now: small-cap healthcare.

Inside this theme, the setup in Molina Healthcare $MOH stands out. Not only does the stock have a textbook bearish-to-bullish reversal pattern, but we also saw a significant shift in earnings sentiment this quarter.

Again, there were no S&P 500 earnings reactions to cover, so we highlighted one of our favorite space stocks. Its name is MDA Space $MDA, and it's a a $5.5 billion Canadian space stock with exposure to some of the most important growth areas in the modern space economy, including satellite systems, geointelligence and Earth observation, space robotics, lunar infrastructure, and defense-related space capabilities.

The best part? The technicals, fundamentals, and earnings sentiment are all pointing higher right now.

In a tough tape, Jabil $JBL and Regions Financial $RF had negative earnings reactions in absolute terms, but both stocks actually posted positive reaction scores. Both stocks also beat their headline expectations across the board.

JBL hit a new all-time high intraday, and RF looks poised to lead the next leg higher in the regional bank industry.

In reaction to mixed earnings reports, Kroger $KR and Accenture $ACN cratered 8.4% and 18%, respectively. They also broke key technical levels...

KR broke down to a new 52-week low, while ACN resolved a massivetop and closed at the lowest level since 2017. We expect these stocks to continue drifting lower over the coming days and weeks.

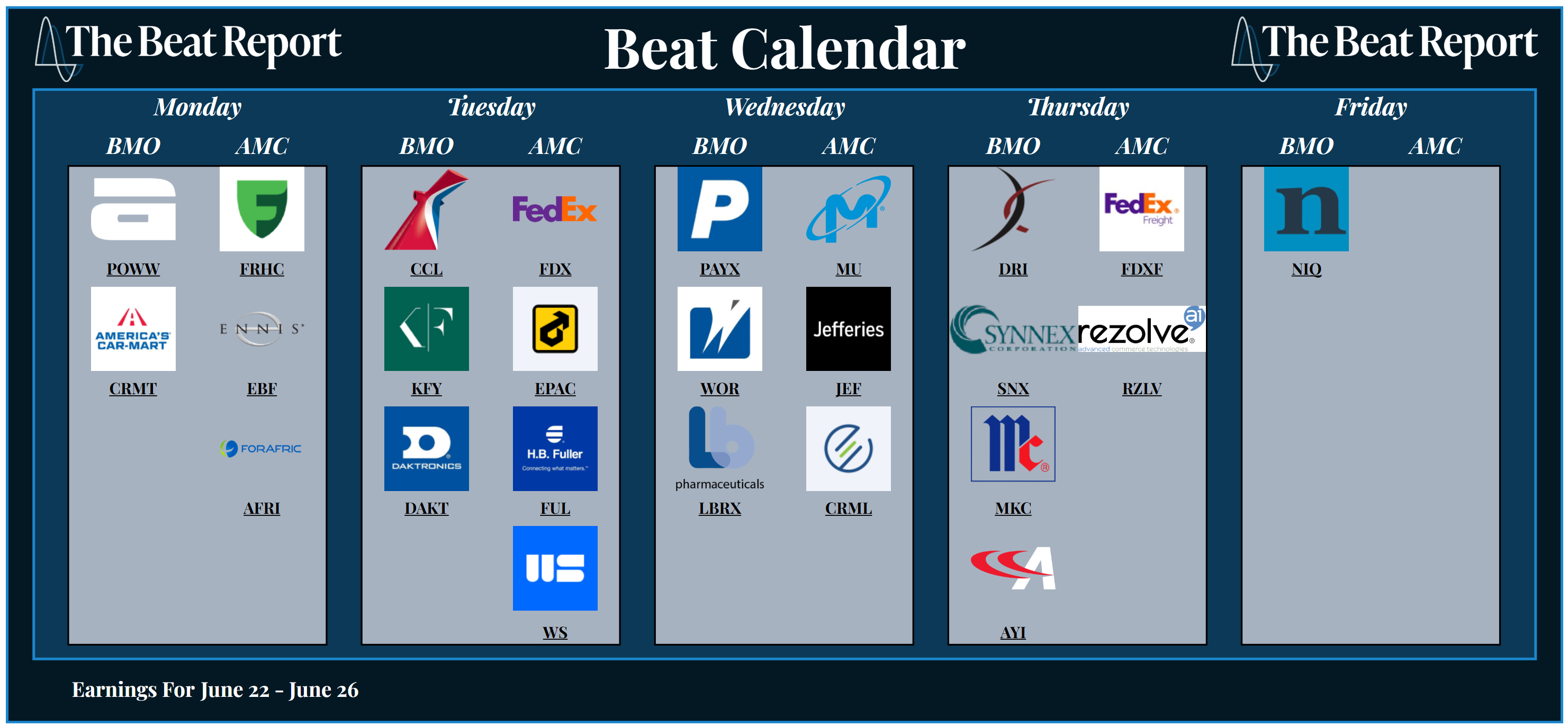

What's happening next week 👇

After the nonstop flood of reports we’ve been covering since April, next week’s calendar is much lighter.

But it's far from empty...

We still have a handful of notable reports coming up, including Carnival $CCL, FedEx $FDX, FedEx Freight $FDXF, Paychex $PAYX, Micron $MU, Jefferies $JEF, Worthington Steel $WS, and many more.

That gives us a good mix of transports, consumer discretionary, industrials, financials, software, food, and semiconductors.

But the three reports we’ll be watching closest are FedEx, Carnival, and Paychex.

Each one tells a different story...

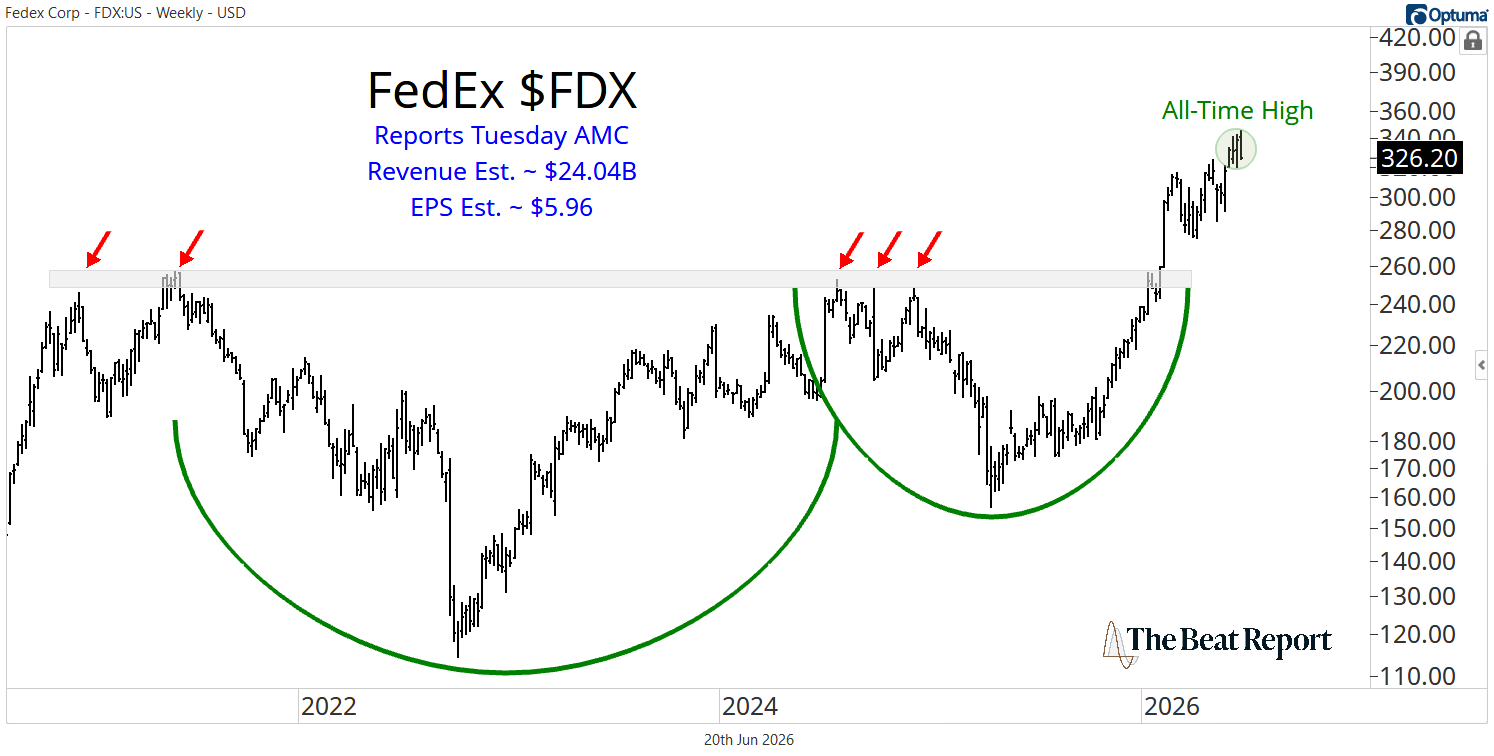

FedEx is the cleanest leadership chart of the group.

Carnival is the big base breakout candidate.

And Paychex is the former laggard trying to complete a reversal pattern.

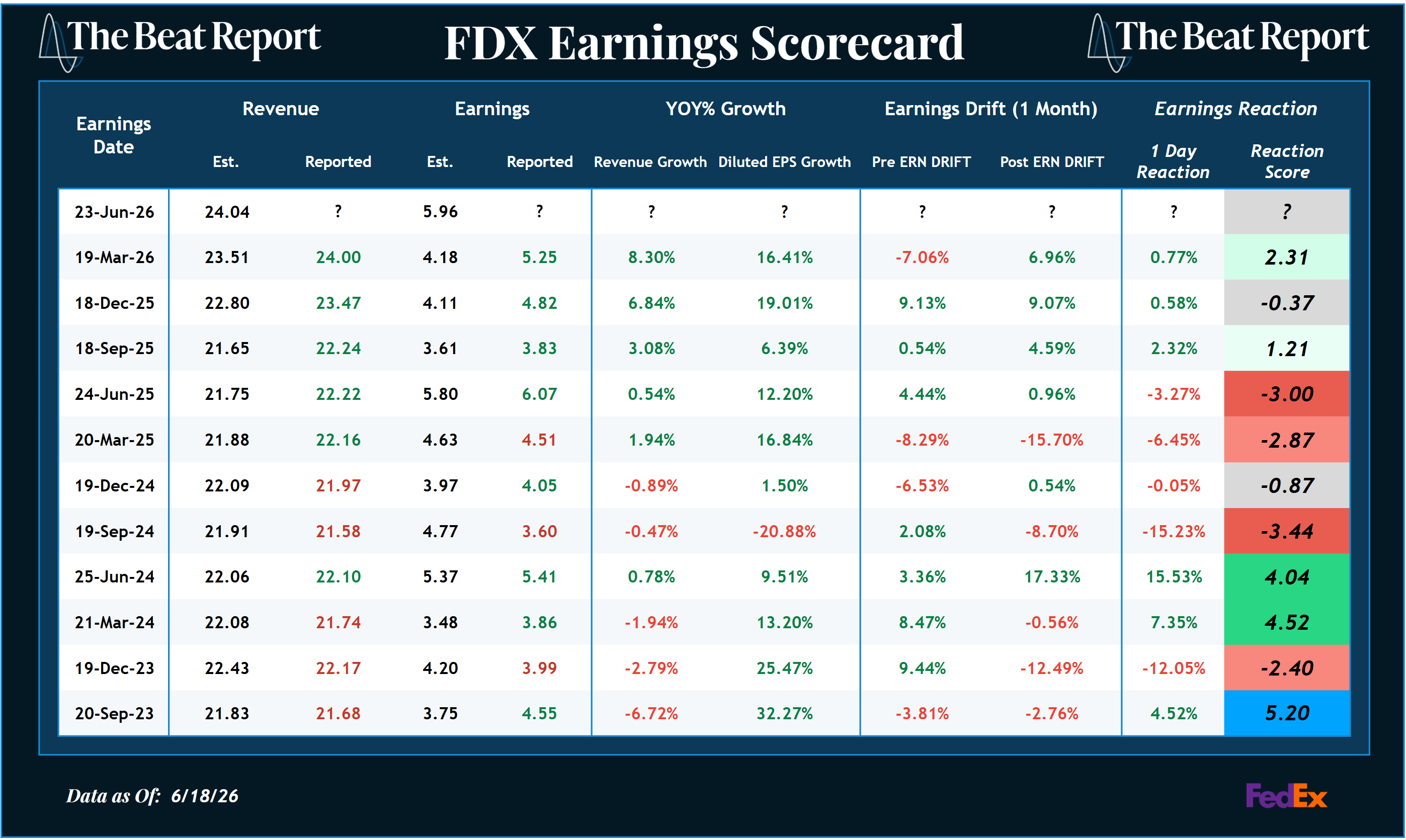

Let’s start with FedEx, which reports Tuesday after the close, and the market is looking for $24.04 billion in revenue and $5.96 in earnings per share.

FedEx has turned into one of the most important economic bellwethers in the market.

This is a massive integrated logistics company that moves packages, freight, documents, inventory, and time-sensitive goods worldwide.

And when FedEx is working, it usually says something important about global trade, business activity, and the physical economy.

Right now, the chart is working beautifully.

FedEx broke out from a massive multi-year base earlier this year and has been marching to fresh all-time highs ever since.

That's exactly where we want to find stocks heading into earnings.

What's more, the earnings scorecard backs up the chart.

FedEx has beaten headline expectations across the board in four consecutive quarters, and both revenue and earnings growth have been positive for five straight quarters.

The stock has also posted three consecutive positive one-day earnings reactions, while pre- and post-earnings drift have been consistently positive.

In other words, buyers have been accumulating shares before, during, and after earnings.

That's exactly what healthy earnings sentiment looks like.

And the fundamental story is also improving.

The company is benefiting from stronger U.S. domestic and International Priority package yields, cost savings from transformation initiatives, higher domestic package volume, and progress across its Network 2.0 strategy.

Management has also been moving FedEx toward a cleaner, more focused operating structure after the FedEx Freight separation, which should give investors a better read on the core integrated logistics business.

So the setup heading into Tuesday is simple.

If FedEx rallies, it would confirm that this breakout still has legs.

But if it fails to rally on another solid report, that would not necessarily kill the trend, but it would be the first sign that expectations may be catching up with the move.

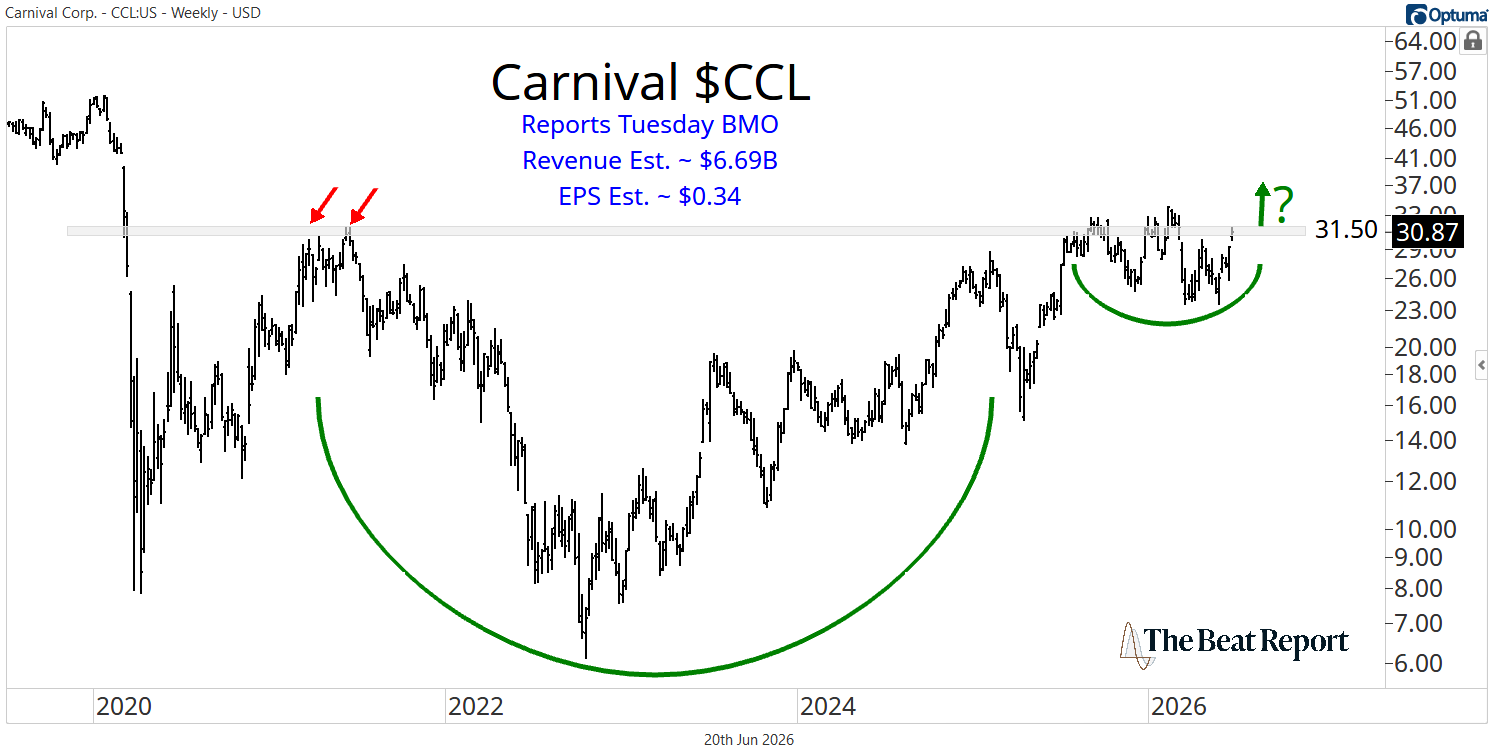

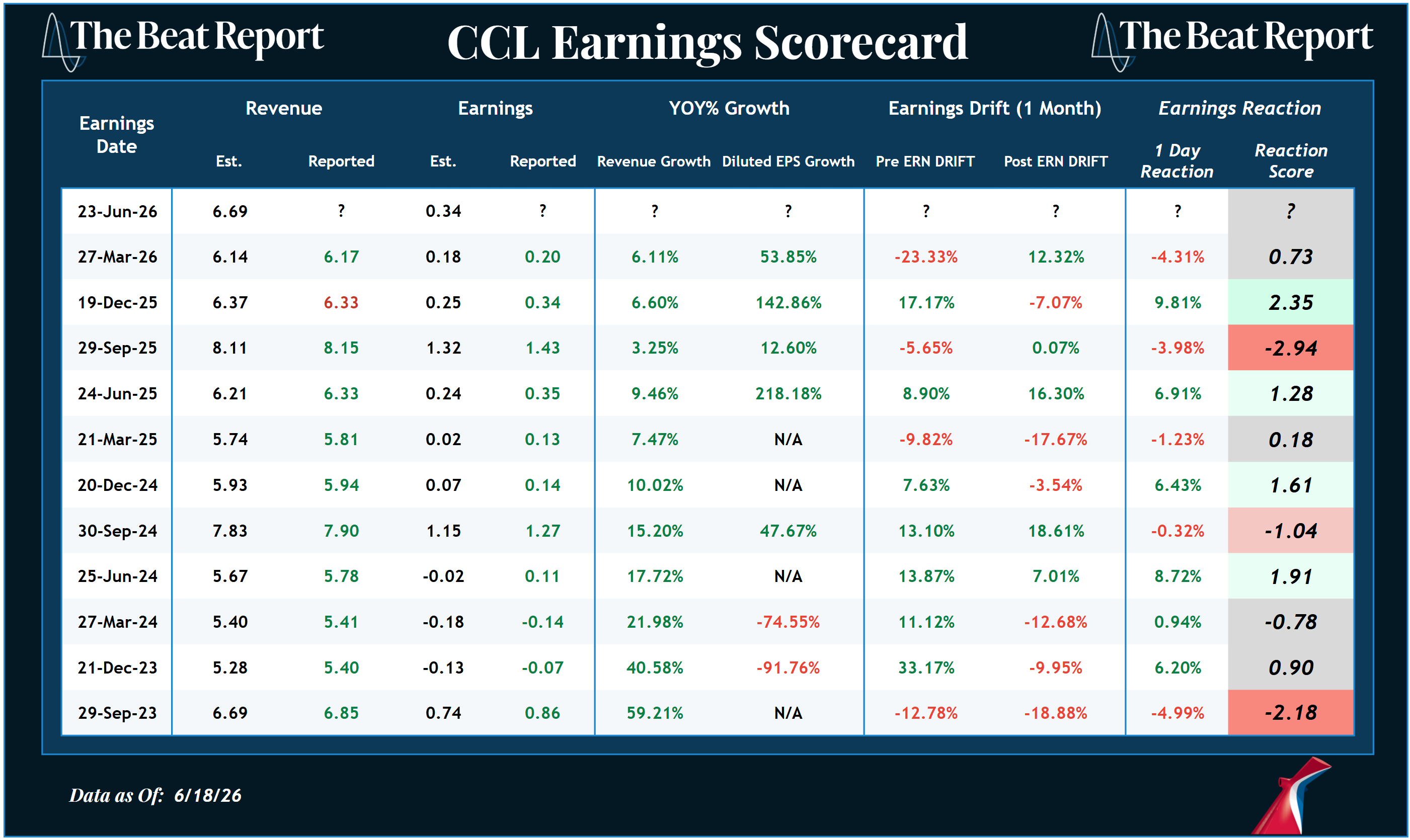

Next up is Carnival, which reports Tuesday before the open, and the consensus is for the company to report $6.69 billion in revenue and $0.34 in earnings per share.

Carnival is one of the more compelling base-on-base structures in the entire consumer discretionary space.

And each breakout attempt has failed at $31.50.

This marks the prior cycle peak, and the supply continues to outstrip demand at this level.

However, Carnival has been coiling beneath it, absorbing overhead supply, and building pressure for what could become a major breakout.

If buyers can finally push CCL through $31.50 and hold it, we believe the reaction leg higher will likely be epic.

The earnings scorecard gives us reasons to care about this setup ahead of this week's report, but not enough conviction to jump the entry.

Earnings growth has been massive over the past several quarters, revenue growth remains positive, and demand for cruising continues to look strong.

Last quarter, Carnival delivered record first-quarter revenue, net yields, operating income, EBITDA, and customer deposits.

Bookings for 2026 were up double digits, and nearly 85% of the year was already on the books.

The problem is earnings sentiment...

Carnival’s earnings reactions have been inconsistent. One quarter the stock gets rewarded, the next quarter it gets punished. Over and over again.

That is not the kind of persistent earnings sentiment we see in the best stocks.

But that doesn't invalidate the technical setup...

The stage is set for a gap-and-go above $31.50 if Carnival delivers a strong report and the market finally rewards it with conviction.

If that happens, this base-on-base structure would be resolved, putting CCL back on the leadership radar.

But if the stock fails again at $31.50, then the stock likely needs another quarter to absorb overhead supply.

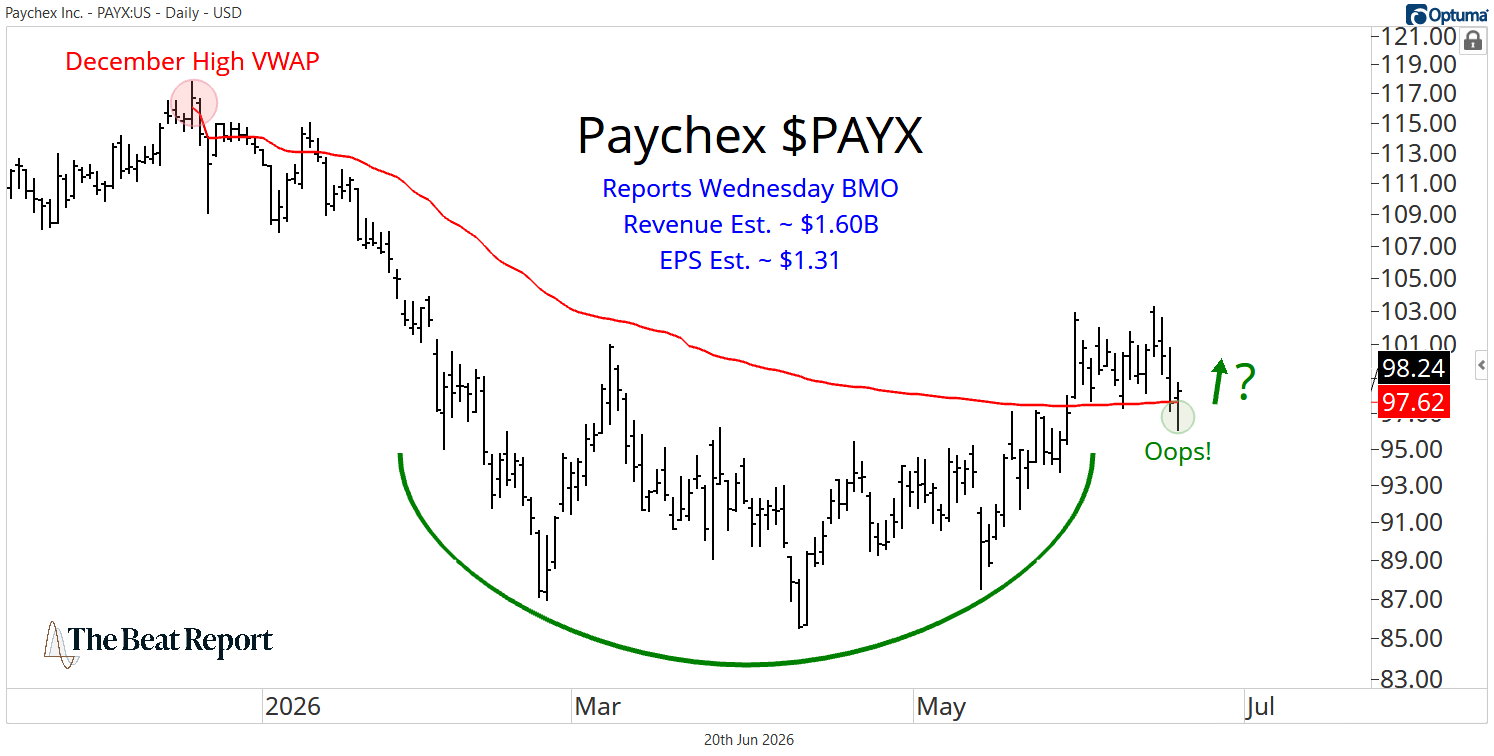

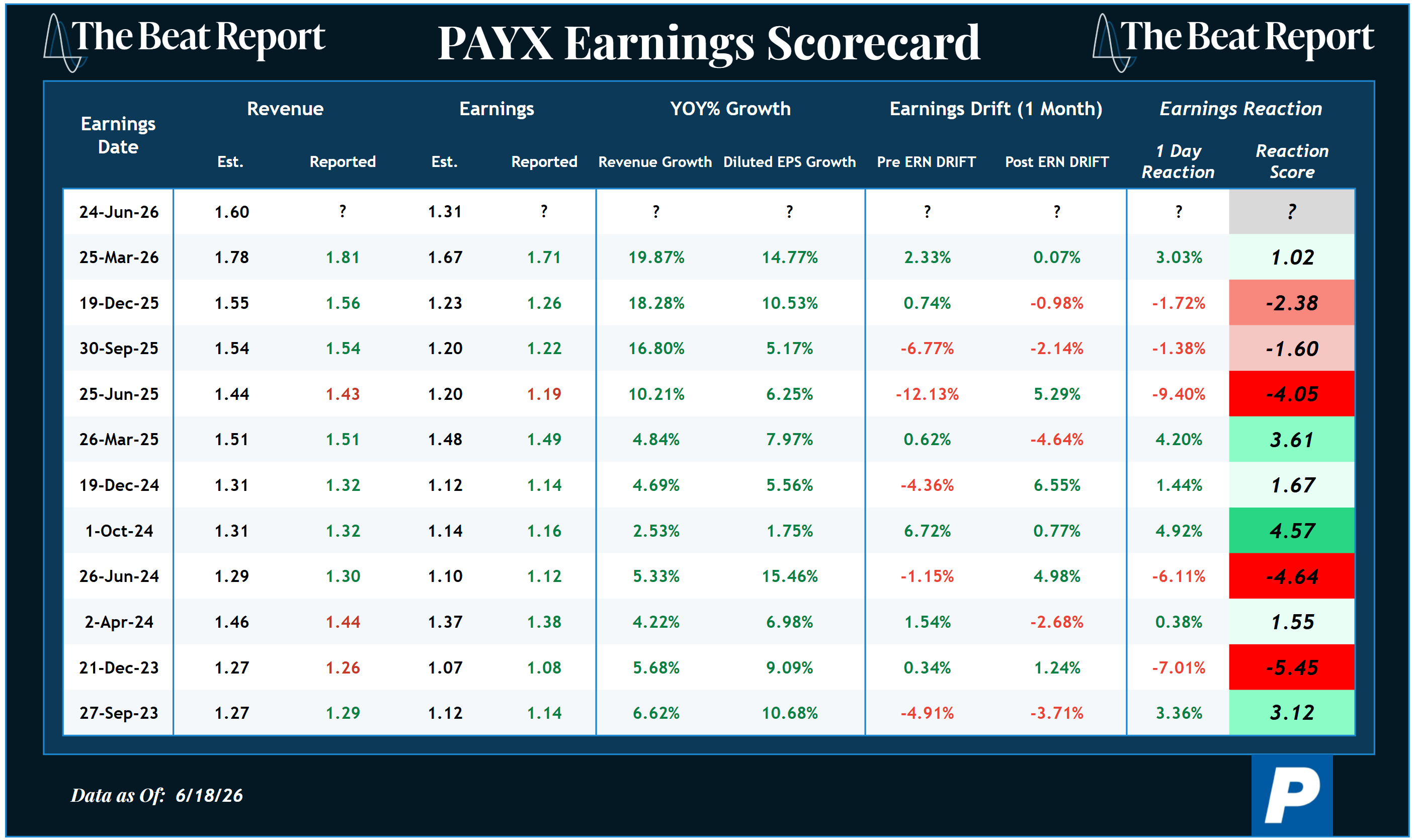

Finally, we have Paychex, which reports Wednesday before the open, and the market is looking for $1.60 billion in revenue and $1.31 in earnings per share.

Paychex is another repair story, but it is very different from Carnival.

This is a human capital management company that provides payroll, HR, benefits, insurance, and compliance solutions to small and mid-sized businesses.

In plain English, Paychex helps businesses pay their workers, manage their people, stay compliant, and handle the HR work small companies usually don't want to do themselves.

That may not sound exciting, but it's a very sticky business model.

And after a tough stretch, the stock is starting to act better.

PAYX has carved out a textbook bearish-to-bullish reversal pattern over the past several months.

Then the stock broke above the VWAP anchored to its December high a few weeks ago, and then it laid a bear trap on Thursday.

Now it needs upside follow-through.

Right now, the earnings scorecard is supportive of the technicals.

Revenue growth and earnings growth are both hitting multi-year highs, and last quarter the stock snapped a streak of three consecutive negative earnings reactions.

And that matters because Paychex has been trapped in the broader “SaaSpocalypse” and software slowdown narrative.

Investors have been quick to punish anything tied to payroll, HR software, or white-collar employment trends.

But the company isn't acting broken.

Last quarter, Paychex delivered 20% YoY revenue growth and 15% YoY adjusted EPS growth.

Management also highlighted progress in integrating Paycor, accelerating AI initiatives, growing advisory and benefits solutions, and serving roughly 800,000 clients across HR, benefits, payroll, and compliance.

The AI angle here is not some gimmick either.

Paychex says it now has more than 500 AI-powered capabilities and agents across its platform, helping clients navigate employment law, benefits selection, payroll processing, service workflows, and sales support.

The market has spent a long time treating these kinds of software names as if AI would destroy them.

But in Paychex’s case, AI may actually strengthen its moat by making its compliance expertise, payroll data, and advisory relationships more scalable.

So this week is an important test...

If Paychex delivers another solid report and the stock climbs higher, the reversal pattern will be complete.

But if PAYX fails to rally, the stock will probably churn sideways for longer.

We just held our first-ever Beat Report Pitch Meeting.

We've always held these meetings internally, but this was the first time we pulled back the curtain and let the public sit in on one.

This is the time when our Beat Report analysts have a chance to present their highest-conviction trade ideas and debate them in real time with Steve Strazza and the rest of the team.

And it turned into something much bigger than we expected...

The discussion ran for nearly two and a half hours, much longer than anything we’ve ever done here at Stock Market Media.

Editor's Note: With the IPO window wide open and money rotating through every corner of this market, Steve Strazza thinks we're heading into one of the more favorable stretches of the cycle for aggressive traders.

He made the full case in a FREE training this week. He walked through the setups he's watching, how he handles risk, and why he's leaning in now.