Inflation’s Rebellion: No Room for Summer Soldiers

The Summer Soldier and the Inflation Setup

By Jason Perz

November 15, 2025

“These are the times that try men’s souls. The summer soldier and the sunshine patriot will, in this crisis, shrink from the service of their country…” — Thomas Paine, 1776

It’s one of my favorite lines in all of literature — and one of the best metaphors for trading. Because right now, we’re surrounded by summer soldiers.

Oil drops 4% and suddenly “the inflation trade is dead.” Same crowd that was calling for $150 crude six months ago now can’t stomach a pullback.

But here’s the thing: the structure hasn’t changed.

Inflation Is Setting Up for Another Leg Higher

Let’s step back and look at what’s actually happening.

The Fed is still cutting rates. Odds are building for one more cut in December. Fiscal authorities are talking about $2,000 stimulus checks. Trump has floated a 50-year mortgage, which would inject liquidity and keep home prices artificially high.

And now, policymakers are quietly shifting the goalposts on inflation.

Kevin Hassett from the White House said he’s comfortable with 3%. The Fed says 3% “for the short term” is fine. Even Trump brushed off affordability as a “con job.”

Translation: they’re telling you they don’t mind higher inflation.

When the people in charge start normalizing 3% inflation targets, cut rates, and send out checks — it’s not a deflationary playbook. It’s a reflationary one.

If they’re trying to make inflation move higher… they’re going to get it.

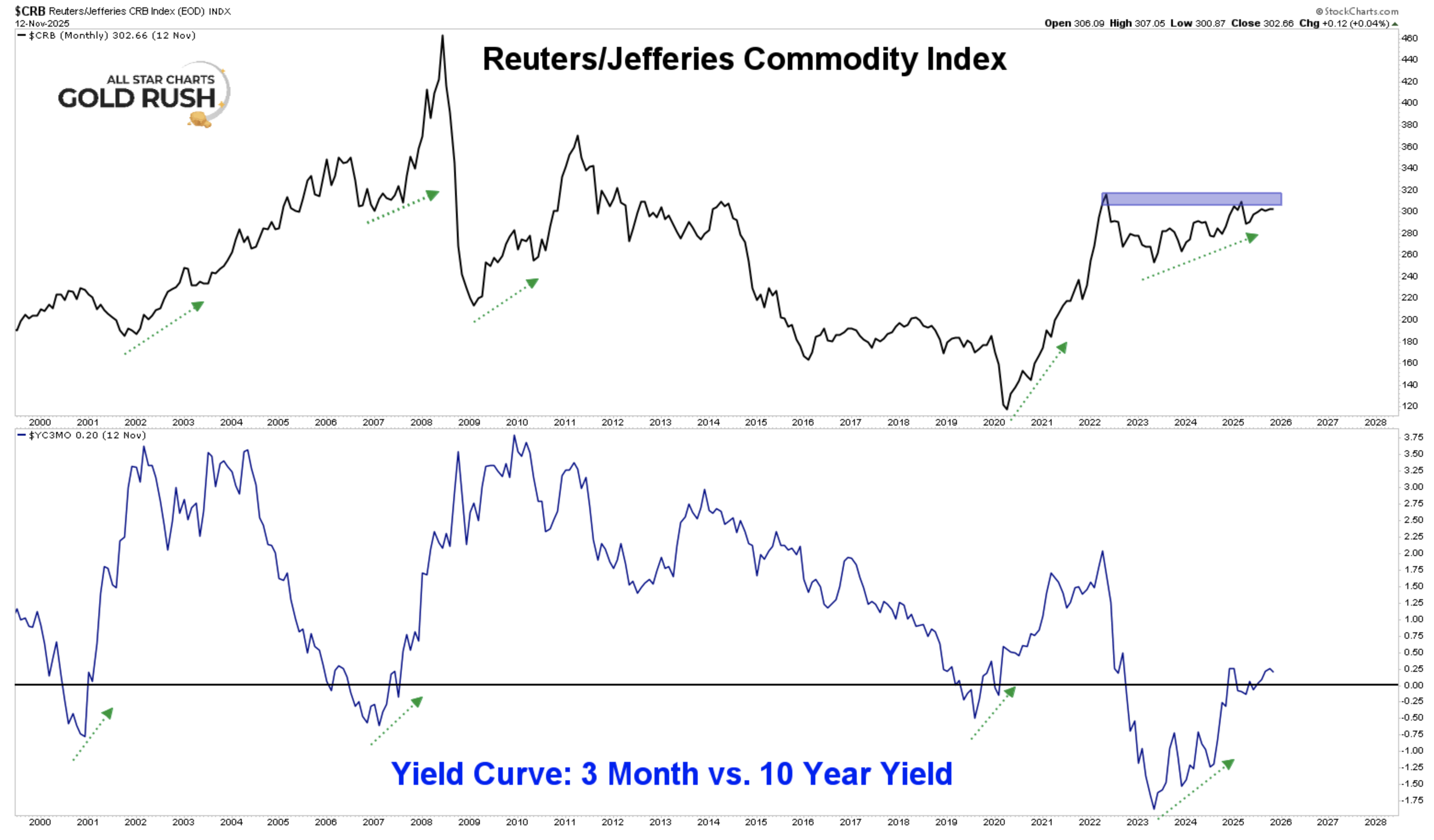

The Yield Curve Knows What’s Coming

Now, look at the chart below.

The top panel is the Reuters/Jefferies CRB Index — a broad measure of global commodities. The bottom panel is the yield curve — the spread between the 3-month and 10-year Treasury yields.

Notice something? Every time the yield curve bottoms and starts to steepen (green arrows), the CRB Index follows with a surge in commodities.

The curve has flipped from inversion to bull steepening, meaning short-term rates are falling faster than long-term rates. That’s what happens when central banks cut aggressively and liquidity floods the system.

This setup doesn’t kill inflation. It feeds it.

The Fed Can Cut, But It Can’t Control the Long End

The Fed can influence short-term rates, but the long end of the curve — 10-year yields — is controlled by global capital flows, not Jerome Powell.

When the short end falls and the long end holds firm, you get a bull steepener — the exact regime we’re in now.

It’s not bearish. It’s transitional.

That steepening supports risk assets like equities and commodities. It creates liquidity waves that lift everything until the cycle matures into a bear flattener — when long yields fall back below short yields as growth cools.

We’re not there yet.

Energy Is the Patience Trade

Now, let’s talk about energy — the market everyone loves to hate.

Oil dropped 4% the other day and the crowd panicked. “Energy’s done.” “Cycle’s over.” Same story, different day.

But the market structure says otherwise.

We’re still seeing tight supply, steady demand, and a global policy stance that’s inflationary by design. Energy stocks (XLE) just need to clear the key levels — 97 and 101 — to confirm the next move.

Until then, it’s a game of patience.

Energy is like that one friend who’s always late to the party — messy, stubborn, but when they finally show up, they’re the life of the room.

The fundamentals haven’t changed. The chart structure hasn’t changed. Only sentiment has. And sentiment always flips right before the move happens.

The Lesson: Don’t Be the Summer Soldier

Trading is about endurance, not emotion.

You can’t get shaken out every time a sector pulls back. You can’t declare the end of a cycle every time a chart dips. You’ve got to zoom out — read the structure, follow the liquidity, and stay patient through the noise.

Thomas Paine wasn’t writing about markets when he said “the harder the conflict, the more glorious the triumph,” but it fits perfectly.

This is one of those moments. Inflation is being invited back in. The yield curve is confirming it. Commodities are tightening up, and the next wave is forming quietly under the surface.

So stay disciplined. Stay focused. Don’t be the summer soldier.

You need to have a subscription to access this content in full.

Log in or subscribe today to unlock new features and receive Member Benefits.