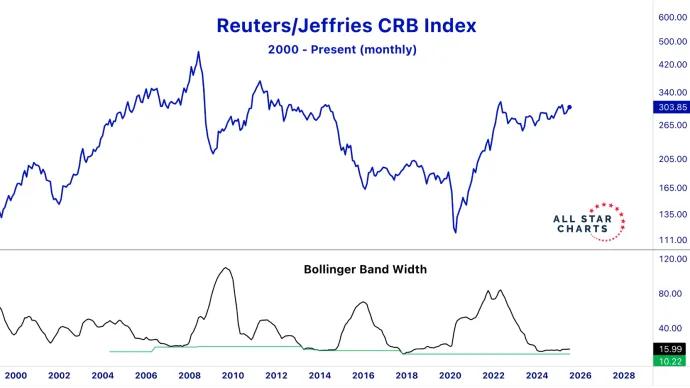

The yield curve warned us. CRB compressed. XLE broke out.

For months, the yield curve has been doing what it always does before big commodity and energy moves: it started whispering before price started screaming.

This wasn’t a headline trade.This wasn’t a CPI print trade.This was a...

As we head into the weekly close, crude oil is sitting uncomfortably close to a 52-week closing low. If it finishes the week here, that’s not a bullish headline. That’s pressure.

“Ending is better than mending.” — Aldous Huxley, Brave New World

Huxley wasn’t talking about the Federal Reserve, but he may as well have been.We’ve entered a market regime where policymakers would rather pump, patch,...

“These are the times that try men’s souls. The summer soldier and the sunshine patriot will, in this crisis, shrink from the service of their country…”— Thomas Paine, 1776

It’s one of my favorite lines in all of literature — and one of...

In most parts of life, the rule is simple — follow the leader.But in the bond market, the game’s a little different. Here, it’s more like carry the follower.

That’s exactly what we’re seeing play out right now between short term and...

There’s no drama about what the Fed is expected to do this week—rates are staying put. Markets are pricing it in, 105 out of 105 economists in the Reuters survey agree, and Powell hasn’t given us any reason to expect otherwise. The drama is...

Everyone keeps assuming the Fed is done. That rates peaked in 2023. That the next move is down. That the cycle has run its course and we’re heading back to easy money.