As we head into the weekly close, crude oil is sitting uncomfortably close to a 52-week closing low. If it finishes the week here, that’s not a bullish headline. That’s pressure.

At the same time, the 30-year U.S. Treasury yield is doing the opposite. It’s consolidating near the highs and quietly pressing upward. No panic. No collapse. Just steady, persistent firmness.

That creates a divergence, and divergences matter.

Historically, oil and long-end yields don’t live in completely different worlds. They’re both inflation-sensitive, growth-aware instruments. When they separate like this, it’s usually temporary. One of them eventually catches up to the other.

The problem — and the opportunity — is that we don’t get to know which one first.

This is a mixed signal, not a trade signal. And that distinction matters.

Right now, oil is weak. Yields are firm. I’m not here to argue with either.

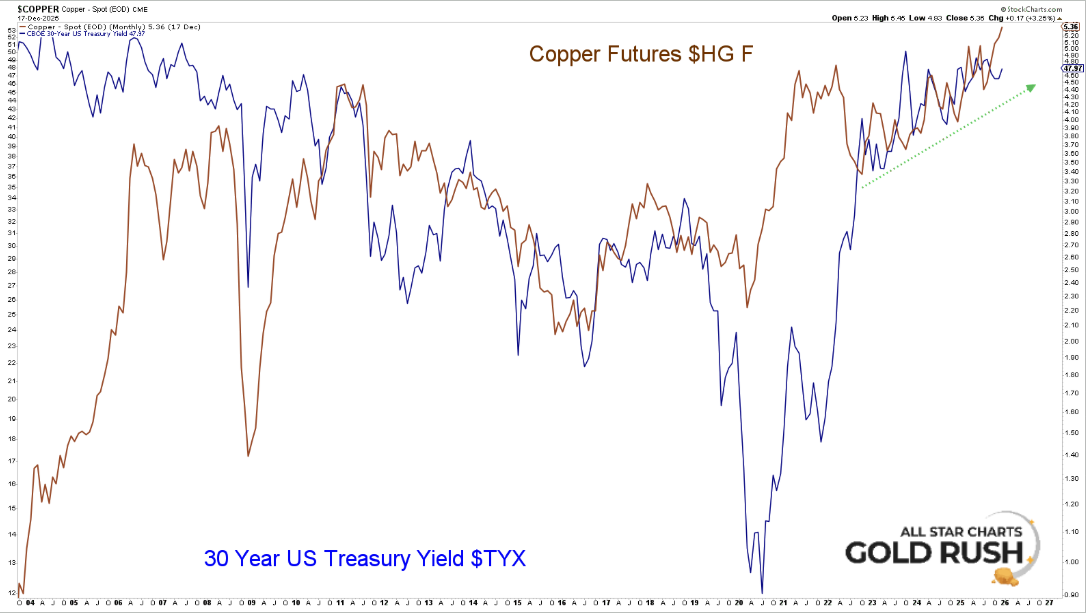

I Don’t Know the Future — But Copper Might

If oil is the question mark, copper is the exclamation point.

Copper could log all-time closing highs this week. Not intraday noise. Not a wick. A close. That matters.

And what makes this even more interesting is that copper and long-end yields are still connected. They’re moving together, reinforcing the same message: global demand isn’t rolling over, and rates are not signaling some imminent deflationary collapse.

We’ve said this before, and it’s worth repeating: bond yields look like they want to go higher.

That view isn’t just U.S.-centric either.

German yields are breaking to new highs. Japanese yields are making all-time highs.

This is not a one-country story. This is a global rates story — and copper is validating it.

“The tape tells the truth, even when the news lies.” — Jesse Livermore

Copper is telling a story of strength, expansion, and continued pressure on the cost of capital.

Where That Leaves Oil

Here’s the uncomfortable part.

Oil is not a buy right now. Not yet.

As long as crude remains well below its 52-week high at 77.48, I have zero interest in forcing a long. Weak price is weak price. I don’t care about narratives. I don’t even care what I think. I care about levels.

That said — and this is important — if oil is ever going to bottom, now is the window.

We’re entering oil’s seasonal strength period. Historically, this begins around now and strengthens materially into February–April. That doesn’t mean it has to work. It means the backdrop is becoming more favorable.

So my posture here is simple and explicit:

I’m not long

I’m not short yet, unless we get a decisive weekly close below 57.13

I’m watching closely

If oil holds this zone, stabilizes, and eventually reclaims 77.48 next year, I want to be long.

If it closes below 57.13 in the front-month contract decisively, I’ll respect that and go short.

This isn’t about conviction. It’s about confirmation.

Flexibility Is the Edge

I don’t trade with a crystal ball. I trade with conditional logic.

Copper is strong. Yields are firm. Oil is weak — but sitting at a level where outcomes widen.

That tells me one thing: stay flexible.

Over the next few months, my bias is clear. I’d rather be looking for longs than pressing shorts, if oil can hold together here. But it has to prove it. I’m not front-running anything.

“The goal is not to predict the market. The goal is to read it.” — Paul Tudor Jones

Right now, the market is speaking in mixed signals. And when that happens, the smartest move is patience — not bravado.