By the Time You See Inflation, It’s Already Too Late

The Big Picture — Because Inflation Doesn’t Start in the Grocery Aisle

By Jason Perz

January 6, 2026

Inflation never starts where people think it does.

It doesn’t start at the checkout line. It doesn’t start with sticker shock. It starts quietly, in currencies and rates.

That’s where we are right now.

The U.S. dollar is rolling over into a weak-dollar regime, and the yield curve is steepening. Historically, that combination has been one of the cleanest early signals for future inflation pressure — not headline CPI blowing out tomorrow morning, but structural inflation building beneath the surface.

This is why we keep repeating the same message, even when it’s uncomfortable:

We are in a sticky inflationary environment — not yet a headline inflation environment.

And that distinction matters more than most people realize.

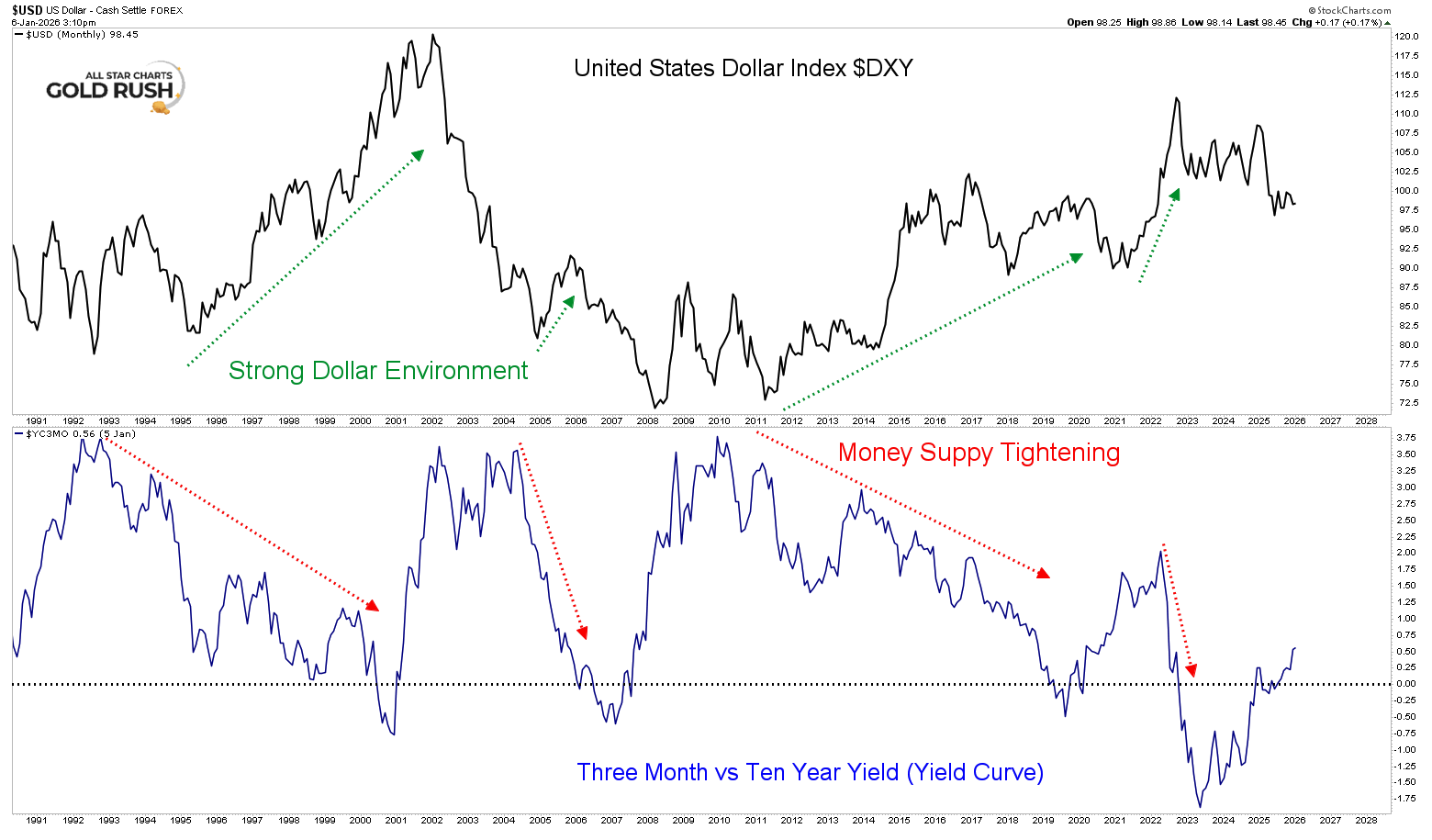

One Chart That Explains the Regime Shift

This single chart tells you almost everything you need to know about where we are in the cycle.

Every major inflationary and commodity-driven regime of the last 40+ years shares the same fingerprint: a weakening U.S. dollar paired with a steepening yield curve.

That’s not theory. That’s history.

On the top panel, you can see long stretches of dollar strength. Those periods consistently line up with tightening financial conditions, restricted liquidity, and commodity underperformance. When the dollar is strong, capital hides. Growth slows. Real assets stall.

But when the dollar rolls over and begins to trend lower, the regime flips.

Currencies set the price of everything. When the reserve currency weakens, hard assets don’t need a surge in demand to move higher — they simply reprice because the measuring stick is shrinking. Inflation doesn’t explode all at once. It seeps.

Now look at the bottom panel.

The 3-month vs. 10-year yield curve tells the same story from a different angle. For years, the curve was inverted — tight money, restrictive policy, deflation fears. That phase is ending.

As the curve steepens:

Liquidity conditions improve

Credit creation restarts

Capital moves out the risk curve

Real assets begin to outperform financial assets

Historically, this turn in the yield curve leads commodity cycles. It always has. Markets move first. The data follows later.

This is why waiting for CPI confirmation is how investors get blindsided.

Inflation doesn’t start in the grocery aisle.

It starts here — in currencies and rates.

And right now, both are telling you the same thing:

The regime is changing.

Why CPI Doesn’t See What’s Coming

This is the part almost nobody explains honestly.

The inflation indexes are not weighted toward the commodities that actually sit at the foundation of the modern economy.

Let’s be explicit:

Gold & Silver Monetary metals. Not meaningfully weighted.

Copper Used in power grids, AI infrastructure, EVs, electronics, housing. Not directly weighted.

Aluminum & Steel Core industrial inputs. Not directly weighted.

The only major commodity that shows up directly and meaningfully?

Gasoline.

That’s it.

So when copper, steel, and aluminum surge — CPI barely moves. Those costs don’t vanish. They simply take time to filter through cars, appliances, electronics, housing materials, and capital equipment.

Inflation doesn’t hit instantly.

It moves through the system in waves.

And When Something Shows Up Too Loudly… They Remove It

If a commodity starts influencing CPI too much, it doesn’t get debated.

It gets reweighted away.

Coffee is the most recent example. After a major price spike, its weighting was reduced so aggressively that it barely registers in CPI anymore. Other commodities have quietly disappeared entirely over the decades.

This isn’t accidental. It’s how inflation stays “contained” on paper.

Which is exactly why people who watch indexes instead of price get blindsided every cycle.

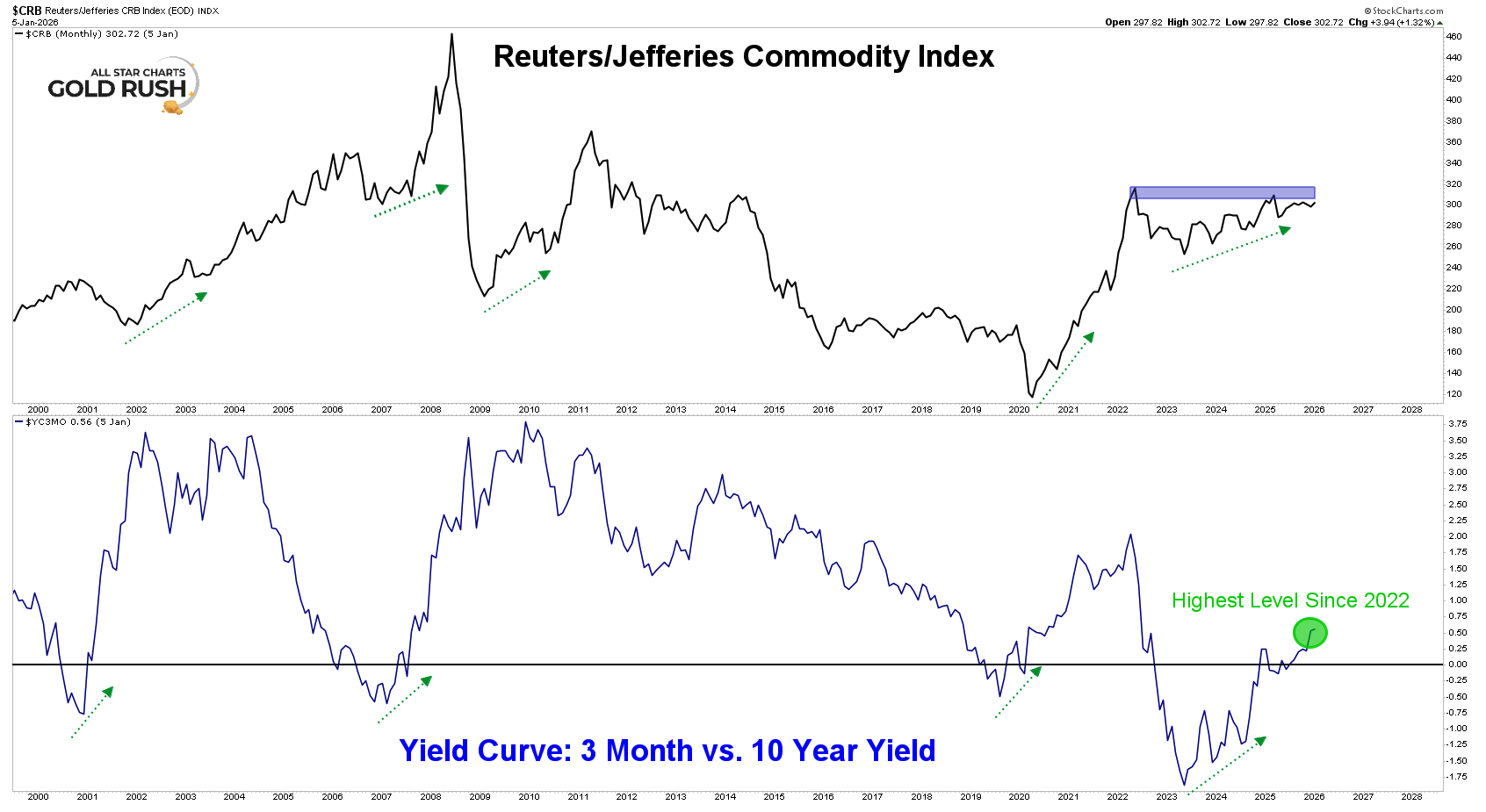

CRB + Yield Curve = The Commodity Signal

Now look at the CRB Index chart alongside the yield curve.

The CRB is heavily energy-weighted. That matters.

Historically:

When the yield curve bottoms and turns higher

And the dollar weakens

The CRB follows — not immediately, but decisively

Right now, the CRB is consolidating just below major resistance, while the yield curve has already turned up to its highest level since 2022.

That setup doesn’t scream “deflation.”

It whispers “next leg higher.”

Energy is the missing piece — and that’s exactly what could wake up.

Why This Matters Before CPI Moves

People always ask the same question:

“If inflation is coming, why don’t we see it yet?”

Because inflation is a process, not an event.

It starts in currencies

Then rates

Then commodities

Then producers

Then finished goods

Then consumers

By the time CPI reflects it, the opportunity is gone.

Markets don’t wait for permission from economic releases.

They move ahead of them.

The Takeaway

A weak dollar.

A steepening yield curve.

A surging metals and mining complex.

A commodity index pressing higher.

Energy quietly positioning to follow.

This is how inflationary cycles begin — not loudly, but structurally.

Headline inflation will get the attention later.

Positioning happens now.

The grocery aisle is the last place inflation shows up.