I think Powell sees exactly what the market is showing anyone willing to look past CPI headlines: inflation is bubbling under the surface. It hasn’t re-accelerated in the statistics yet—but inflation never announces itself there first. It shows up in prices before it shows up in prints.

And prices are already talking.

We’re coming off the 2020–2022 inflation shock, and here’s the part most people conveniently forget: we never went back to pre-COVID price levels. We stabilized on top of them. That matters. When price levels reset higher and stay there, inflation doesn’t disappear—it becomes sticky. It embeds itself into wages, supply chains, capital spending, and expectations.

That’s the environment we’re in now.

Sticky Inflation Isn’t Loud — It’s Persistent

If you stare at CPI alone, you can convince yourself inflation is “contained.” CPI is backward-looking, politically sensitive, and poorly weighted toward the things that actually drive future costs.

But when you zoom out and look at the raw inputs—the materials that sit at the base of the global economy—a different story emerges.

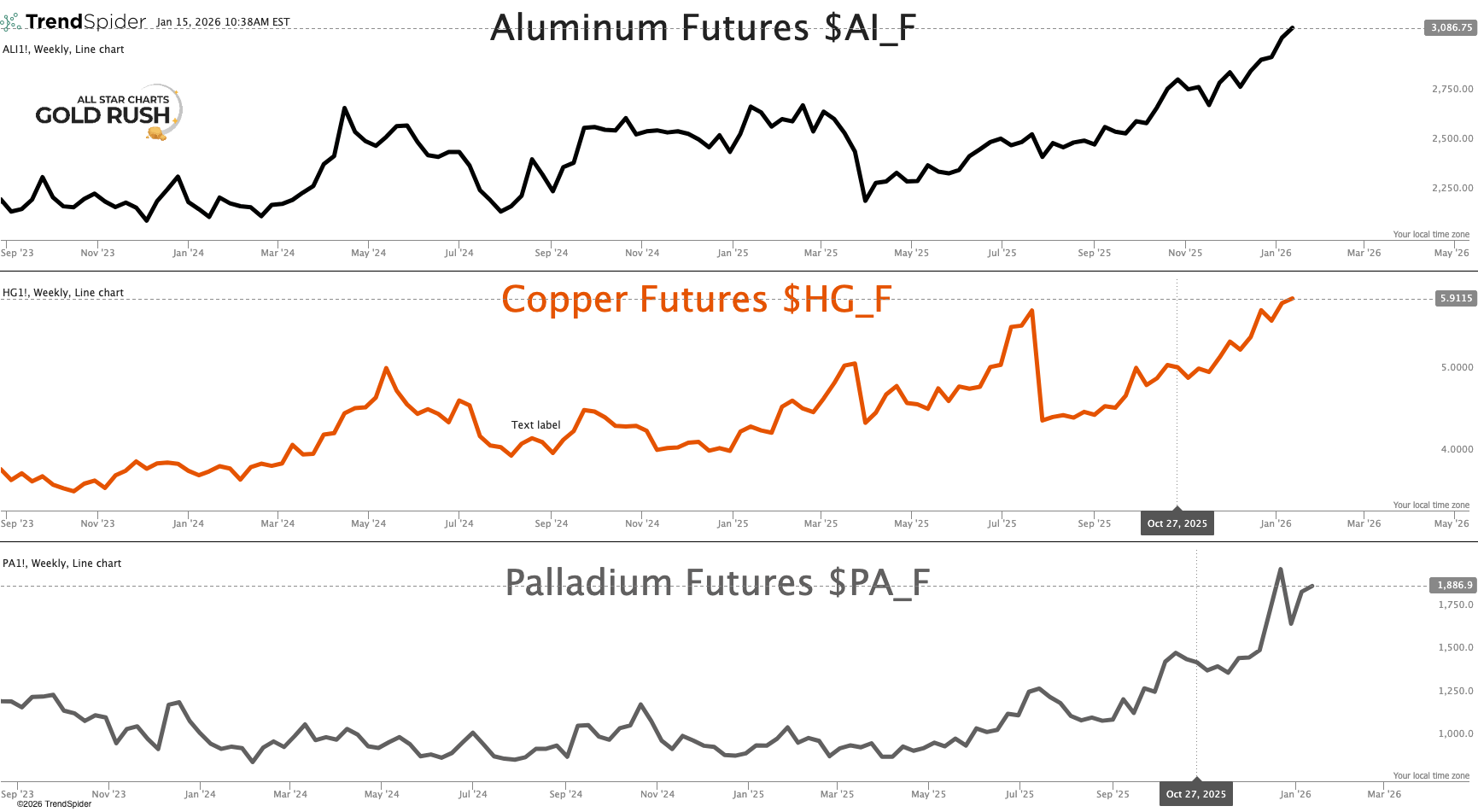

Aluminum is breaking higher.

Copper is pushing toward new cycle highs.

Palladium has come alive after years of dormancy.

Nickel, zinc, tin—all moving.

These aren’t speculative meme trades. These are industrial metals. They move when capital spending rises, when infrastructure demand accelerates, and when supply is tighter than people realize.

Markets don’t wait for CPI confirmation.

They front-run it.

The Metals Message Isn’t Random

Aluminum futures are in a sustained uptrend, grinding higher after digesting gains. Copper has resumed leadership after consolidation, behaving like a metal that knows it’s structurally scarce. Palladium—written off, ignored, hated—is waking up the way beaten-down commodities do right before they matter again.

This isn’t confined to futures. Metals and mining equities are confirming the move. Leadership is expanding. Breadth is improving. Capital is rotating toward real assets.

That doesn’t happen in a disinflationary regime.

It happens when money is leaking out of currency and into things you can’t print.

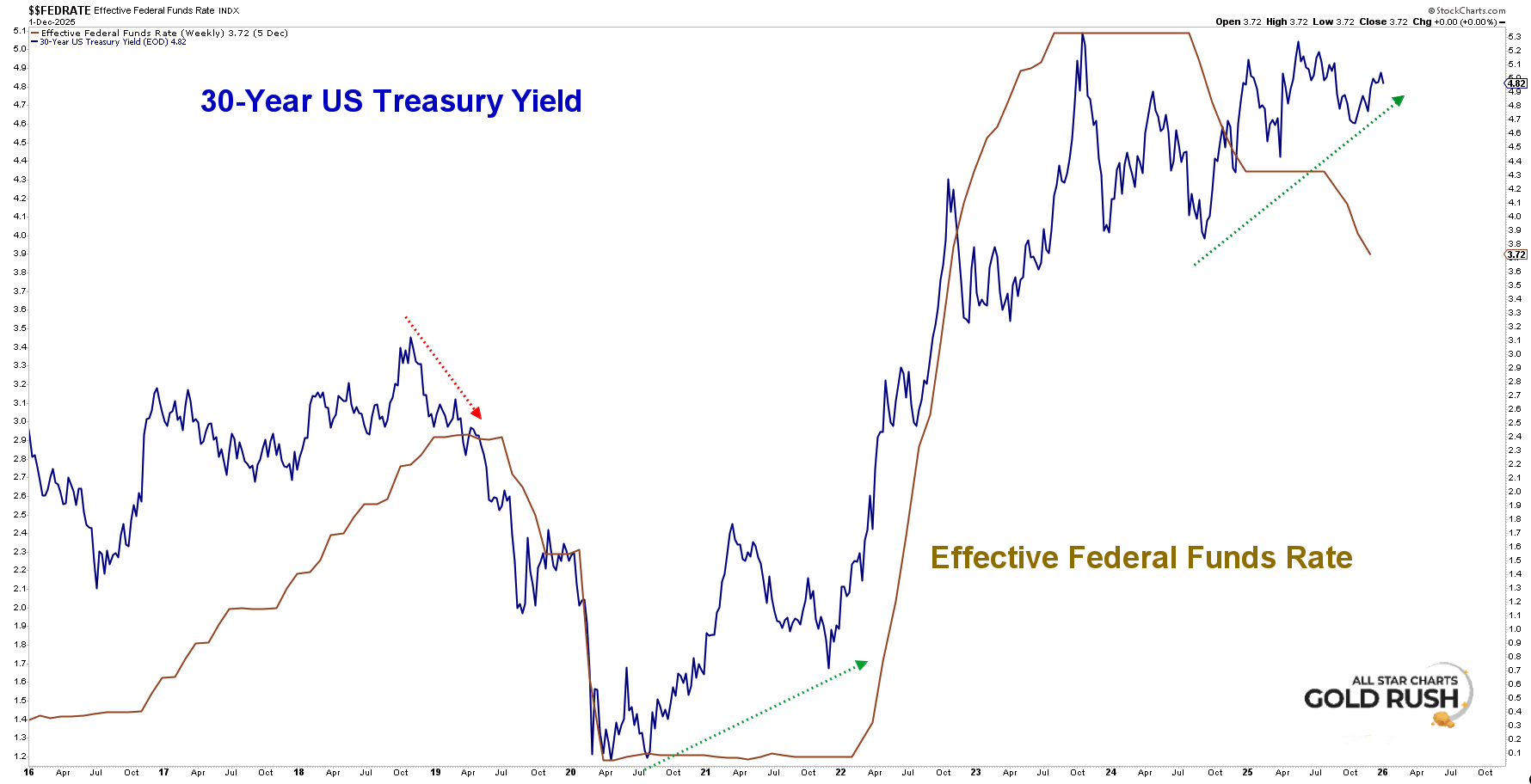

Now Look at Rates — This Is the Tell

The effective fed funds rate is being pushed lower, while the 30-year Treasury yield continues to move higher.

That divergence matters.

Short rates are policy.

Long rates are markets.

When long-term yields rise despite easing pressure at the front end, the bond market is sending an uncomfortable message: inflation risk isn’t gone.

Growth expectations, term premiums, and supply dynamics are pushing yields higher even as the Fed faces pressure to cut.

That’s not a victory lap for disinflation.

That’s a warning sign.

Historically, easing into rising long rates doesn’t end cleanly. It leads to financial repression, currency pressure, and higher real-asset prices.

Powell knows this.

Why Powell Spoke — And Why It Matters

Powell’s recent weekend statement matters—not because of the politics, but because of the timing. He framed the DOJ probe as an attempt to intimidate the Fed into cutting more aggressively and emphasized that policy will be set by evidence, not pressure.

I’m not here to glaze Powell. But I am here to recognize competence.

Powell understands that cutting aggressively into rising long-end yields and firming commodity prices is how inflation re-ignites—not how it dies. He also understands CPI is a lagging indicator, and by the time it turns, pretending you didn’t see it coming doesn’t work.

The Bottom Line

Inflation doesn’t explode. It accumulates.

Quietly. Persistently.

If inflation were dead, metals wouldn’t be leading.

If growth were collapsing, copper wouldn’t act like this.

If policy were truly restrictive, long bonds wouldn’t be selling off.

Markets are voting with capital, not commentary.

Inflation doesn’t start at the grocery store.

It starts in currencies, rates, and commodities.

Powell knows it.

The bond market knows it.

The metals market knows it.

By the time investors understand it, it is already too late.