For forty years, bond yields trended lower. From the early 1980s until 2020, the 10-year Treasury yield fell through every cycle.

Each downturn, each policy mistake, was met with the same cure: cut rates, buy bonds, suppress yields.

That cycle ended with the pandemic.

In 2020, unlimited QE, fiscal expansion, and sticky inflation broke the trend.

Yields stopped falling and began moving higher. That change - an end to a 40-year bond bull market - is the foundation for the setup we face today.

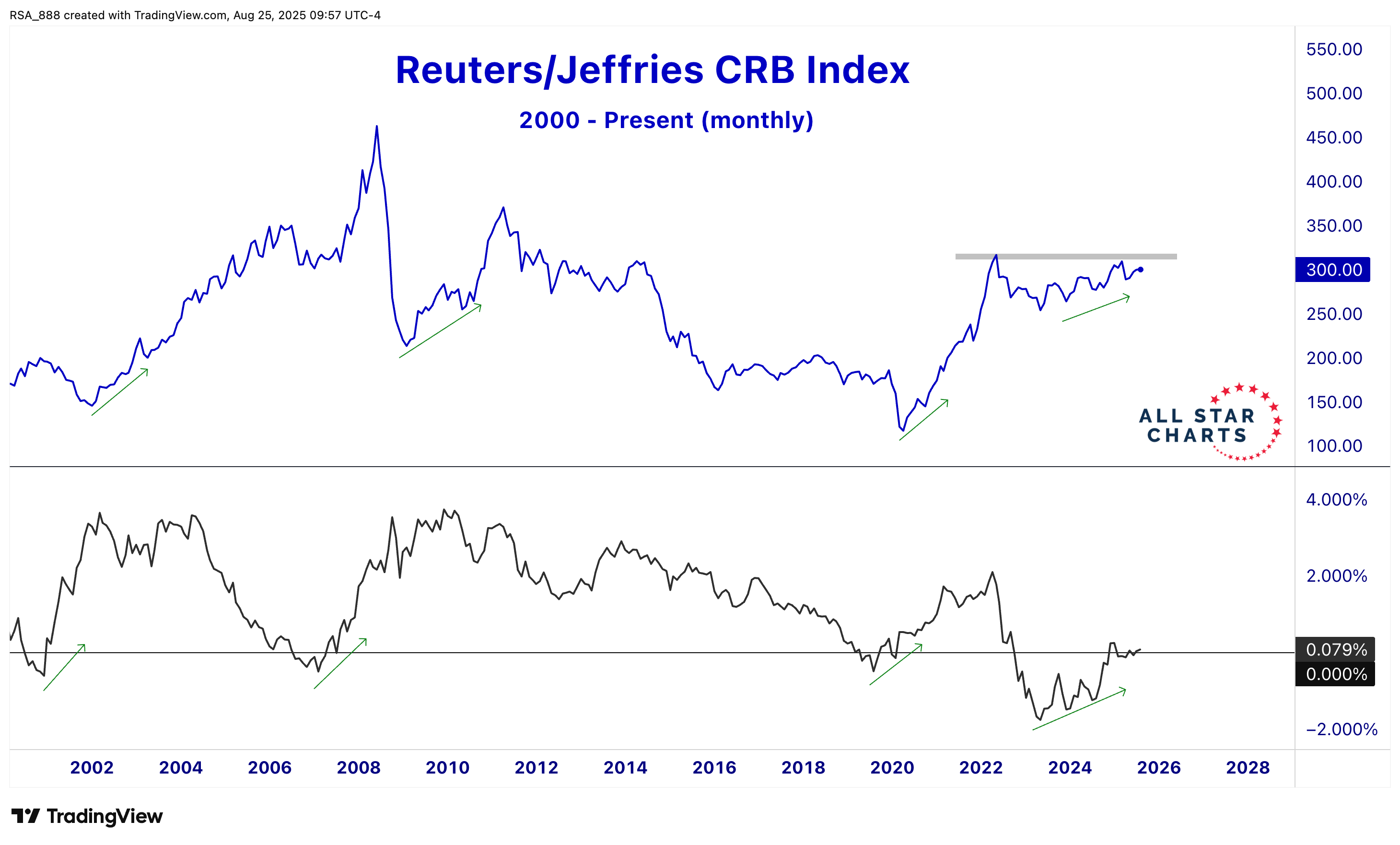

Yield Curve vs. Commodities

📊 Yield Curve Steepening = Commodities Surges

Every major steepening of the yield curve has aligned with a melt-up in the prices of commodities.

The pattern is clear in the Reuters/Jefferies CRB Index:

Early 2000s reflation

Post-2008 recovery

Post-2020 reopening

Each cycle saw the same structure - Fed cuts at the short end, liquidity expansion, and flows into real assets.

Energy, metals, and cyclicals led the charge each time.

Now that Powell has signaled that rate cuts are back on the table, the market is reacting accordingly.

The yield curve has already turned up. If the Fed follows through, history suggests another commodity surge is close.

This time, the CRB Index matters even more because it is so energy-heavy. If liquidity enters an already tight energy market, the reaction could be sharp.

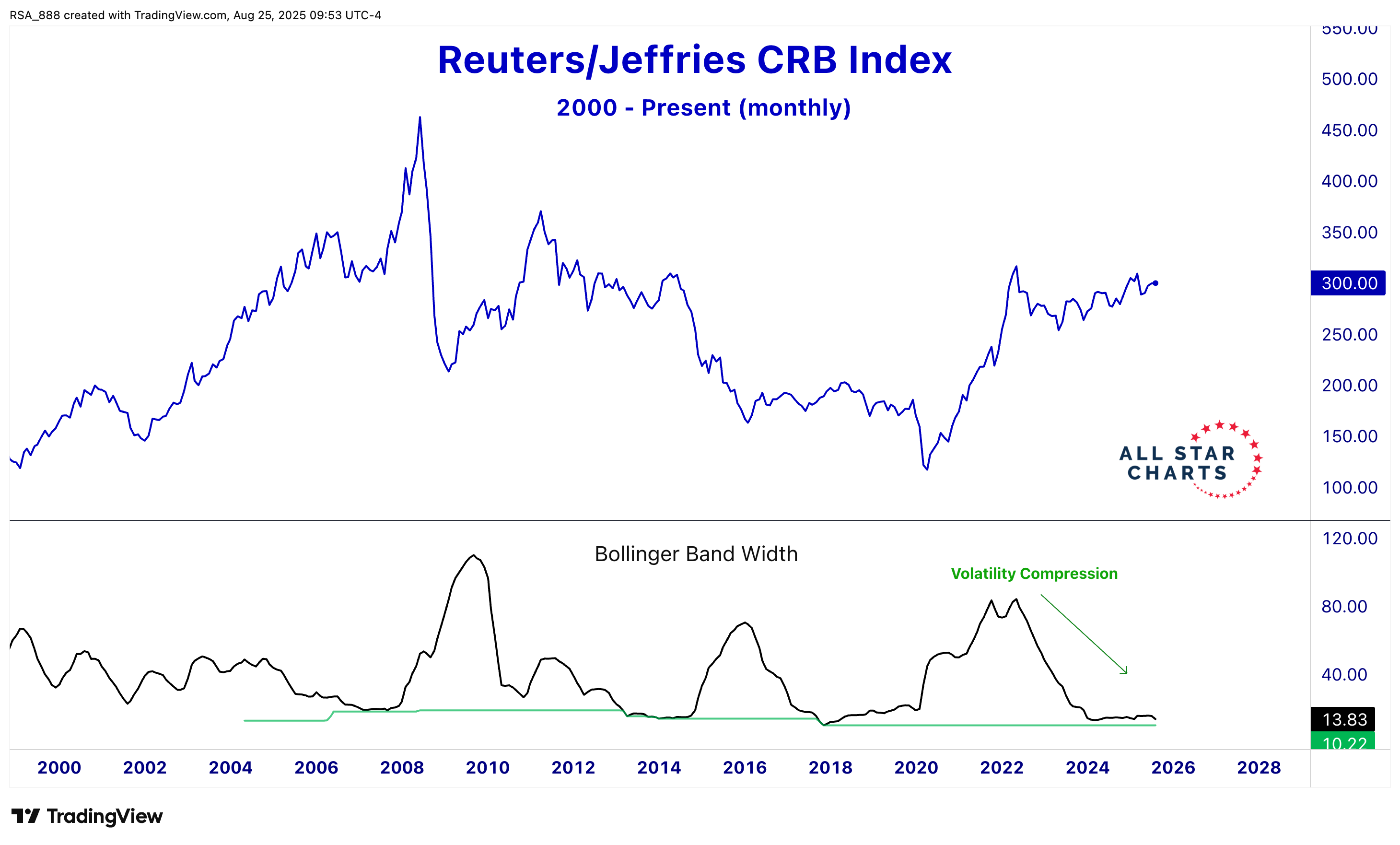

The Bollinger Band Squeeze

📊 CRB Compression at Historic Lows

The CRB Index sits in one of the tightest Bollinger Band squeezes in decades. Volatility in commodities has collapsed to levels that rarely hold for long.

Past examples show what happens next:

2007–08: CRB doubled in less than two years.

2020–21: Commodities nearly tripled off the pandemic lows.

These were not slow moves... They were vertical accelerations.

The same conditions are present now - low volatility, compressed price action, and a macro trigger.

We think that the macro trigger will likely be the Fed.

From Bonds to Commodities

The market can no longer assume that cuts equal disinflation. In an environment of sticky inflation, rate cuts mean reflation.

Long-term yields are no longer capped. They have broken the 40-year downtrend.

Policies since 2020-QE, including stimulus during deficits, and now cuts despite sticky prices, continue to fuel higher yields.

That shift forces investors into real assets. Precious metals, industrials, materials, and cyclicals thrive in this environment.

What to Watch

Yield Curve: Steepening is the oxygen for commodities.

CRB Bollinger Band Squeeze: Low volatility signals a sharp resolution.

Energy: Because the CRB is energy-driven, oil and gas may lead. Metals and miners will likely follow.

Final Word

The bond bull market ended in 2020. The new regime is reflation. The Fed’s next move - cutting rates - adds fuel to this structure.

With the yield curve turning higher and the CRB trapped in a historic squeeze, commodities are primed for a breakout.

When the move begins, it will not be orderly. It will be fast, broad, and led by higher long-duration yields.

Keep this setup on your radar.

P.S. Tomorrow at 1 p.m. ET, Jeff Macke and JC go LIVE.

Catch their take on the latest earnings, potential M&A targets, and the Macke 30 Index before anyone else.