Everything you need to know about price action, regardless of asset class. We analyze stocks, bonds, currencies, and commodities based on supply and demand, momentum and trend.

Young Aristocrats

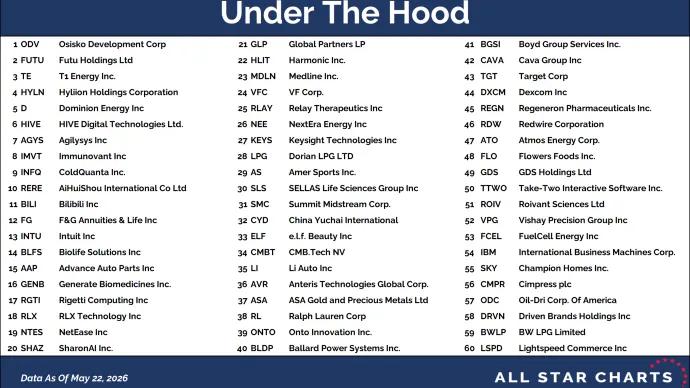

Under The Hood

The Bond Report

Minor Leaguers

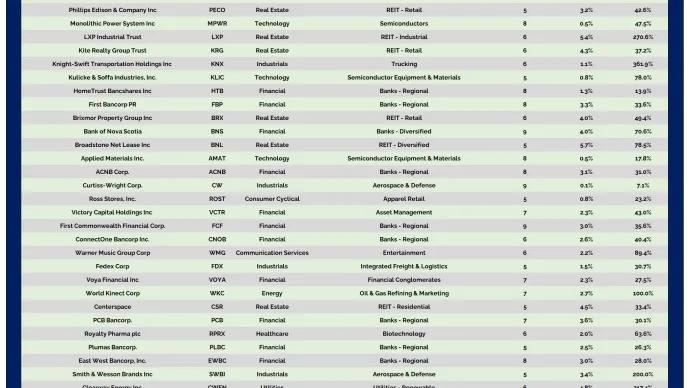

2 to 100 Club

Freshly Squeezed

Currency Report

All Star Charts Gold Rush

Junior International Hall of Famers

Commodities Weekly

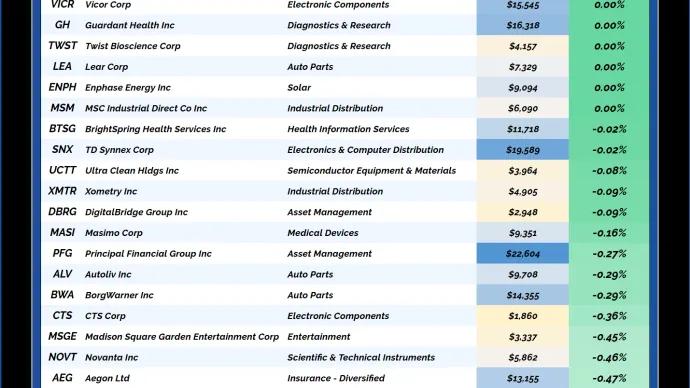

Short Report

International Hall of Famers

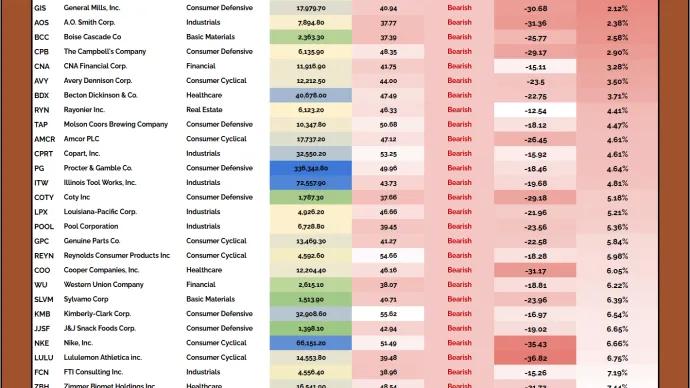

Hall of Famers

Junior Hall of Famers